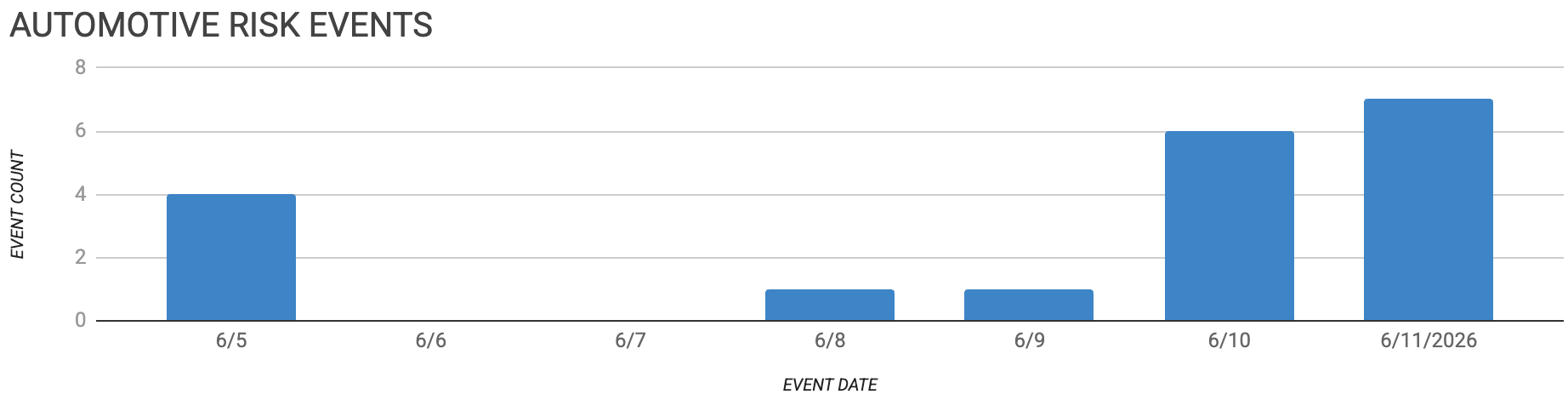

Automotive Supply Chain Risk Digest #486

June 5 - 11, 2026, by Elm Analytics

Contents

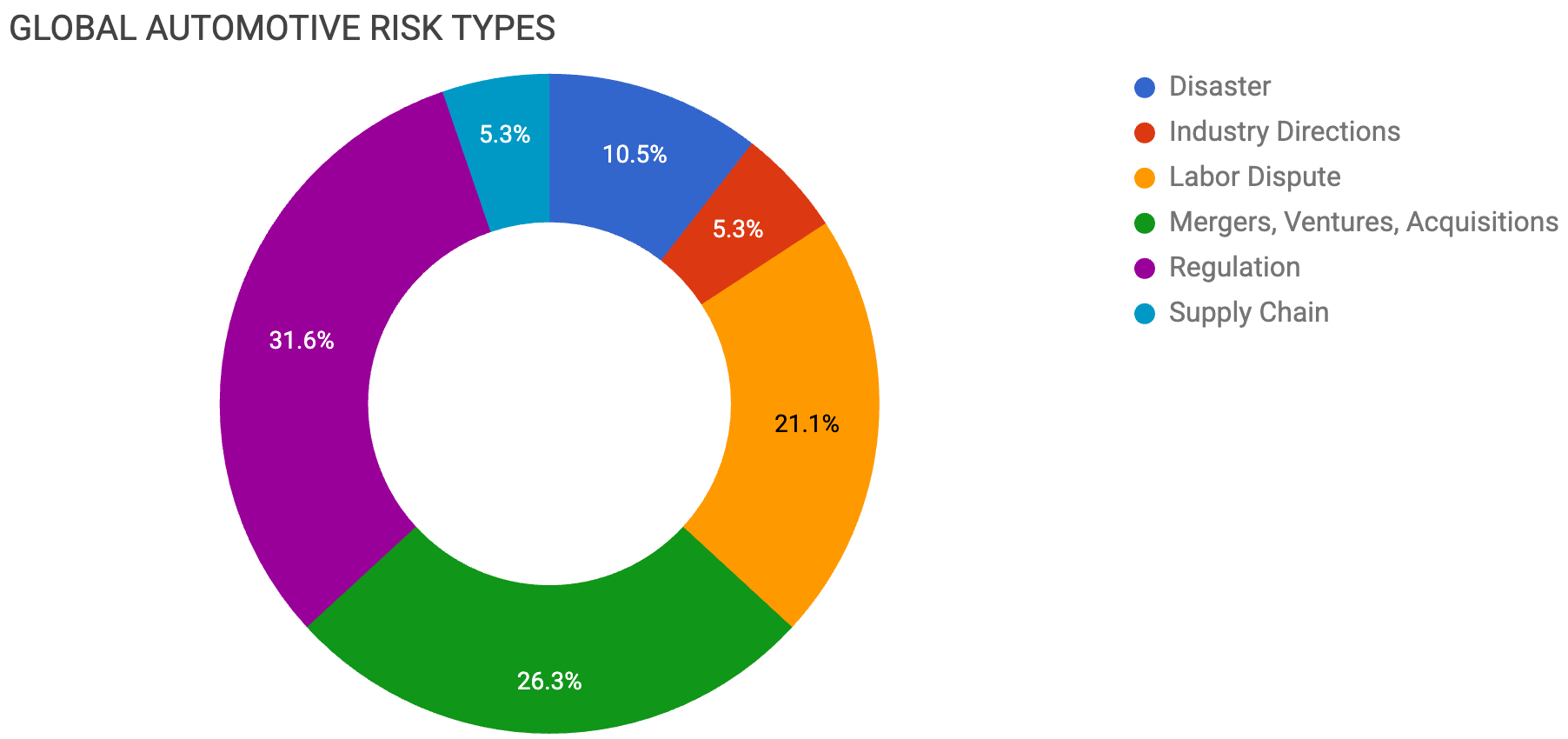

DISASTER

Novelis Oswego hot mill restarts

Hyundai Chennai resumes after fire

INDUSTRY DIRECTIONS

Mexico advances Olinia micro-EV plan

LABOR DISPUTE

Dauch strike ends with agreement

Plasman strike idles Volvo Gent

OPmobility dispute threatens JLR supply

Unifor enters Detroit Three talks

MERGERS, VENTURES, ACQUISITIONS

Dana buying Eaton mobility business

Nio partners with GigaDevice chips

Changan exits Ford EV venture

BYD pauses Turkish plant plan

BYD eyes European brownfield factory

REGULATION

OEM partnerships become a platform necessity

Trump uncertainty clouds USMCA renewal

Mexico challenges higher US tariffs

Japan automakers absorb policy costs

China meets to curb automaker price war

China's indium controls tighten supply

SUPPLY CHAIN

BASF warns of upstream shortages

Disaster

Novelis has restarted the hot mill at its Oswego, New York, plant, the largest domestic source of aluminum sheet for the US auto industry. This comes nine months after fires in September and November forced it offline. The shutdown pushed Ford to project $1.5B to $2B in one-time costs to secure alternative aluminum until the plant reaches full throughput later this year. GM and Stellantis are also dependent on the Oswego sheet for body panels. The restart eases a major sourcing crunch, though Novelis is still ramping, and the relief is only partial. Aluminum has climbed roughly 30% in 2026 due to the 50% US import tariff and supply risks in the Middle East tied to the Strait of Hormuz. Novelis, a unit of India's Hindalco, is separately adding capacity in Alabama. This would deepen the domestic supply once online.

Hyundai Motor India is restoring output at its Chennai Plant 1 after a June 1 fire at supplier Mobis India's Sriperumbudur facility disrupted the supply of chassis, cockpit, and front-end modules. Full normalization is expected by June 22. The blaze started in the scrap yard and spread to two units. This left Hyundai sourcing the affected parts from alternate locations, while its Pune and second Chennai plants ran without major interruption. Hyundai expects to recover most of the lost production next quarter. The episode is a reminder of how concentrated module sourcing magnifies single-site risk. These integrated assemblies have no quick second source, so one fire idled a line for weeks.

Industry Directions

Mexico’s government-backed Project Olinia has entered negotiations with more than 10 business groups to form a public-private partnership for a low-speed electric microvehicle. The project targets 50k units by 2029, with commercial deliveries expected from summer 2027 at roughly $8,400. The program is pursuing a 75% domestic content rate and plans to build a dedicated battery assembly plant in Mexico. This plant would import LFP cells, build a proprietary battery management system, and integrate packs locally. A cargo variant is slated for July 2026. Because Mexico lacks the scale of competitive cell manufacturing, the near-term build remains import-dependent for cells. Olinia is localizing pack assembly and trying to seed a domestic micro-mobility supplier base. The vehicle does not meet Mexico’s NOM-194 safety standard, so the government is drafting a new low-speed category. That change would also open the segment to other manufacturers.

Labor

UAW Local 2093 reached a tentative four-year agreement with Dauch Corporation on June 10, ending the Three Rivers, Michigan, strike that began June 1. This resolves the near-term risk to General Motors' pickup output posed by last month's authorization votes. The deal lifts top production wages to $30 per hour by 2030, a 36% increase over four years from the current $22 top rate. The agreement now goes to the plant's 1k members for ratification. The walkout never reached GM's lines. Dauch had stockpiled axles since January, leaving a roughly two-week buffer. It kept output going with about 250 nonunion staff and temporary contractors. The Three Rivers plant feeds axles to GM's profitable heavy-duty pickups in Flint and midsize trucks in Missouri, and also makes Chrysler Pacifica parts and Nexteer linkage components. Dauch is investing $133M at Three Rivers as tariffs push production onshore. Its footprint expanded with the recent $1.4B Dowlais takeover, giving it more flexibility in future disputes even as labor costs rise.

The same supplier-labor dynamic played out in Belgium, where automotive supplier Plasman reached a draft agreement to end a strike at its Ghent plant after walkouts halted production earlier in June. The dispute flared when an expected new order was not assigned to the Ghent site. The stoppage starved Volvo Car Gent of parts, forcing it to suspend final assembly and lay off roughly 4k workers. The cascade is what matters here. A single supplier’s work stoppage idled an entire OEM assembly plant within days. There was little buffer between a parts strike and an assembly shutdown.

In the UK, the pay dispute at French supplier OPmobility is escalating toward a strike ballot at its Warrington plant. The site produces exterior body panels, bumpers, spoilers, and tailgates for Jaguar Land Rover's nearby Halewood factory. Roughly 80% of Unite members rejected the company's final offer. After that, OPmobility cut shift allowances and moved to four-day workweeks. These changes dropped take-home pay by about $670 a month. Unite is now preparing a formal strike ballot. If a walkout lands, Halewood faces the same single-source exposure that idled Volvo Gent. OPmobility's molded exterior modules are not quickly resourced.

Canada’s Unifor heads into Detroit Three bargaining on June 22, refusing any concessions. Two Ontario assembly plants are idle, and US tariffs erode the competitiveness of Canadian production. The union picked Ford to set the pattern, citing its commitment to Canadian operations. Ford includes engine output at Windsor and Essex, and a near-complete retooling of Oakville for heavy-duty pickups. The backdrop is grim for the other two. Stellantis halted its Brampton retooling in February 2025 and moved the planned product to the United States, leaving the plant idle. GM cut a third shift at Oshawa and idled its CAMI plant in Ingersoll after pulling the BrightDrop program. With contracts expiring on September 20, the collision between tariff-driven production migration and a no-givebacks stance puts the Canadian assembly footprint and the Tier suppliers around it under real pressure.

Mergers, Ventures, Acquisitions

Dana will acquire Eaton's mobility business in a deal valued at about $5.1B. The combined supplier will have an enterprise value of over $10B and will operate as Dana Inc. The merger pairs Eaton's commercial-vehicle transmissions, engine, and emissions lines with Dana's powertrain, thermal, and sealing technologies. They target $250M in run-rate cost synergies within 24 months of the expected Q1 2027 close. The deal lets Eaton shed an underperforming automotive arm to concentrate on electrical and aerospace markets.

Nio signed a co-development partnership with Chinese chipmaker GigaDevice, a supplier of NOR Flash memory and microcontrollers. They will jointly design automotive-grade chips and next-generation electrical architectures for smart cockpit and driving systems. The deal advances CEO William Li’s campaign to slash semiconductor variety. Li flagged that Nio’s ES9 SUV carries more than 1k chip types and over 4k chips. Nio aims to cut the number to 400. The move fits the broader margin squeeze in China’s EV sector. Vertical chip co-design and standardization are becoming cost-survival tools. Li has pegged the potential industry-wide savings from standardizing cells and chips at roughly $14.8B.

Changan Automobile is listing its 40% stake in Changan Ford New Energy for sale at a reserve of about $22.8M. This would end its direct equity in the EV joint venture barely two years after launch. The venture, formed in 2023 to electrify the Changan Ford brand, has seen operations grind to a halt. It sold just 35 Mach-E units in 2025 and ceased Ford-brand sales and service last October. The retreat tracks Ford's broader pullback, which included canceling large EVs and dissolving its EV division by the end of 2025. Ford is also taking direct control of China distribution. The unwinding is another marker of foreign-Chinese EV joint ventures, stranding capital as Western OEMs scale back electrification and Chinese domestic brands take the volume.

BYD has put its planned Turkish plant on hold and is now hunting for a second European production site. Deputy CEO Stella Li named Hungary the top priority and a second facility the next in line. The roughly $1B Manisa project near Izmir was announced in mid-2024 and slated to open by late 2026, but it has not broken ground and has no timeline. The driver is not tariffs, since Turkey’s customs union with the EU already exempts it. Instead, the EU’s proposed ‘Made in EU’ local-content rules for publicly procured and subsidized vehicles are shaping plans. Germany has signaled it will fold these rules into its EV subsidies. BYD’s first European plant, in Szeged, Hungary, has itself slipped to Q4 2026, about a year late, with equipment still being installed.

For the second site, BYD wants a brownfield rather than new construction, with Spain on the shortlist. Advisor Alfredo Altavilla framed the logic plainly: the Made in Europe rules would bite before any greenfield plant could come online. Taking over and refurbishing an existing factory is the only fast route. That demand meets ready supply, as Stellantis has openly pitched leasing its underused European plants to Chinese automakers, including Leapmotor and Dongfeng. BYD's European sales passed 100k units in May, up 270% from last year. The brownfield-takeover pattern points to Chinese OEMs absorbing Europe's surplus assembly capacity rather than adding to it, reshaping who runs the continent's idle plants.

Regulation

A Boston Consulting Group report argues that partnerships in platforms, software, and electrification have become essential as OEMs face flat sales and rising technology costs. Excess capacity in China and Europe forces OEMs to launch more variants on fewer platforms at lower per-model volume. The newer wrinkle is the direction of travel. Rather than absorbing Western expertise, Chinese automakers now offer leading-edge technology and rapid development. Partners co-innovate in China before globalizing. Stellantis is localizing European output with Leapmotor and Dongfeng to build cheaper EVs. Volkswagen turned to Rivian and Xpeng after its Cariad software arm failed to deliver. For suppliers, the through-line is consolidation. Fewer, larger shared platforms mean higher stakes for each platform win. More Chinese-origin architecture and software are entering Western vehicle programs.

President Trump said on June 10 that he was unsure he would renew the USMCA, unsettling the renegotiation just as talks with Mexico got underway. The pact matters to automakers chiefly because last year's exemption of USMCA-compliant goods from most US tariffs has been the main shield for the North American auto trade. In the first round of negotiations, US officials floated raising the share of a vehicle that must be American-made to qualify for those benefits. The risk for suppliers is twofold. A failure to renew would expose cross-border auto flows to the broader tariff regime, while a tougher rules-of-origin standard would raise compliance costs and could strand content sourced outside an expanded domestic threshold.

Beneath those renewal politics sits a concrete grievance Mexico brought to the table. Its vehicles face a higher effective US tariff than imports from Japan or South Korea. An internal document put the average effective rate on Mexican-built vehicles near 19%, compared with the flat 15% that Japan and Korea secured last year without any regional-content strings, so a $50k vehicle from Mexico carries about $9,375 in duties versus $7,500 from those countries. USMCA’s duty-free path requires 75% North American content, plus labor and value rules, and verifying origin across as many as 18k components per vehicle adds an estimated 3% cost penalty. Nissan has already announced it will end production at its COMPAS plant in Aguascalientes. The asymmetry inverts the logic of preferential access. The supposedly favored regional bloc now faces stricter rules and higher effective duties than those negotiated with outsiders, creating structural pressure to reassess Mexico's manufacturing footprint.

US policy swings have cost Japan's six major automakers up to $27.58B in the just-ended fiscal year across tariffs, EV write-downs, and emissions-rule reversals, a tally that could exceed $40B by March 2027. Tariffs are the largest piece, with Toyota projecting $17.22B and Honda $15.23B over the two fiscal years ending March 2027, hitting their US, Mexican, and Canadian production alike. The EV retreat drove Honda to book $9.05B in write-downs and post its first annual loss in roughly 70 years, while Nissan retooled its Canton, Mississippi, plant to build trucks rather than EVs. The relaxed US emissions rules cut both ways, letting Nissan and Mazda recoup set-aside penalty funds while forcing Subaru and Mitsubishi to write off now-unneeded emissions credits. For the supply base, the takeaway is volatility in volumes and program plans. Each portfolio reset and footprint shuffle reorders supplier allocations, and the costs are large enough to squeeze supplier support and pricing flexibility.

Two Chinese regulators summoned automakers to rein in a price war driven by below-cost pricing, demanding compliance with pricing and anti-dumping rules amid softening domestic demand. May passenger-vehicle retail fell 22.1% year on year to 1.51M units, with NEV sales down 7.5% in their fifth straight monthly decline, and dealers are cutting orders to avoid inventory buildup. The pressure is flowing offshore. NEV exports jumped 112.6% in May to 424k units, a record 54% of China’s passenger-vehicle exports. The combination of a regulated price-war truce and surging exports points to overcapacity, intensifying volume and pricing pressure on Western OEMs and the supplier bases tied to them.

China's export licensing controls on indium phosphide, in place since February 2025, are tightening the global supply of the compound semiconductor, whose lasers and photodetectors are used in automotive lidar and other optical sensing systems. The auto sector's volumes are modest, but the chokepoint is real. China produces 70% of the world's indium, and AXT, which makes most of its InP substrates in China, is caught in a permit backlog, with new non-Chinese capacity two to three years out. The exposure that matters is the playbook, not the volume. This is the same materials-chokepoint approach Beijing used on rare earths, which already disrupted auto, semiconductor, and aviation chains, and the sector's reliance on Chinese magnets and battery materials.

Supply Chain

On the same upstream-risk theme, BASF CEO Markus Kamieth warned that the US-Israel conflict with Iran is raising the odds of material shortages that could halt tightly run supply chains, including car production. He pointed to the emerging scarcity of inputs such as sulfur and helium, while BASF supplies coatings, plastics, catalysts, and battery materials across the auto industry. Purchasing teams at Volkswagen and Mercedes-Benz are working to mitigate exposure, but Kamieth noted that disruptions that start far upstream in chemicals or basic materials are hard to detect until they bite. The warning frames a second-half-2026 downside risk that is structurally hard to hedge, since a single missing basic input can idle assembly lines that depend on thousands of components arriving on time.