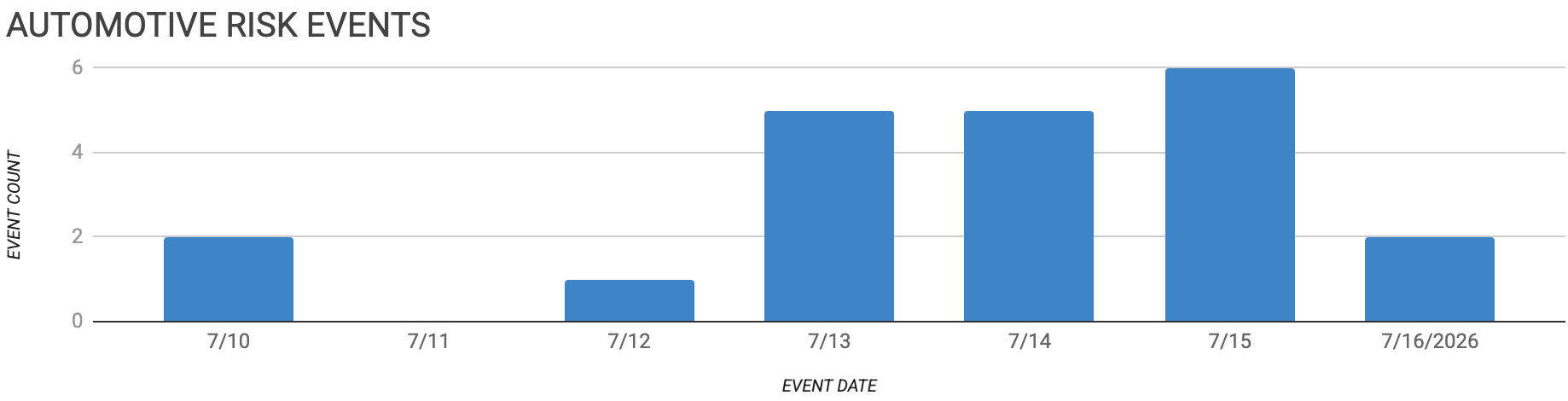

Automotive Supply Chain Risk Digest #491

July 10 - 16, 2026, by Elm Analytics

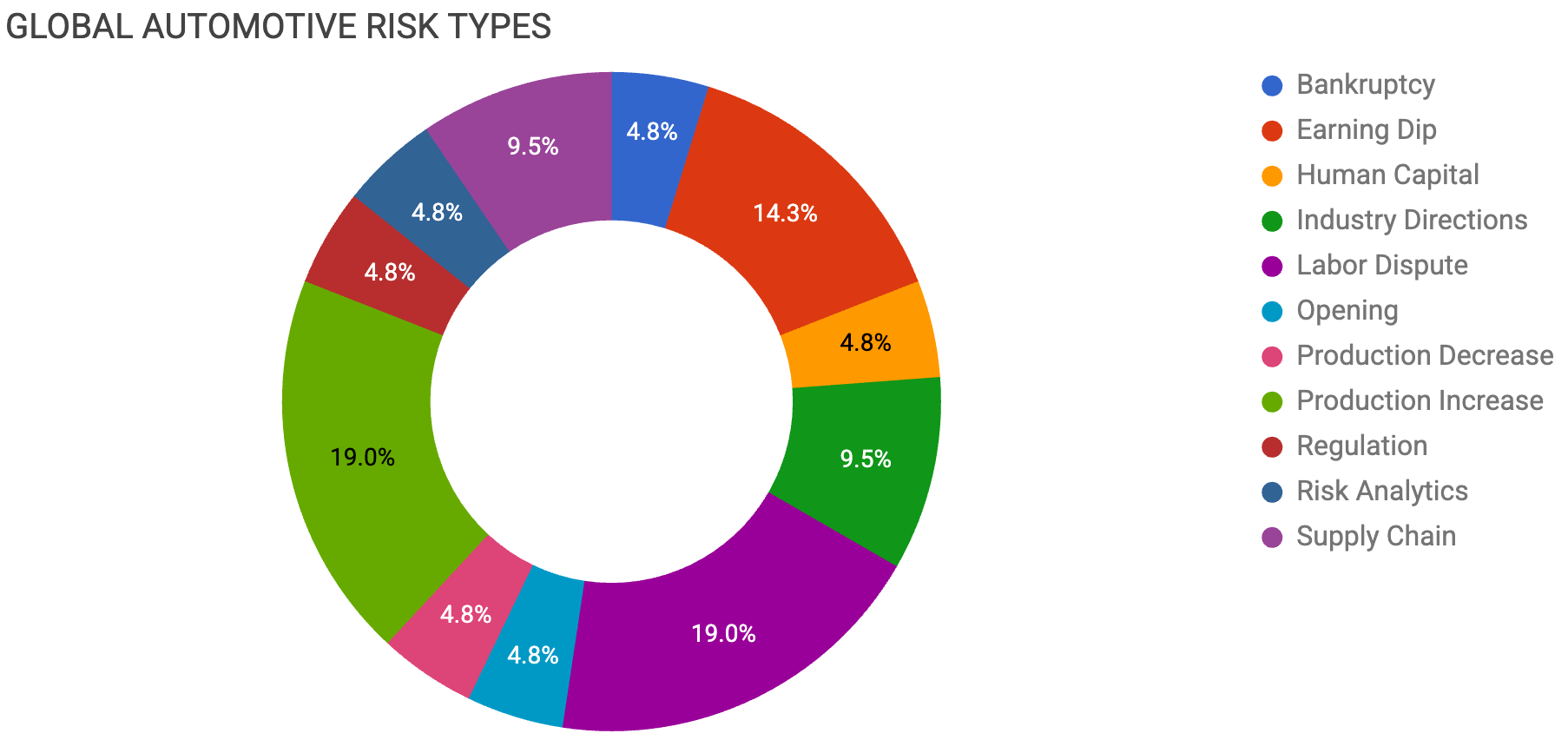

Contents

BANKRUPTCY

Lucid hires turnaround adviser amid strain

EARNING DIP

Memory shortages drive automotive costs higher

Seres swings sharply into first-half loss

GAC losses widen despite sales growth

HUMAN CAPITAL

Volkswagen targets another 50k job cuts

INDUSTRY DIRECTIONS

Volkswagen shifts toward structural capacity reduction

Chinese vehicle exports surpass 1M

LABOR DISPUTE

Hyundai workers strike over humanoid robots

Wage dispute threatens production losses at Hyundai

Ford and Unifor reach tentative agreement

UAW wins major supplier wage gains

OPENING

Hyundai SK On battery plant starts

PRODUCTION DECREASE

Honda ends US Prologue production

PRODUCTION INCREASE

Mercedes expands Hungarian EV production

Stellantis shipments surge in North America

Bosch starts US silicon carbide production

Gotion starts four overseas battery plants

REGULATION

USMCA talks target stricter content rules

RISK ANALYTICS

Chinese mineral curbs threaten global output

SUPPLY CHAIN

Samsung advances Tesla AI5 chip production

Gordie Howe Bridge adds border redundancy

Bankruptcy

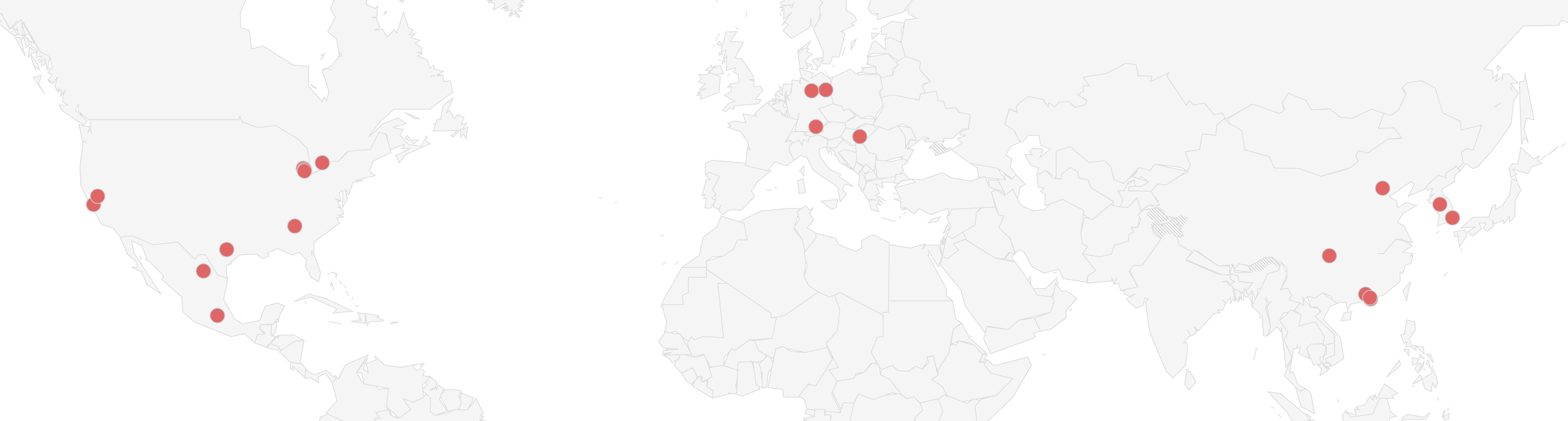

Lucid Group has hired AlixPartners to advise on a turnaround after a report that the EV maker could seek bankruptcy or go private, both of which the company denied. Lucid ended the first quarter with about $700M in cash against about $2B in debt. In late June, it laid off about 18% of its US workforce, including its chief operating officer, while cutting the second shift at its Casa Grande, Arizona, plant. Q2-2026 deliveries were 3.9k vehicles, barely ahead of a year earlier, and the majority owner, Saudi Arabia's Public Investment Fund, has so far kept the company funded. For suppliers on the Air and Gravity programs, a turnaround adviser, thin cash, and a single-shift plant are the standard checklist items that precede volume cuts.

Earning Dip

AI demand has turned memory chips into the automotive supply chain's newest cost crisis. Samsung, SK Hynix, and Micron have shifted 70% to 80% of advanced capacity to high-bandwidth memory and server DDR5, squeezing the general-purpose DRAM and NAND that vehicles use, and automotive buyers, roughly 3% of the global DRAM market, are struggling to secure allocation even at premium prices. Q2-2026 DRAM contract prices rose 58% to 63% quarter over quarter, NAND jumped 70% to 75%, and suppliers have already notified customers of further 20% to 30% DRAM and 35% to 40% NAND increases for the third quarter.

Seres chairman Zhang Xinghai says a memory chip that previously cost about $3 now runs nearly $15, adding an estimated $2.2k to $3k per vehicle at its Aito brand. Ford and GM have signed supply agreements with Micron to lock in allocation, while Chinese players are turning to cockpit-ADAS fusion architectures that share a single SoC and memory pool, yielding an estimated $300 to $440 per vehicle in savings. UBS sees the DRAM imbalance persisting at least through the first half of 2028, so this is a structural cost, not a cycle to wait out.

Seres expects a first-half net loss of $220M to $265M, a swing from a $435M profit a year earlier, citing rising prices for memory chips, industrial metals, and lithium carbonate, along with asset writedowns. Core subsidiary Aito, the Huawei partner brand, swung to a loss, and group sales fell 28% year over year in June. The speed matters: Seres was still profitable in the first quarter, so essentially the entire loss fell in the second quarter, a measure of how quickly input costs are moving.

GAC Group expects a first-half net loss of $600M to $675M, nearly double the year-earlier deficit, despite rising sales, growing exports, and improved gross margins. The joint ventures that have long funded the group are shrinking, with GAC Honda's first-half sales down 55.8% to 68k units and GAC Toyota slipping 9.4% in June, while the Aion and HYPTEC EV brands remain loss-making despite 88.5% sales growth. China's auto manufacturing profit margin fell to 3.4% from January through May, a five-year low. Volume no longer buys profit in China's market, and GAC is the clearest example yet of a legacy player bleeding from both the old business and the new one at once.

Human Capital

Volkswagen Group CEO Oliver Blume has outlined a plan to cut up to 50k more jobs globally, on top of the 50k already agreed with unions in 2024, arguing that the group's overhead is roughly one-fifth above competitors’. Four German plants are at risk: Emden, Hanover, Zwickau, and Neckarsulm, though Blume says there are “smarter options” than closures and points to an average 20% improvement in German factory costs over the past year. The group, which employs more than 657k people, is also reviewing a portfolio of more than 2k stakes and businesses after selling 51% of its ship engine unit, Everllence, for about $8.5B.

Industry Directions

VW's plan stalled at a July 9 supervisory board meeting, where union opposition blocked closures and further cuts. The board instead announced a “Future Plan” to trim the model lineup by up to 50%, cut product complexity by up to 75%, and reduce annual capacity from 10M to about 9M vehicles, with little detail on how it would be executed. The stakes run past Wolfsburg: Germany’s auto industry has shed 125.8k jobs since 2019, a quarter of them in the past year, and Boston Consulting Group estimates Europe carries more than 20% excess vehicle capacity, about 5.4M units a year, with factory utilization near 60% against the 80% needed to run efficiently. For suppliers, German OEM restructuring is no longer cyclical cost-cutting but a structural resizing, and the footprint decisions made in the next year will set sourcing patterns for a decade.

One reason for that pressure keeps growing. Chinese automakers exported 1.1M vehicles in June, the first month above the 1M mark and more than 70% higher than a year earlier, even as domestic sales fell for a ninth straight month. The push is moving onshore in destination markets too, with Chinese OEMs planning to lift overseas production from 1.2M vehicles last year to 3.4M by 2030, BYD's Hungary plant opening later this year, and a second European site in the works. The average net margin across a basket of 12 global automakers has fallen to 1% from about 6% five years ago, and the EU is reportedly reconsidering whether to extend duties to battery-gasoline hybrids, which currently escape the tariffs applied to pure EVs.

Labor

Hyundai's roughly 40k-member Korean union launched a three-day partial strike this week, the auto industry's first factory stoppage centered on humanoid robots. The trigger was Atlas, the 6-foot-2 robot from Hyundai-owned Boston Dynamics, unveiled in January and slated for deployment by 2028 at the nonunion Metaplant in Georgia, with no timeline yet for Korea. At an estimated $130k per unit, Atlas pays for itself in about two years, and the union is demanding job-security guarantees around AI adoption, a shift from hourly pay to fixed salaries to protect against reduced hours, and a retirement age of 65, up from 60.

The wage gap is also real. Hyundai offered a $67 increase in basic monthly pay, annual bonuses worth up to 350% of monthly salary, a one-time payment of about $7.1k, and 15 shares per worker. The union rejected it, seeking a $100 monthly increase and bonuses worth 800% of salary. The two-hour-per-shift stoppages through Wednesday could cost about 5k vehicles and $134M in lost production. The union has threatened stronger action if there is no deal by Thursday, while workers at GM Korea, also affiliated with the Korean Metal Workers' Union, ran a two-day partial strike of their own. It will be interesting to see how any contractual automation language settles; this will likely serve as the template that other unions cite in negotiations.

Labor is moving in North America, too. Ford reached a tentative three-year national agreement with Unifor covering more than 5k Canadian workers, subject to ratification. The union opened with Ford first among the Detroit 3, citing the automaker's commitment to its Canadian operations, and noted that current contracts across Ford, GM, and Stellantis expire on September 20. Some 6k workers have been laid off across the three companies' Canadian operations as production has shifted or paused. A Ford pattern settled two months early would set the target for GM and Stellantis talks, where the footprint questions are harder to answer.

The UAW is running the same playbook down the supply chain. The union has won two rich supplier contracts in metro Detroit by leveraging just-in-time truck programs: about 1.1k workers at Bridgewater Interiors' Warren, Michigan seat plant, which feeds Ram 1500 and F-150 assembly, won a top rate of $35 per hour by the end of 2029, a 36% raise, after a strike threat that would have stopped both truck lines within an hour. It follows the Dauch Corporation settlement in Three Rivers, Michigan, where a 10-day strike that threatened GM truck output in Flint and Wentzville produced a 36% increase to $30 per hour by 2030. Neither contract contains automation language, and the union sought but did not win plant-closure or work-relocation protections at Dauch. Dana, Nexteer, and Magna are next in line for renewals. Supplier labor is being repriced across the Detroit base at the same moment OEMs are pushing suppliers to automate, which points toward a smaller, higher-paid independent parts supplier workforce.

Opening

Hyundai and SK On's $5B joint-venture battery plant in Bartow County, Georgia, has begun early-stage production, marking Hyundai's second battery plant in the state. At full capacity, the 3.3M ft² facility will produce 35 GWh annually, enough for about 300k EVs, employ around 3.5k people, and feed the Metaplant near Savannah, which builds the Ioniq 5 and Ioniq 9. The ramp timeline is open, given the US EV slowdown since the federal tax credit ended. Hyundai runs a separate $4.3B, 30 GWh joint venture with LG Energy Solution in the same county.

Production Decrease

Honda is heading the other direction. It will end production of the Prologue, its only US-market EV, with the 2026 model year, winding down sales through early 2027. The SUV is built by General Motors in Coahuila, Mexico, on GM's EV platform, and sold about 40k units last year, roughly a tenth of the CR-V's volume. Earlier this year, Honda scrapped a three-model EV program for Ohio and Canada at a cost of $10B and is pivoting its US lineup to hybrids. The exit removes contract volume from GM's Ramos Arizpe complex, which also builds GM's own Equinox EV and Blazer EV.

Production Increase

Mercedes-Benz has started production of the electric C-Class at Kecskemét, Hungary, following a roughly $1.2B expansion that more than doubled the site to about 47M ft², making it the largest automotive manufacturing footprint in Hungary. Batteries, body parts, and other key components for the electric C-Class and GLB are now made on-site, shortening supply lines, and lines can flex between combustion and electric models, with load shared with Rastatt, Germany. The smaller G-Class will be built exclusively at Kecskemét, which now employs more than 5k people.

Stellantis reported Q2-2026 global shipments up an estimated 10% to about 1.6M vehicles, led by a 38% jump in North America, driven by new and refreshed Ram, Jeep, Chrysler, and Dodge products. European shipments rose 5%, with Leapmotor-branded vehicles contributing 25k units of the increase.

Bosch has begun sample production at its first US semiconductor plant in Roseville, California, following the finalization of a $225M CHIPS Act award, with commercial output of silicon carbide chips expected later this year. The company bought the fab from TSI Semiconductors in 2023 and is spending $2B in total on the conversion, part of up to $7.5B in planned US investment through 2031. Silicon carbide chips manage high-voltage power in EVs and hybrids, with data center and defense demand as a hedge. A domestic silicon carbide source lands well with OEMs still carrying scars from the COVID chip shortage and now watching the memory squeeze covered above.

Gotion High-Tech says its four overseas plants, in Germany, Vietnam, Indonesia, and Thailand, are now online, with the Vietnam site producing LFP cells and the other three assembling packs. Its G-Yuan semi-solid-state battery has cleared extreme-condition testing. It is headed for mass production, with a 197 Ah cell delivering above 300 Wh/kg, 12 GWh of planned capacity, and a 0.2 GWh all-solid-state pilot line now complete. The overseas footprint aligns with customers, including Volkswagen, a Gotion shareholder, and China's export push. All-solid-state remains distant, by the company's own admission, so that near-term deliveries will be LFP and hybrid chemistries.

Regulation

Top US and Mexican officials meet the week of July 20 in Mexico City to negotiate automotive rules of origin and tariffs, after the US declined to renew the USMCA at the July 1 joint review, putting the deal on annual reviews ahead of a 2036 expiration. The US wants North American content requirements raised from 75% to 82% of a vehicle, with 50% of value originating in the US, while Mexico and Canada push to cut auto and metals tariffs that run as high as 27.5% on their vehicles versus 15% for the EU, Japan, and South Korea. Mexico says unresolved bilateral issues have fallen from 54 to 14. Industry groups warn that a year-to-year USMCA will suppress capital-intensive regional investment until a durable deal is in place.

Risk Analytics

The IEA warns that the full implementation of China's rare earth export restrictions, currently delayed by a year, would put $6.5T in downstream production outside China at risk across automotive, high-tech, defense, and energy sectors, with the US and Europe absorbing nearly half the impact. Parallel graphite controls would expose another $300B, and China holds more than 90% of processed graphite output. Diversification is moving: public financing for new projects quadrupled to $65B between 2023 and 2025, and new refining in the US and Malaysia cut China's rare earth processing share to 85% last year, with 70% possible by 2035 if planned projects deliver.

Supply Chain

Samsung has taped out its version of Tesla's AI5 self-driving chip and will build it on its latest 2nm process at the Taylor, Texas fab, a node previously expected to debut with the follow-on AI6. The choice suggests Samsung’s 2nm yields have crossed the roughly 60% threshold viable for a high-volume customer, with volume production of Tesla AI chips at Taylor expected in the second half of 2027. Tesla is dual-sourcing AI5 from Samsung and TSMC, with each foundry producing slightly different versions. A credible second source at the leading edge matters beyond Tesla, since every OEM planning in-house silicon has been negotiating against a one-foundry market.

The Gordie Howe International Bridge connecting Windsor, Ontario, and Detroit opens on July 27, after a delay while Washington and Ottawa renegotiated toll governance, including a 15-year economic development fund tied to a portion of the bridge's profits. The crossing adds redundancy to a corridor where the Ambassador Bridge alone carries more than $300M in goods daily and handled 1.8M trucks in 2025, many moving parts and finished vehicles on just-in-time schedules. The 2022 blockade showed what a single-crossing chokepoint costs. A second span is the rare piece of transportation risk that actually got fixed.