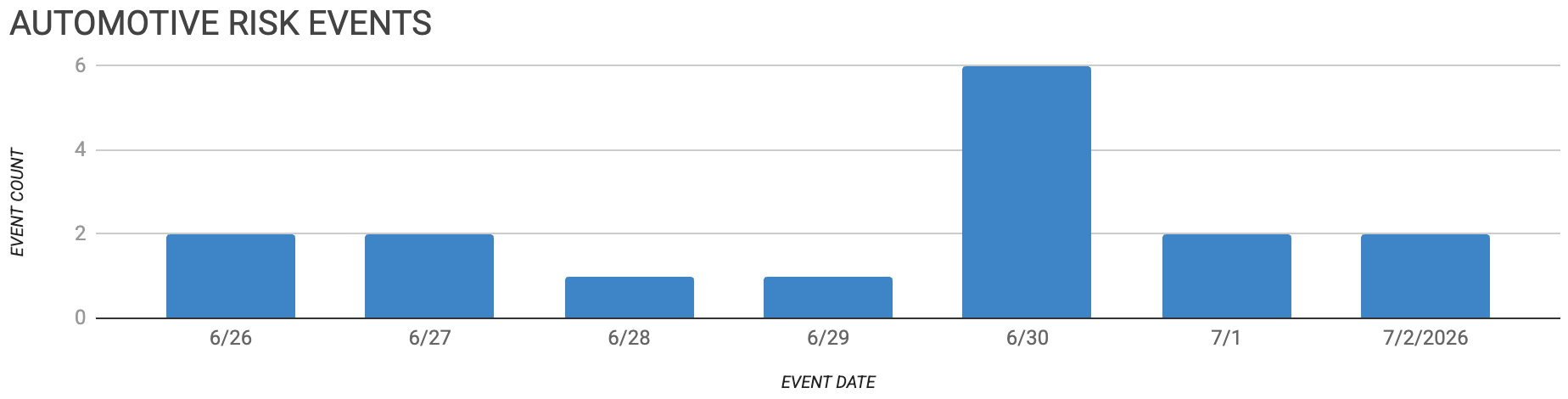

Automotive Supply Chain Risk Digest #489

June 26 - July 2, 2026, by Elm Analytics

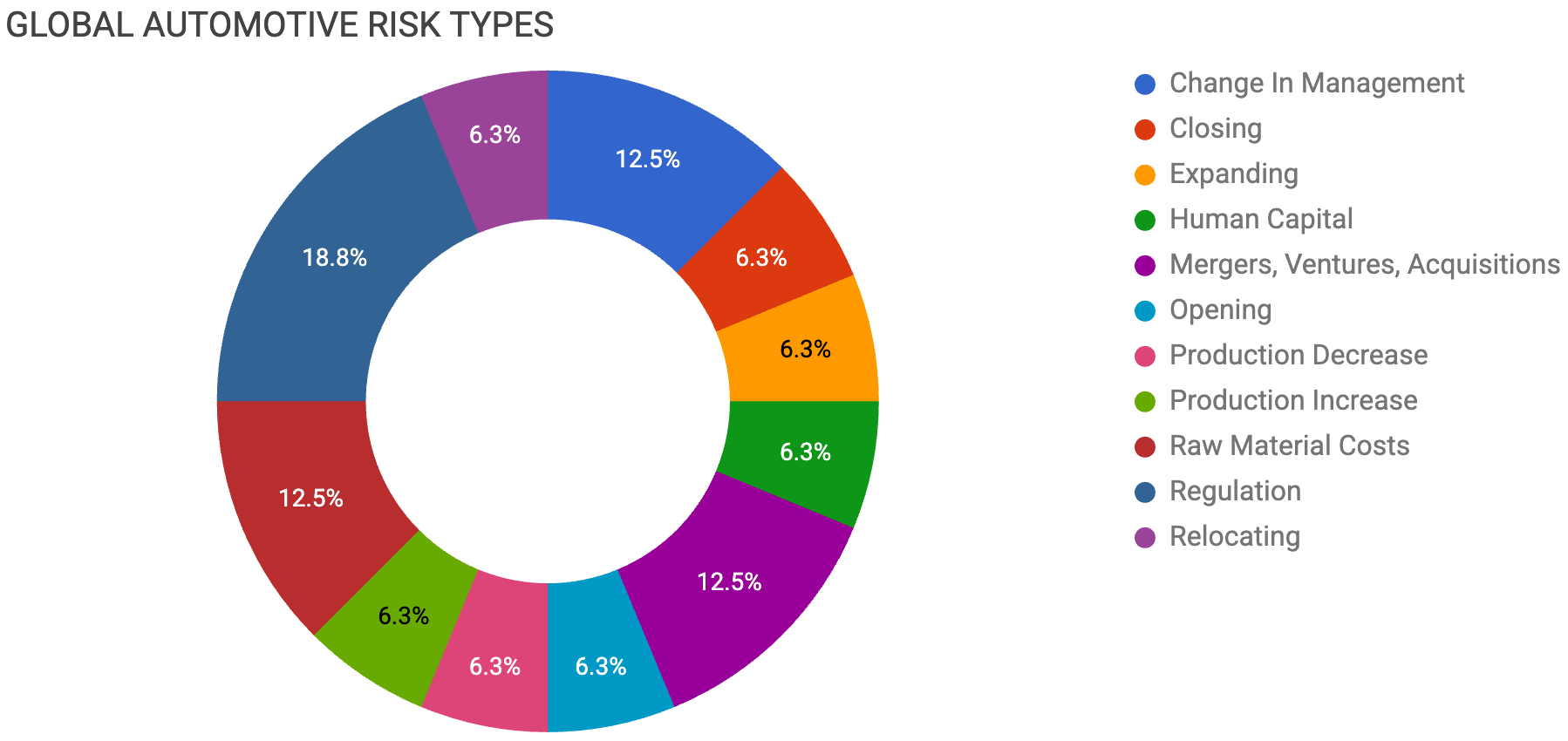

Contents

CHANGE IN MANAGEMENT

Lucid misses deliveries, names CFO

Christian Fischer as Bosch CEO unexpected

CLOSING

Shiloh closes Valley City plant

EXPANDING

BorgWarner expands Mexico EV production

HUMAN CAPITAL

Volkswagen weighs massive German cuts

MERGERS, VENTURES, ACQUISITIONS

Volkswagen may end Bosch AV partnership

Stellantis, Nissan eye Marelli assets

OPENING

Ford CATL-licensed plant starts production

PRODUCTION DECREASE

Mercedes electric GLC ramp

PRODUCTION INCREASE

CATL restarts Jianxiawo lithium mine

RAW MATERIAL COSTS

Battery metals recovery faces risks

Automakers shift copper to aluminum wiring

REGULATION

USMCA enters sunset review process

US demands stricter USMCA content

UK EV makers face tariffs

RELOCATING

Porsche may shift Cayenne production

Change In Management

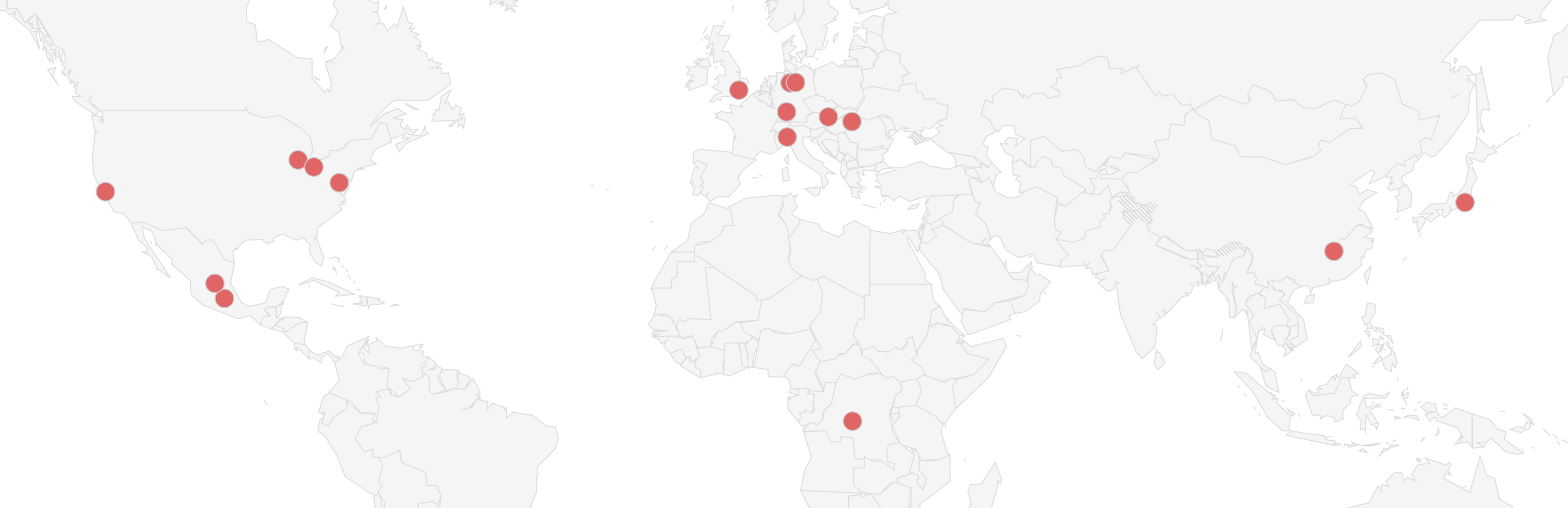

Lucid missed second-quarter delivery estimates with 3.95k vehicles delivered and 4.77k produced, against expectations of 4.61k and 5.28k. The EV maker also named TI Automotive finance veteran Alexander De Bock as CFO, the latest move in an executive shakeup that has brought in a new CEO and CTO and led to the COO's departure since April. Lucid suspended its 2026 production forecast in May, has cut its workforce twice this year, and is streamlining its supply chain to conserve cash. Supplier disruptions and aluminum and chip shortages continue to slow its production ramp.

Bosch replaced CEO Stefan Hartung with deputy chief executive Christian Fischer on July 1, an unexpected change at the top of the world's largest parts supplier just months after Hartung's contract was renewed through 2031. Hartung, who has been the chairman since 2022, steered Bosch through last year's profit slump and, in April, outlined margin plans built on tighter cost control and technology investment. Fischer helped shape that strategy, so the handover signals continuity as suppliers contend with high costs, weak demand, and geopolitical strain.

Closing

Shiloh Industries will permanently close its manufacturing operation in Valley City, Ohio, cutting 43 jobs. Shiloh supplies lightweight metal stampings and laser-welded assemblies to North American OEMs and Tier 1 suppliers.

Expanding

BorgWarner will invest $49M to expand manufacturing in San Luis Potosí, Mexico, adding local production of electronic components and EV technologies through 2028. The expansion is projected to create 663 engineering and technical jobs by 2030, with 421 of those front-loaded into 2026 to meet immediate technical requirements.

Human Capital

Volkswagen is reportedly weighing closing four German plants, Hanover, Zwickau, Emden, and Audi’s Neckarsulm site, and raising total job cuts to as many as 100k, according to people familiar with plans headed to a July 9 supervisory board meeting. The closures would put more than 45k jobs at risk on top of 50k cuts already planned, and the group would trim investment by about 15% to roughly $148B over five years, with a possible spinoff of the core VW brand and parts operations into separate entities. The works council, IG Metall, and the state of Lower Saxony have all vowed resistance, the same coalition that forced CEO Oliver Blume’s retreat from closures in 2024. The pressures have only worsened since then. Non-Chinese automakers’ share of the Chinese market fell from 57% in 2020 to 32% in 2025, and BYD, Chery, SAIC, and Leapmotor doubled their combined European share through May. A restructuring of this scale would take years to work through the German supply base. Suppliers with heavy exposure to the four named plants should be reassessing program volumes now, not after the July 9 meeting.

Mergers, Ventures, Acquisitions

The cost drive extends to software. Volkswagen reportedly plans to end its automated-driving partnership with Bosch, launched in 2022 through its software unit Cariad, after roughly $1.7B in investment produced technology that internal assessments judged not yet competitive, per a Bild report. VW intends to source driver-assistance hardware and software from a new partner instead, with a contract targeted for September.

Stellantis and Nissan are in talks to take over some Marelli assets as the supplier works through Chapter 11, one year after filing. Stellantis is discussing Marelli's suspension business in Italy, Poland, Brazil, and Mexico, while Nissan is looking at cockpit assets in Japan. The two automakers are Marelli's largest unsecured creditors, and their future order commitments will be key to the reorganization, which is expected to conclude this year under the ownership of senior lenders including Strategic Value Partners, MBK Partners, Fortress, and Polus Capital. Carve-outs for the two customers most dependent on Marelli parts would keep critical lines running while reducing the value realized from bankruptcy. Anyone sourcing from the remaining 150-plus-facility portfolio should watch which assets stay.

Opening

The LFP battery plant Ford built in Michigan under CATL technology licensing was completed and began production in June, according to a CATL vice president. The project survived a rocky three years: congressional scrutiny, a 2023 suspension and restart at reduced scale ($2B and 20 GWh, down from $3.5B and 35 GWh), and Ford's December 2025 EV retrenchment, which wrote down $19.5B in EV assets and shifted part of the plant's capacity to energy storage products. First automotive battery deliveries remain on schedule for 2026, destined for Ford's economy and mid-size electric pickups.

Production Decrease

CATL also sits at the center of a Mercedes-Benz production problem. Mercedes paused the ramp of the electric GLC at Bremen after battery deliveries from CATL's new Debrecen, Hungary plant were delayed by environmental certification issues, forcing slower sea shipments from China, and after spring flooding damaged wiring harness production at Kromberg & Schubert's Morocco plant. Mercedes says both issues are resolved, but customers face waits of around six months, and it is unclear whether lost output can be recovered by year-end.

Production Increase

CATL's Jianxiawo lithium mine in Yichun, Jiangxi, resumed production on June 29 after securing its safety permit, ending a suspension that began in August 2025 when its mining license expired. The lepidolite mine has an annual capacity of about 100k tons of lithium carbonate and accounted for 8% to 10% of China's output before the halt, with analysts expecting more than 45k tons of incremental supply in the second half. Lithium carbonate futures still jumped 8.4% on the news to about $24.1k per ton, though high inventories and the fresh supply are expected to hold prices in a range of roughly $22k to $29k per ton.

Raw Material Costs

Resource: Reuters columnist Andy Home on why the battery metals bust has run its course. Useful context for the Jianxiawo restart above. Cobalt and nickel recoveries rest on export controls in the DRC and Indonesia, lithium's on price-driven supply destruction, and grid storage is now 15% of battery demand. The column flags demand-destruction risk if prices keep climbing, with some storage projects already at break-even.

Automakers, including Ferrari, BMW, and Stellantis, are expanding the use of aluminum wiring in place of copper as copper prices approach record levels near $15k per ton, more than four times aluminum's price. JPMorgan estimates the substitution will affect about 2% of global copper demand this year and could displace up to 6% by 2030, with Chinese policy guidance actively encouraging the switch. Aluminum's lower conductivity requires larger cables, and US tariffs on aluminum products complicate the economics. For harness and cable suppliers, the transition is becoming a real requalification workload, and copper exposure in long-term contracts deserves a fresh look.

Regulation

The Trump administration will not extend USMCA, starting the pact’s sunset process: annual reviews for up to 10 years, with expiration on July 1, 2036, unless the three countries agree to a 16-year extension. Mexico has signed a letter seeking extension, and Canada says it is ready to negotiate improvements, but Washington has scheduled its next formal round with Mexico only for the week of July 20, leaving Canada sidelined amid a list of bilateral irritants. The declaration changes little on the ground, since US tariffs of 25% on Canadian and Mexican autos and parts and 50% on steel and aluminum already override the pact’s duty-free terms.

The substance of the review is content rules. The US is demanding 50% US-specific content in North American vehicles, which would push required regional content to about 82% from today's 75%, and wants higher thresholds on parts, including batteries and ADAS, where a capable local supply base largely does not exist. Automakers are united in wanting the pact preserved as a trilateral deal, with Ford calling it a bedrock for investment and GM seeking lead time on any origin changes, while the UAW wants import quotas, a wage floor, and stricter labor enforcement, or US withdrawal. A Mexican official said both governments agree on the problems and floated a universal 15% auto tariff with a lower rate for Mexico and Canada under tighter rules of origin.

Rules of origin are also the flashpoint across the Atlantic. The SMMT estimates that British EV makers face $1.85B in tariffs if the UK and EU do not resolve battery content requirements before they take effect in January, triggering a 10% tariff on 70% of battery-electric and plug-in hybrid vehicles traded between the two. The trade at risk is worth about $21.7B, and the rules were already delayed once in 2023 after carmakers threatened to close British plants.

Relocating

Porsche plans to move Cayenne production from Slovakia to its Leipzig plant to shore up capacity utilization in Germany, conditional on workers accepting pay cuts, per an FAZ report. The move represents part of the wider Volkswagen Group cost drive and follows Porsche's decision not to renew several hundred temporary contracts, as well as a plan to cut 200 jobs by August through voluntary agreements. Volumes leaving Bratislava would dent utilization at the Slovak plant and pull demand from its local supply base.