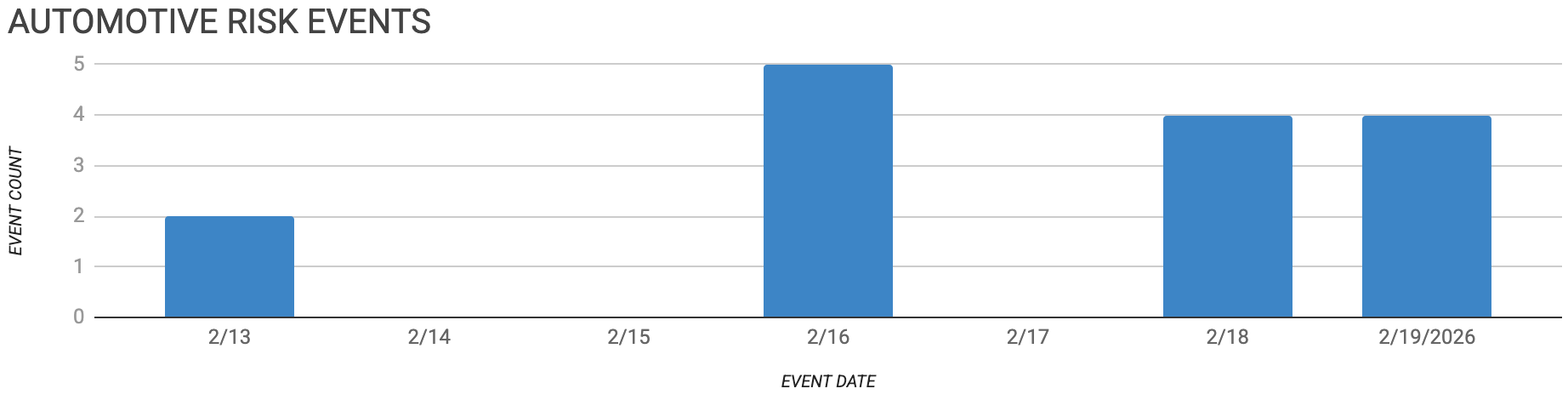

Automotive Supply Chain Risk Digest #470

February 13 - 19, 2026, by Elm Analytics

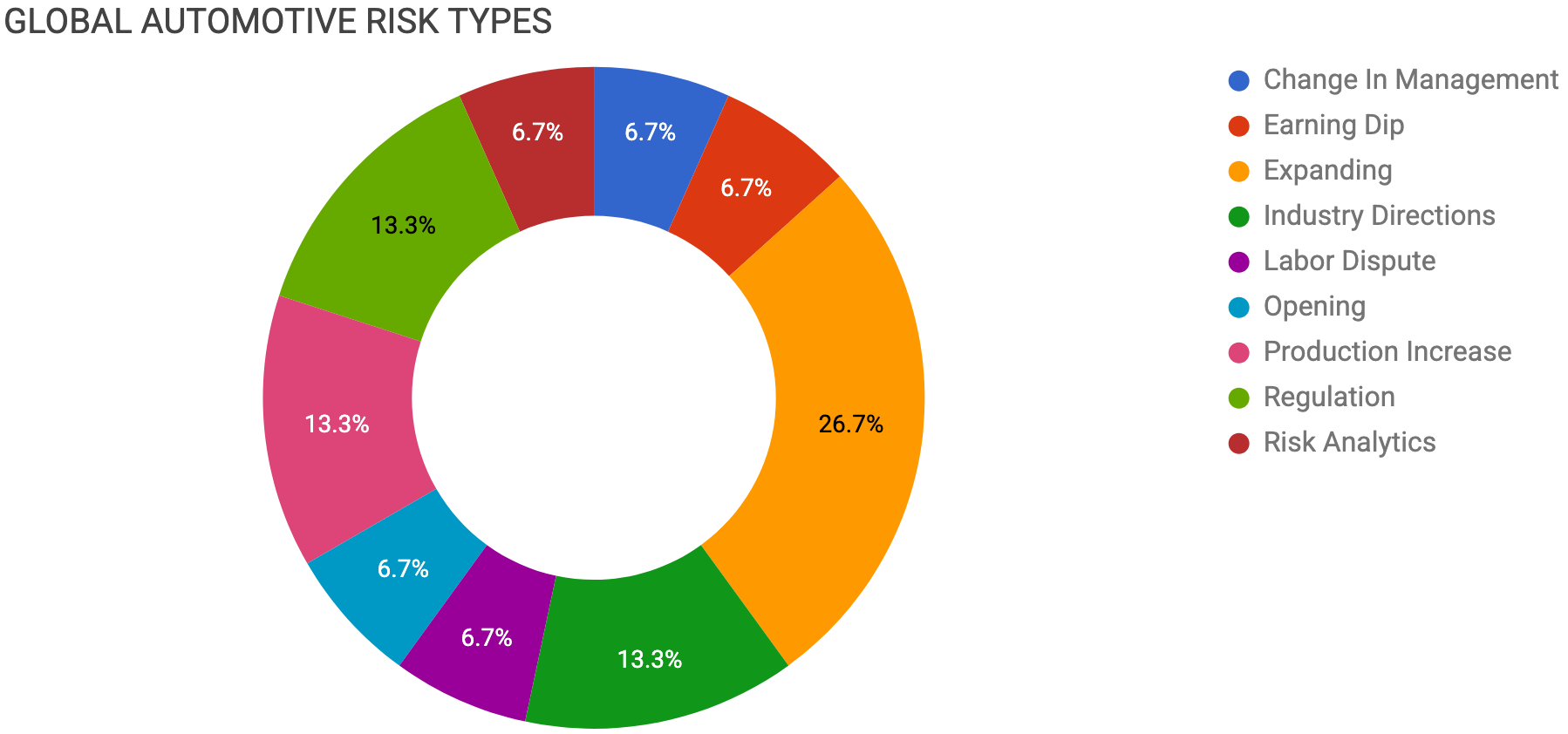

Contents

CHANGE IN MANAGEMENT

Stellantis hires GM supply executive

EARNING DIP

Renault expects lower 2026 margins

EXPANDING

JSW MG triples India capacity

Valeo expands India EV operations

Nexperia secures loan to boost chips

GM invests in Oshawa stamping

INDUSTRY DIRECTIONS

Automakers rewrite contracts for tariffs

Stellantis revives diesel models Europe

LABOR DISPUTE

Tesla union dispute escalates Berlin

OPENING

Elastomer Solutions opens Mexico plant

PRODUCTION INCREASE

Renault considers EV production Spain

GM boosts Korean output for US

REGULATION

EU proposes local content EV rules

ITC reviews USMCA auto origin rules

RISK ANALYTICS

Supply chains shift to adaptive resilience

Change In Management

Stellantis has hired Marcelo Conti, a former GM supply chain executive, as its new North America purchasing chief, while Marlo Vitous moves into a global role overseeing indirect purchasing.

The reshuffle comes as Stellantis faces mounting cost pressures and EV-related losses, and at the same time pushes to strengthen supplier relationships and improve quality.

In parallel, GM’s work on Tier-n mapping and deeper supply chain visibility underscores how critical multi-tier risk management and strong supplier relations have become for the industry, especially as Stellantis ramps up production.

Earning Dip

Renault expects lower 2026 margins due to EV growth, international expansion, and consolidation of its India JV. Ongoing cost-reduction targets highlight continued pressure on suppliers and on manufacturing efficiency.

Expanding

JSW MG Motor, the Indian joint venture between SAIC and JSW Group, plans to invest up to $440M to triple plant capacity to 300k units and support a wave of new hybrid and EV launches in India.

The company aims for new energy vehicles to make up most of its lineup and is pushing deeper localization to reduce import and currency exposure.

The expansion creates new opportunities for suppliers in India, but also adds financial and geopolitical risk to the regional footprint.

Valeo plans to invest more than $216M to expand and localize operations in India, aiming to lift sales to about $756M by 2028.

The company has also secured a nearly $1B order for electric powertrains for Mahindra’s Born Electric platform.

From a supply chain risk perspective, the strategy shifts more EV sourcing to India, reducing reliance on China but increasing ramp-up and localization execution risks.

Invest International, backed by the Dutch government, will lend Nexperia $60M to upgrade its global chip production sites.

The funding is aimed at boosting output, modernizing production lines, and improving efficiency. It follows Nexperia, owned by Wingtech, facing heightened scrutiny over its governance amid geopolitical tensions. A

The Dutch state intervened by installing a European management team, a move that also contributed to disruptions in the supply of automotive chips.

In a separate step, a Dutch court has ordered an investigation into possible mismanagement, while allowing the current European leadership to remain in place.

For automotive supply chains, the loan should support near-term capacity and stabilize supply, but ongoing trade tensions and governance issues are likely to keep pressure on the availability of high-volume commodity semiconductors.

GM is investing $47M in Oshawa stamping operations to prepare for next-generation full-size pickups, extending production into the late decade.

The announcement comes amid layoffs and ongoing tariff pressure. The upgrade signals a long-term commitment to the program, but also continued exposure to trade-related costs.

Industry Directions

As automakers expand production across the US Sun Belt, many are rewriting supply contracts to more directly address tariff risk, raw-material price volatility, and ongoing inflation.

Older agreements that lack clear price adjustment mechanisms or flexible force majeure terms are now under strain, prompting renegotiations and, in some cases, disputes.

As a result, contract design is emerging as a primary lever for managing supply chain resilience.

Since late 2025, Stellantis has reintroduced diesel variants on at least seven European passenger car and van models, reversing course as EV demand underperforms and emissions rules soften.

Diesel now accounts for only 7.7% of new EU car sales, compared with 19.5% for full EVs, but the powertrain still offers a lower-cost option and helps address a competitive gap versus Chinese entrants that are heavily focused on EVs.

Labor

Legal complaints and defamation claims between Tesla and IG Metall are escalating ahead of a key works council election at the Berlin plant.

The dispute is closely linked to wage standards, union influence, and potential investment decisions that could shape Tesla’s European production capacity.

The controversy also comes amid a sharp decline in European sales and recent workforce reductions at the site.

Opening

Elastomer Solutions México has opened a $15M, 54k ft² plant in Zacatecas to produce elastomer components for automotive applications. The facility will supply OEMs, including BMW, Audi, VW, Mercedes-Benz, and Nissan.

Production Increase

Renault is considering building its next-generation compact EVs at its Palencia, Spain, plant, expanding production beyond its France-based ElectriCity network.

The potential shift aligns with CEO François Provost’s broader restructuring agenda, including the reintegration of Ampere and a review of current EV ventures.

Allocating these programs to Spain would reshape European supplier volumes and adjust logistics footprints tied to Renault’s AmpR platforms.

GM plans to lift Korean production to 500k units to meet US demand for Trax, Trailblazer, and Buick crossovers, even as tariff rules remain uncertain.

The Korean plants operate mainly as export bases, making them highly sensitive to a potential duty hike from 15% to 25%.

This trade risk could flow directly into cost structures and threaten the continuity of supply for these high-volume US nameplates.

Regulation

The EU reportedly plans to require EVs to contain at least 70% EU-sourced content and to meet additional requirements for battery components to qualify for subsidies under the upcoming Industrial Accelerator Act.

The proposal is designed to counter Chinese competition and reinforce Europe’s manufacturing base, but automakers are split over the risk of higher costs and the potential for retaliation.

The rule would push OEMs and suppliers to build deeper Tier-n visibility and realign regional sourcing strategies to keep projects eligible for incentives.

The ITC is reviewing USMCA automotive rules of origin to assess economic and competitiveness impacts and reflect recent technology changes, with a report due in July 2027.

Current rules require 75% North American content, along with specific “core parts” and labor value thresholds, for vehicles to qualify for duty-free treatment.

Most automakers support extending USMCA, while Stellantis argues that non-North American vehicles should face origin requirements that mirror USMCA, or that tariffs on USMCA-compliant vehicles produced in Mexico and Canada should be removed.

Any reforms that emerge from this review could trigger sourcing shifts and increase compliance burdens across North American supply chains.

Risk Analytics

Automotive supply chains are entering a new era in which disruption is no longer episodic but structural, driven by geopolitics, tariffs, industrial policy, and rapid technological change.

The 2026 AlixPartners Disruption Index (pdf) shows that leading companies are moving beyond tactical firefighting toward strategic supply chain redesign.

They are diversifying suppliers, shifting production footprints, and increasing investment in resilience.

At the same time, AI is moving quickly from pilots to day-to-day use, especially in procurement and operations.

Energy availability and cost are also emerging as critical constraints that shape manufacturing and supplier network decisions.

The message for supply chain leaders is clear: build flexibility, modernize systems, and embed continuous adaptation into the operating model, or risk falling behind.

The Risk Analytics section is a very interesting statement this week.