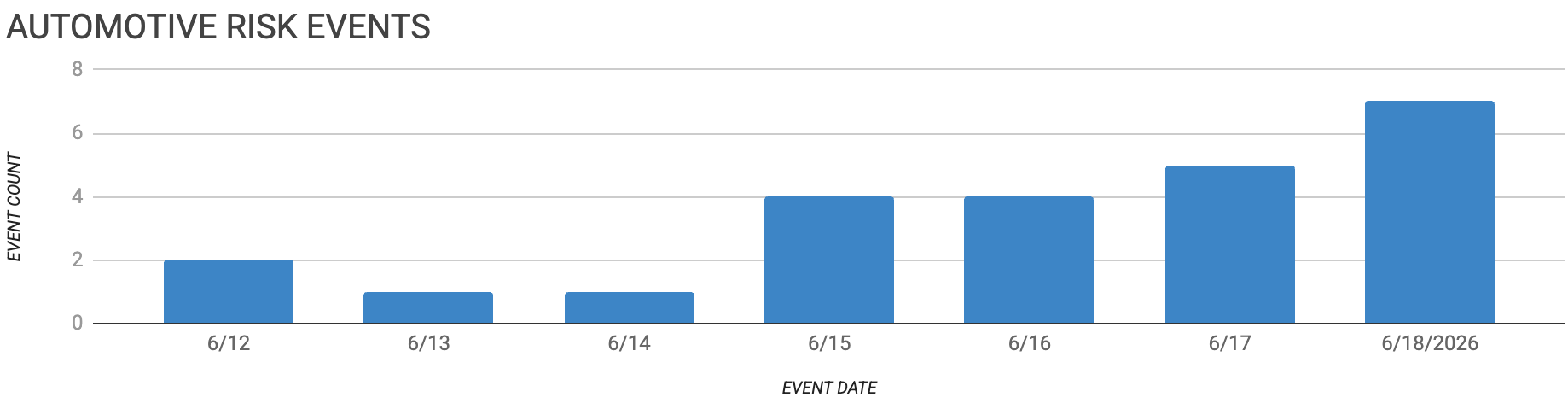

Automotive Supply Chain Risk Digest #487

June 12 - 18, 2026, by Elm Analytics

Dear Reader,

Most teams can name their direct suppliers. Far fewer can say who sits two, three, or four tiers down, and that gap is where this week’s risk lives. What counts as “your chain” is also widening fast. It is no longer just parts and the firms that make them.

It is now local-content thresholds that determine whether a vehicle qualifies for tariff relief, as with BYD’s push for 50% local content in Brazil and the EU’s proposed content rules reshaping where Chinese brands can build.

It is the lines of code in a connected vehicle, where Ford must seek federal authorization to keep selling a Lincoln whose software is written in the US but installed in China. Your exposure now runs to ownership structures, software origin, and the financial health of firms you may never have heard of.

Knowing all of this by spreadsheet is no longer realistic, and you cannot manage a risk you cannot see. Mapping the chain beyond your direct suppliers, surfacing the ownership links and dependencies that create hidden exposure, is what turns a surprise into something you saw coming. It is the problem we built supplyAware™ to help with, and it has rarely mattered more.

Best,

Nick Gaydos

Editor

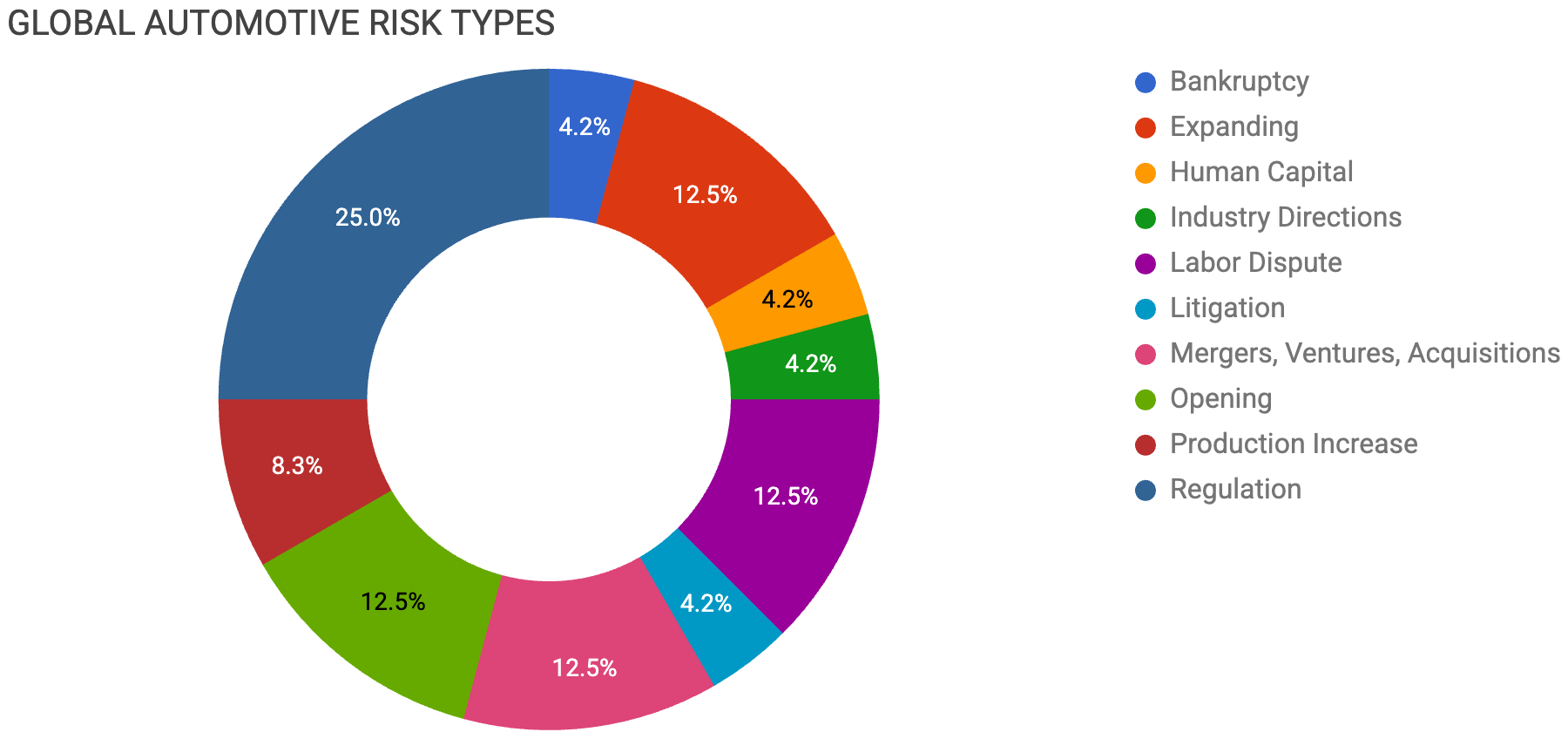

Contents

BANKRUPTCY

First Brands advances liquidation plan

EXPANDING

Hyundai weighs new Mexico plant

Volvo offers Geely European capacity

BYD expands Brazil battery output

HUMAN CAPITAL

Volkswagen accelerates German restructuring

INDUSTRY DIRECTIONS

Stellantis commits minicars to EVs

LABOR DISPUTE

Dauch strike ends with contract

Unifor enters difficult Canada talks

Ford Canada begins pattern bargaining

LITIGATION

OPmobility sues Marelli over secrets

MERGERS, VENTURES, ACQUISITIONS

Honda partners with QuantumScape

Geely continues asset consolidation

Principal Mineral acquires Isola

OPENING

Vulcaflex plans Auburn materials plant

Sungwoo chooses Monterrey battery plant

ALMAC converts Alabama factory

PRODUCTION INCREASE

Foxconn plans Polish EV production

Renault starts Brazilian Geely production

REGULATION

China revokes automaker licenses

Battery standards tighten in China

European capacity attracts Chinese automakers

UK weighs Nissan Sunderland support

EU approves US tariff deal

Connected-car rules pressure automakers

Bankruptcy

A US bankruptcy judge in Houston cleared First Brands to solicit creditor votes on a wind-down plan that funds lawsuits against its indicted founder, with approval set for July. The parts maker collapsed in September after lenders alleged it double-pledged assets as collateral, and once its $1.1B bankruptcy loan ran out in January, it leaned on prepayments from Ford and GM to keep parts flowing. It now sits $223M behind on administrative expenses, including to its unpaid suppliers who shipped parts after the filing.

Expanding

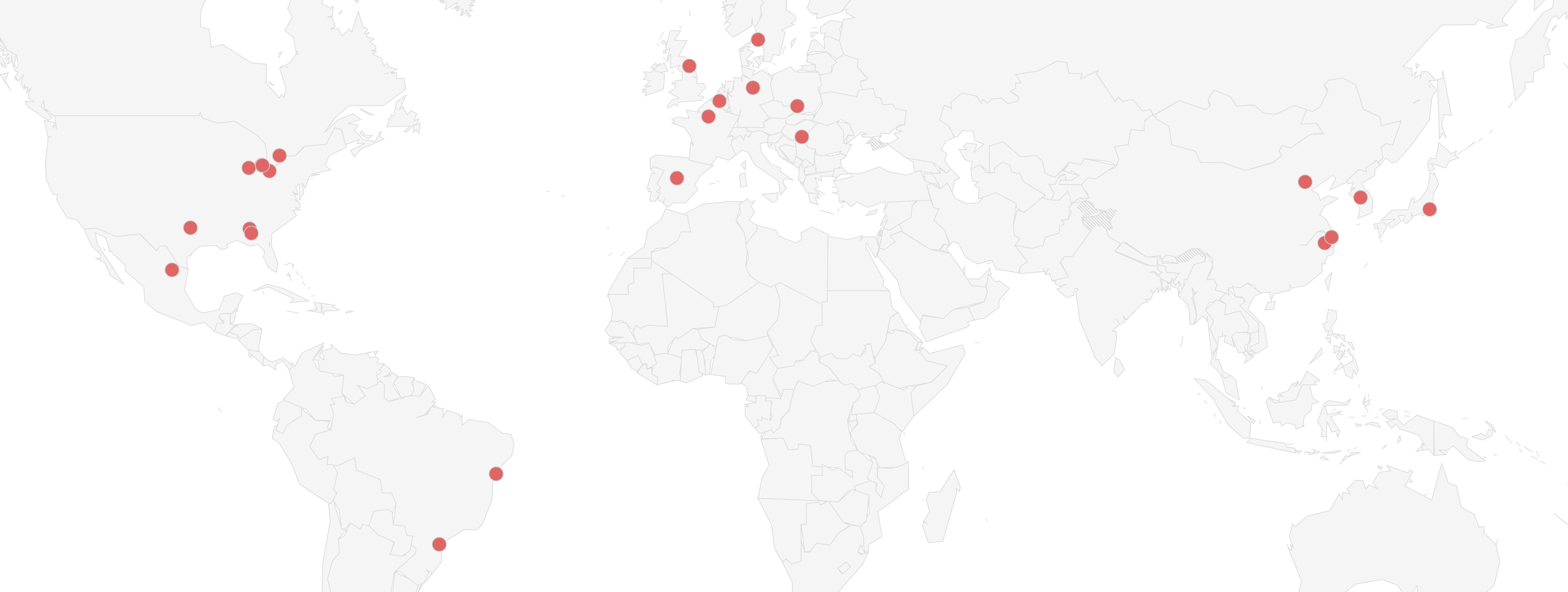

Hyundai is weighing a Mexican plant of more than $2B and 250k to 300k units a year, with any decision hinging on the USMCA review and a possible Mexico-South Korea trade deal. It already runs over $2.5B in Mexican operations, and a new plant would pull additional supplier capital expenditure to the site. Mexico's January jump in tariffs from 20% to 50% on imports from non-FTA countries already hits roughly 8 out of 10 vehicles Hyundai brings in, with the local CEO saying that more than half of last year's profit will go toward absorbing the impact. The plant reads as a hedge against that tariff wall, and the conditional framing signals Hyundai will not commit greenfield capital until USMCA terms are clear.

Volvo CEO Hakan Samuelsson has offered the automaker's European plants to build for its Geely siblings, Zeekr and Lynk & Co, calling existing capacity a faster, cheaper route than a greenfield site. Volvo runs factories in Torslanda, Sweden, and Ghent, Belgium, with a third opening in Kosice, Slovakia next year, and any could host sibling production. Local builds would let Geely sidestep the EU's 18.8% tariff on its China-built EVs, which adds to the standard 10% duty, though Ghent qualifies only if Volvo cuts its labor and energy costs. This is the brand-specific facet of the wider Chinese capacity scramble covered below.

BYD is scaling up battery production in Brazil to raise local content in its Brazil-built cars to 50% by the start of 2027. It will invest about $1.08B in its Camacari plant in Bahia and up to $98M in a new battery energy storage line, and will decide within 90 days whether to site that line in Manaus or build a new one. Brazil is the clearest test outside China of BYD's vertical-integration model, building batteries, vehicles, and now grid storage in one footprint, which compresses the market for any Tier 1 hoping to supply the same content locally.

Human Capital

Volkswagen is pushing ahead with a restructuring targeting $6.9B in annual net savings by 2030, having already cut about $1.15B through bargaining and downsizing, and planning to eliminate roughly 50k German jobs by 2030. Factory costs at its German sites fell more than 20% on average in 2025 as it right-sizes for stable rather than growing volumes. The move follows BMW's outlook cut due to a weakening China, feeding concerns that profit warnings are building across the sector. A structurally smaller VW means fewer programs and lower volumes to bid on, with the pain falling on Tier 1s and Tier 2s tied to legacy combustion platforms.

Industry Directions

Stellantis is dropping multi-powertrain versions of its next-generation minicars, committing to electric-only E-Car models priced at $17.4k, which would undercut nearly every EV in Europe. The two models, a Fiat and a Citroen 2CV remake, will use a dedicated platform built with partners, possibly including Leapmotor, with which Stellantis already shares production sites in Spain. Locking the entry segment to a single powertrain sharply narrows the supplier set, favoring partners capable of meeting aggressive EV cost targets and sidelining the mild-hybrid and ICE suppliers that currently share these platforms.

Labor

UAW Local 2093 has ratified a four-year contract with Dauch Corporation, ending a 10-day strike at the driveline supplier's Three Rivers, Michigan, plant with 80% approval. The deal delivers a 36% wage increase to $30 per hour by 2030 with no new health care concessions. It clears a near-term production risk for General Motors, which relies on Dauch driveline parts, and extends the run of UAW wins, resetting Tier 1 labor cost assumptions.

Unifor enters summer talks with the Detroit Three in Canada under conditions its leaders say could rival the 2008-09 collapse. Local 444 President James Stewart cited trade instability, tariffs, and USMCA uncertainty as forces the union cannot bargain away, even as workers expect gains after years of inflation. He signaled the talks will focus less on wages than on securing sufficient production to justify long-term investment in Canadian plants, including the idled Brampton Assembly Plant, and on floating partnerships to build offshore automakers' vehicles in Canada under different nameplates.

Ford Canada opens bargaining on June 22 as Unifor's pattern target, chosen because it maintained its Canadian investment through 18 months of trade upheaval. It has about 5,000 unionized workers and recently invested nearly $3.65B to retool Oakville for Super Duty, including an Essex Engine Plant expansion in Windsor, and now wants added operational flexibility in return. The Ford pattern cascades to GM and Stellantis before the September 20 expiry, so whatever production-security language Unifor wins here becomes the template for the whole Canadian footprint.

Litigation

OPmobility, formerly Plastic Omnium, has sued bankrupt rival Marelli for trade secret misappropriation, alleging it poached former OPmobility CEO Laurent Favre despite warnings the hire could expose confidential information. Supplier distress reshuffles talent as well as assets, and a bankrupt competitor pulling in a rival's recent CEO raises real questions about where proprietary cost and program knowledge lands.

Mergers, Ventures, Acquisitions

Honda has signed a multi-year joint research agreement with QuantumScape to develop and manufacture solid-state batteries, making it the developer's second major OEM partner after Volkswagen. It follows a hands-on benchmark against competitors and builds on Honda's own pilot solid-state line at Sakura, Japan, which began in early 2025, with QuantumScape's Cobra separator process intended to enable gigawatt-hour-scale output. The value lies more in the manufacturing method than in the chemistry, since scaling separator production has been the unsolved problem, and a second OEM signing points toward industrial viability even as Honda trims its broader EV plans.

Geely chairman Eric Li says the group will continue to close, merge, and restructure redundant entities to concentrate resources under its core listed platform, Geely Auto, extending the consolidation that has already absorbed Zeekr and Lynk & Co. Zeekr completed its merger and delisted from the New York Stock Exchange in December. A tighter Geely means fewer but larger platform programs and consolidated purchasing leverage, favoring scale suppliers and squeezing those serving niche sub-brand volumes.

Principal Mineral, a Dallas firm building a US printed circuit board supply chain, is acquiring Cerberus-backed Isola Group, a maker of PCB components for vehicles, aircraft, and AI servers, and has raised about $280M to expand. PCBs sit deep in the automotive electronics stack, and a domestic source matters as OEMs work to decouple from Chinese-origin components, a pressure that the connected-vehicle software rules are now sharpening.

Opening

Italian synthetic leather maker Vulcaflex will build its first US plant in Auburn, Alabama, a nearly $70M site with 130 jobs supplying interior materials for vehicles built across the US, Canada, and Mexico. It joins recent Auburn supplier investments, including Kamtec Auto USA and DUCK IL USA. The clustering of foreign interior and component suppliers around Alabama's OEM base reflects the localize-to-serve logic, putting Tier 1 and Tier 2 capacity closer to assembly to limit tariff and logistics exposure.

South Korea’s Sungwoo Corp will invest $18M in a Monterrey, Nuevo Leon plant to produce safety components for rechargeable batteries, as well as automotive electronics and storage parts, with completion targeted for the first half of 2027. It had weighed a US site but chose Mexico on labor cost, skilled workers, and infrastructure, serving both US and Mexican markets from there. Sungwoo's choosing Mexico over the US, even for battery-safety content, runs counter to the US-reshoring trend elsewhere in this issue, a reminder that cost still wins when the tariff math allows.

ALMAC, a supplier of aluminum EV components, has acquired a 300k ft² former building-products plant in Eufaula, Alabama, with work starting late 2027 and about 100 jobs across two shifts. It cited proximity to Hyundai and Kia assembly, taking over a site Nucor Buildings Group vacated last year for Texas. The reuse of an idled building for EV aluminum production is the brownfield version of the same nearshoring pull that is drawing suppliers to Alabama’s OEM cluster.

Production Increase

Foxconn and state-backed ElectroMobility Poland have confirmed a venture to build three mid-range electric SUVs in Jaworzno from 2029, at a plant designed to produce 400k vehicles a year, with Poland lending roughly $1.23B from EU recovery funds, and a paired semiconductor factory also planned. Foxconn's move from contract electronics into European vehicle and chipmaking is a credible new entrant, and a 400k-unit platform built on reference designs could become an open manufacturing base that reshapes where mid-market EV suppliers invest.

Renault Geely do Brasil has started local production of the Geely EX2 EV at the Ayrton Senna plant in Parana, its second Geely model after the EX5 plug-in hybrid. Geely shifted from importing after taking a 26.4% stake in Renault do Brasil in November 2025, thereby gaining access to its manufacturing and dealer network. This mirrors Geely's European playbook of buying into an established automaker's capacity rather than building greenfield, thereby deepening localization and sidestepping import friction in priority markets.

Regulation

China's MIIT has permanently revoked the production licenses of eight automakers, including FAW Xiali, Brilliance Auto, Zotye, and Lifan, and ordered their lines sealed. Most leaned on rebadging with minimal R&D and could not meet tightening emissions and intelligent-driving rules as passenger car retail sales fell 19.5% year on year from January through May. GAC AION and Geely absorbed some freed plants and teams, turning a slow shakeout into reallocated capacity.

The same consolidation pressure runs through China's two mandatory safety standards, which take effect July 1. The battery rule replaces the five-minute pre-fire alarm with a no-fire-or-explosion requirement, adds a bottom-impact test, and requires cells to survive a short-circuit test after 300 fast-charge cycles, which analysts expect will lift battery costs and favor compliant makers like CATL and BYD. It is a regulatory filter on the supply base: cell makers that cannot certify lose program eligibility, accelerating the shakeout that the delicensing just formalized.

Chinese-owned automakers are racing to lock in European factory space before the EU's proposed Industrial Accelerator Act, which would impose foreign-ownership caps, local-content rules, and approval requirements on large investments by countries that hold over 40% of global capacity in key sectors. With the act unlikely before mid-2027, executives say there is no time for greenfield, leaving brownfield takeovers of idle European capacity as the only fast route, and there is plenty:

Jefferies puts Stellantis at about 1.6M unused units against 2019 levels and Volkswagen at another 800k, amid closures at Audi Brussels, Nissan Barcelona, and Ford Saarlouis.

BYD has opened a 300k-capacity plant in Szeged, Hungary, and is scouting Spain and Italy,

Stellantis is lining up Leapmotor in Zaragoza and Dongfeng's Voyah in Rennes

Chery is building at Nissan's former Barcelona plant with Ebro

SAIC's MG will open a 120k plant in Galicia

Geely is in talks to buy part of Ford's Valencia site

Chinese brands have gone from 0.5% of European market share in 2021 to nearly 10% in spring 2026, and Jefferies estimates the deals could eventually put more than 2M cars a year on European production lines. For European Tier 1s, this is a rare demand-side bright spot, but the IAA's local sourcing and IP licensing conditions will determine who actually wins the content.

That scramble reaches Britain, where the government is in advanced talks to give Nissan financial support in return for a long-term commitment to its Sunderland plant. Any aid, via grants, tax breaks, or subsidies, would be tied to new models and to protecting the roughly 6k jobs at a plant that built over 35% of UK-made cars last year, even as Nissan cuts 15% of its global workforce. The commitment is expected this summer, timed to Britain easing its EV mandate, and Nissan has also signed a pact with Chery to study the production of Chinese vehicles on one of Sunderland's two lines. Both moves point in the same direction: Sunderland's survival now depends on filling the lines with someone's volume, whether through a softer mandate or a Chinese partner.

The European Parliament has approved the implementation of last summer's framework trade deal with the US, locking in a 15% US tariff cap on EU imports in exchange for the EU dropping tariffs on all industrial goods. A sunset clause expires at the end of 2029, and the EU can suspend its concessions if the US keeps steel and aluminum derivative tariffs above 15% past the end of 2026 or breaches the cap. Two Section 301 probes still hang over the pact, one on forced-labor enforcement that could add a 10% EU tariff and one on excess capacity. The 15% ceiling is the planning baseline industry wanted, but the steel and aluminum carve-out keeps real exposure on high-metal-content parts, and the Section 301 probes mean the number is not settled.

On a second trade front, Ford and others are scrambling for US authorization to keep selling models caught by the ban on Chinese software in connected vehicles. Ford has asked Commerce to keep importing its China-built Lincoln Nautilus, whose software is written in the US but installed in China, with software rules biting for model year 2027 and hardware rules for 2030, and the rules also cover Chinese-owned automakers like Volvo, which already has an authorization. The harder phase is hardware: GM has told some suppliers to purge China-sourced parts by 2027, and Pirelli has started US production after warning that a product risked a ban over a Chinese shareholder. The scramble shows how deeply US auto supply chains are wired into China, and the 2030 hardware deadline is the one that forces real resourcing, giving domestic plays like the PCB reshoring above a clearer runway.