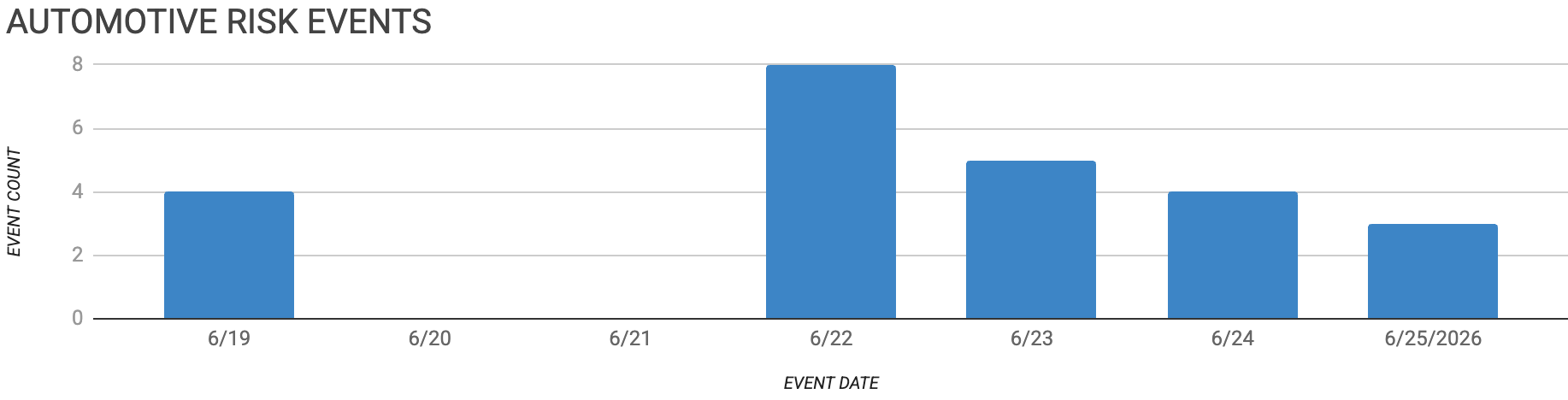

Automotive Supply Chain Risk Digest #488

June 19 - 25, 2026, by Elm Analytics

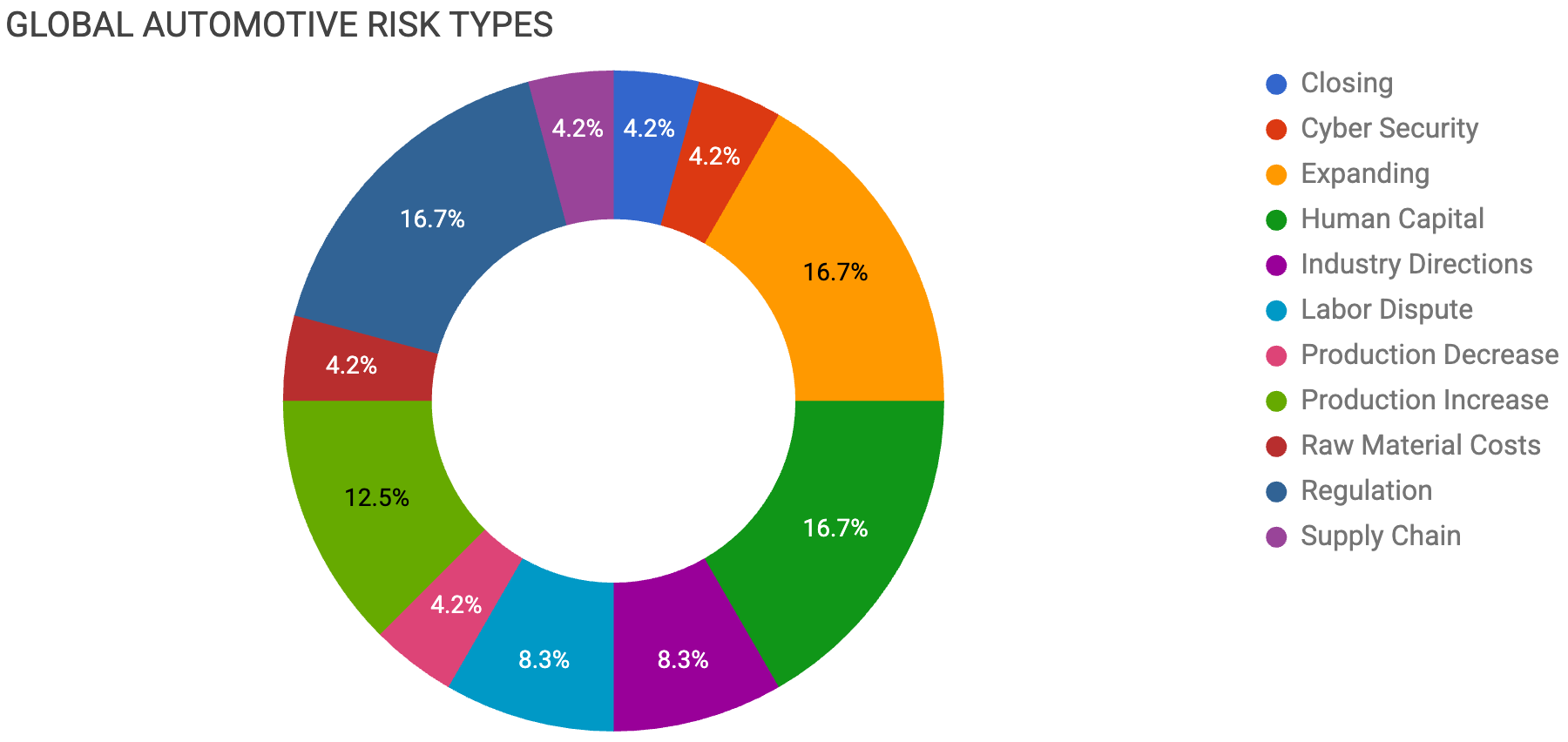

Contents

CLOSING

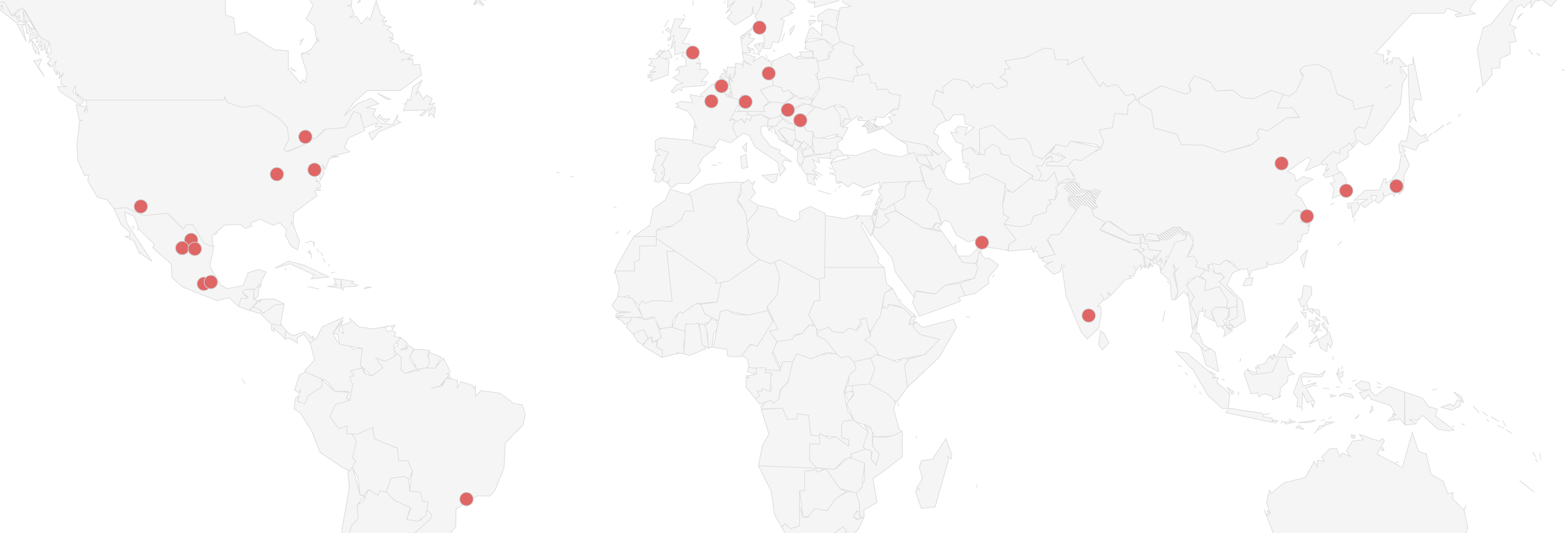

Nissan ends CIVAC production

CYBER SECURITY

Tata Electronics breach exposes designs

EXPANDING

GM expands Brazil investment

BYD accelerates European manufacturing

Henglong builds Saltillo steering plant

EcoCable plans Durango copper plant

HUMAN CAPITAL

Lucid cuts jobs and shifts

Renault reduces French engineering roles

Porsche weighs deeper workforce cuts

Tesla expands Giga Berlin staffing

INDUSTRY DIRECTIONS

Subaru adds flexible powertrain production

Nissan pauses electric Qashqai plans

LABOR DISPUTE

Hyundai union authorizes strike action

Audi Mexico reaches union deal

PRODUCTION DECREASE

Oshawa Silverado output faces cuts

PRODUCTION INCREASE

Toyota ramps hybrid RAV4 output

Mexico auto parts production hits record

Volkswagen starts MEBeco drive production

RAW MATERIAL COSTS

LFP cathode prices double

REGULATION

Polestar barred by Chinese software rule

US Section 232 relief demands traceability

China targets US rare-earth firms

EU prepares China PHEV tariffs

SUPPLY CHAIN

Hormuz recovery slips to September 2026

Closing

Nissan has closed its CIVAC plant in Jiutepec, Morelos, ending nearly 60 years of production at the site that became its first manufacturing base outside Japan in 1966. Output shifts to Aguascalientes, where Nissan is consolidating Mexican production for export, with the US accounting for close to 45% of its combined Mexico and Japan export sales. The closure is just one piece of a global restructuring that cuts capacity from 3.5M to 2.5M vehicles, shutters 7 of 17 plants, eliminates about 20k jobs, and trims platforms from 13 to 7. For Tier 1 and Tier 2 suppliers tied to CIVAC, the move concentrates Nissan's Mexican demand in a single complex and pulls a decades-old anchor out of the Morelos supplier base.

Cyber Security

Tata Electronics, a contract manufacturer that builds parts for several automakers, confirmed a cybersecurity breach after the ransomware group World Leaks posted more than 200k stolen files totaling over 630GB. The dump included design and specification documents for Tesla components, among them a Model Y charge-port controller and trade-secret drawings for the Model 3, which surfaced as the clearest evidence of the intrusion. The wider Tata group’s Jaguar Land Rover unit was hit by a separate cyberattack last year that halted output for six weeks. As vehicle and electronics production concentrates in a handful of large contract manufacturers, a single breach can expose proprietary engineering across an entire customer roster and idle downstream plants.

Expanding

General Motors will add $675M to its Brazil investment plan, lifting the total committed through 2028 to $2B. The money will mainly fund operations in São Paulo state and support the renewal of the Chevrolet portfolio, hybrid vehicles, and factory modernization. The hybrid tilt mirrors GM’s broader retreat from EV-only plans and points its Brazilian supply base toward combustion and hybrid content rather than battery-electric.

BYD is pressing a long-term European build-out, striving to be seen as a European manufacturer within five years through local production, an expanding dealer network, and region-specific products. It will start building cars at its new Szeged, Hungary plant in Q4-2026, has paused its Turkey project to concentrate on Europe, and is hunting for a second assembly plant it would rather buy than build, with Spain among the options. The push leans on plug-in hybrids such as the new Dolphin G, BYD’s first model developed for Europe, as it hedges against uneven BEV demand. Volkswagen and Stellantis have signaled they could sell plants or partner with Chinese makers to shed overcapacity, which would hand BYD a faster route into European production and rewire the supplier base around those sites.

CHL/Henglong Mexico Automotive, a Chinese firm, is investing $42M in Saltillo, Coahuila, to build steering systems, including power steering, for automotive and commercial vehicle customers. The two-phase project is expected to employ 162 people.

EcoCable is investing more than $31M in a new plant in Gomez Palacio, Durango, to produce oxygen-free copper wire for automotive electrical and electronic systems. The two-phase, 200-worker plant development is expected to begin hiring in early 2027.

Human Capital

Lucid is cutting 18% of its workforce, roughly 1.5k employees, 4 months after a 12% reduction, and has eliminated the 2nd production shift at its Casa Grande, Arizona, plant. The cuts are the first major move by new CEO Silvio Napoli and hit full-time staff, contractors, and hourly production workers, yielding about $158M in annual savings against roughly $32M in severance costs. Lucid produced 5.5k vehicles in Q1 but delivered just 3,093, and the shift cut aligns capacity with demand it is not generating. The Saudi Public Investment Fund remains the backstop, but a second mass layoff in one year and a killed shift signal a reset to a smaller production reality, with volume risk for the supplier base built around Casa Grande.

Renault will cut 800 engineering jobs in France by the end of 2027 as part of a planned 15% to 20% reduction in its engineering workforce, with France accounting for half of the global total of 5.5k. The goal is a leaner, faster R&D operation to match Chinese rivals, which now develop vehicles in 2 years compared to the industry’s traditional 4 to 5 years. The plan, due for union approval in July, also funds retraining for 2.5k workers and 150 to 200 new hires focused on electrification, software, and AI.

Porsche is in talks with employee representatives to cut jobs within a streamlining push, with CEO Michael Leiters warning that the cuts planned so far will not be enough to secure competitiveness. The company is shedding non-core assets, including stakes in Bugatti Rimac and the Rimac Group, and is shutting its Cellforce battery-tech unit, an e-bike drive developer, and a data-communications software maker. It is delaying all-electric rollouts in favor of new gas and hybrid vehicles under a value-over-volume strategy, with restructuring costs expected to range from $915M to $1.03B and tariff costs around $800M this year.

Tesla will hire another 1k workers at its Grunheide plant near Berlin, its second 1k-person wave in three months, as it targets 7.5k vehicles per week from October. That pace, a 25% jump on the roughly 6k weekly run rate that the April hires were meant to deliver, would put the plant near 390k vehicles a year, still short of its 500k design capacity but its highest sustained output. Giga Berlin builds only the Model Y for Europe, so the demand swing feeds straight to the line, and Tesla is separately staffing up local battery cell production. The recovery rides largely on higher European fuel prices steering buyers toward EVs rather than on new products, which leaves the ramp-up exposed if energy markets ease.

Industry Directions

Subaru will start mixed production of hybrid, gasoline, and electric vehicles on a single line at its Yajima plant north of Tokyo in August, its first three-powertrain line, building the Forester hybrid and gas models alongside the electric Trailseeker and Toyota bZ4X Touring. The "ultraefficient production" approach lets Subaru shift volume between powertrains and between its Japanese and Indiana plants as tariffs, exchange rates, and demand move. It plans to extend the method to its US plant and to the new Oizumi plant opening as early as 2028, which will start with combustion vehicles and add EVs later. For suppliers, flexible lines mean less predictable per-powertrain volumes and a premium on components that fit multiple drivetrains.

Sticking with Nissan's restructuring, the automaker has halted development of an electric Qashqai, its top-selling model in Europe, where gas- and hybrid-powered versions accounted for about 45% of its 330k European sales in 2025. The EV was committed to Sunderland in 2023 but was halted early last year, and even a restart would not reach the market until the early 2030s, leaving Nissan trailing in a key segment. A planned three-in-one electric powertrain at the Sunderland JATCO plant has also been scrapped, and Nissan is now seeking UK funding tied to new models and job protection at the 6k-worker site, while studying building Chery vehicles on one of its two lines.

Labor

Hyundai’s South Korean union has voted to authorize a strike after wage talks stalled, raising the prospect of production disruption at Korea’s top automaker. The union wants a $97 monthly base-pay increase, a bonus equal to 30% of last year’s net profit, and guarantees on how AI affects jobs, pressing harder after Samsung agreed to share 10.5% of operating profit with its chip workers.

Labor talks landed more smoothly in Mexico, where Audi reached a pre-agreement with its union for a 19.5% total compensation increase, a 4.6% wage rise plus a 14.9% benefits boost. The agreement is headed to a worker vote on June 23 - 24 at the San Jose Chiapa plant in Puebla. The contract deal comes as Audi’s Mexican output fell 14% year over year through May and exports dropped 23.8%. The plant has already idled twice in 2026 for maintenance and upgrades. A ratified contract clears near-term strike risk at a plant already running below capacity, though the cost step-up adds margin pressure as volumes soften.

Production Decrease

General Motors is on course to end light-duty Chevrolet Silverado 1500 production at its Oshawa Assembly plant before the end of 2026, leaving only the heavy-duty variant, according to AutoForecast Solutions, though GM Canada disputes any scaleback. The plant already dropped from three shifts to two in January, cutting about 700 jobs and roughly 50k units of output. Losing the Silverado could push it to a single shift and about 50k vehicles a year, since the redesigned HD models are not due until 2029. Tariffs on Canada-built vehicles are the throughline, and the contrast is stark: GM is adding light-duty pickup capacity in Indiana and working six-day weeks in Flint, while Oshawa is eroding ahead of summer Unifor contract talks.

Production Increase

Toyota is ramping up production of the redesigned, hybrid-only RAV4 across the three plants that build it after a changeover left US inventory thin, with deliveries down 40% through May to about 122k. Georgetown, Kentucky, began US production in June, adding an expected 40k vehicles this year and scheduled to lift that by about 50% next year, while the bulk of US supply still comes from Canada and the Takaoka plant in Japan that started in December. At Georgetown, the RAV4 shares Line 2 with the hybrid Camry, whose sales are climbing, tightening capacity on a single line. Even with Kentucky online, Toyota expects to finish the year down nearly 55k US RAV4 sales purely on inventory, about $1.8B in lost revenue at roughly $33k wholesale, a steep figure while tariffs push its North American operations into the red.

Mexico’s auto parts production hit a record $31.2B in the first quarter, up 9.6% year over year, driven by stable US assembly demand, which accounts for 87.3% of the country’s component exports. Electrical parts, nearly a 1/5 of output, rose 11.6% to $6.1B, while gasoline engine production jumped 42% to $1.87B, coinciding with Hyundai’s new hybrid-powertrain operations in Nuevo Leon. Coahuila, Guanajuato, and Nuevo Leon led by state, and the sector held a $9.97B trade surplus. Mexican parts now account for 45% of all US automotive parts imports, making the sector’s health and tariff exposure a direct input into US assembly continuity.

Volkswagen Group has started series production of its new MEBeco electric drive at Györ, Hungary, backed by $400M, including about $26M in Hungarian state funding, and is adding 260 workers as output scales from one shift to three. The plant now builds complete powertrain units, including components and assemblies such as the rotor, laminated core, and power electronics, a step up in vertical integration for VW. The MEBeco, part of the MEB+ platform, will power the Cupra Raval and the coming VW ID. Polo, ID. Cross, and the Skoda Epiq small-car family.

Raw Material Costs

Prices for lithium iron phosphate, the most dominant cathode chemistry for EV and storage batteries, have roughly doubled over the past year. A 400-kg pack is now above $3,650, up from about $1,460 a year ago. Demand has held steady through the climb, pulled by accelerating Chinese EV exports and fast-growing energy storage. The capacity that existed during the recent downturn cannot return quickly, so the squeeze will continue to persist. For cell makers and automakers, the price increase feeds straight into battery costs and will force renegotiation of long-term contract pricing, with the likely hedge being upstream deals to lock in mineral supply.

Regulation

Polestar will exit the US market after the Commerce Department denied its request to continue selling, making it the first major casualty of the US rule barring vehicles with Chinese-developed software over national security concerns. The Geely-controlled brand will sell its remaining US stock and keep service centers open, then concentrate on Europe, which accounts for about 80% of its sales. Volvo, also Geely-owned, won authorization in May on a case-by-case review, so the line is being drawn on data and software provenance rather than ownership alone, and lawmakers are now floating a ban on Chinese-owned carmakers building in the US as well.

Supply Chain Dive: Steel, aluminum makers face records gauntlet for new US tariff exemptions

Worth a read for purchasing and trade-compliance teams: Canada and Mexico producers feeding the US auto supply chain can halve the 50% tariff to 25%, but only by committing to specific US capacity-expansion projects and proving it through end-to-end traceability, milestone reporting, and accounting records customs can follow, with the reduced rate revocable if they fall short.

China added MP Materials and USA Rare Earth, both in the US mine-to-magnet rare earth chain, plus motor maker Aveox and other US entities to its export control list, halting Chinese dual-use exports to them in retaliation for recent US restrictions. Analysts read the move as largely symbolic since the named firms are mostly defense-linked and do little business in China, but it lands amid a wider tit-for-tat that added BYD and NIO to a US list of companies seen as aiding China's military. The item to note for automakers remains the ongoing weaponization of rare-earth and magnet supply, where China's leverage over inputs to motors and actuators remains an open risk regardless of these specific designations.

The same Chinese PHEV push driving BYD’s European strategy is now drawing a tariff response. The European Commission has prepared duties on plug-in hybrids built in China and could impose them once a majority of member states agree, extending the countervailing duties already on China-built BEVs and range-extenders that add up to 35% on top of the standard 10%. Chinese brands pivoted to PHEVs to sidestep BEV tariffs, and it worked: the BYD Seal U is the EU’s best-selling PHEV, and Chinese-brand PHEV sales were up 236% in April. Closing the PHEV lane would push the same makers harder toward local European assembly, accelerating the plant purchases and factory-sharing deals already in motion and pulling Chinese supplier content onto the continent.

Supply Chain

The US and Iran have agreed to reopen the Strait of Hormuz; however, ocean networks are not expected to recover until mid-September 2026, with a 60-day window to complete the deal and minesweeping still ahead. Far East to US West and East Coast spot rates have jumped 192% and 158%, respectively, since the conflict began in February. Those rates are expected to keep climbing for about 4 weeks before peaking around the formal reopening of the Strait. Bunker fuel and oil prices fell roughly 20% in mid-June, which should ease fuel surcharges, but automotive importers and parts shippers face elevated freight and full vessels into July, a cost that is layered on top of the tariff pressure already in the chain.