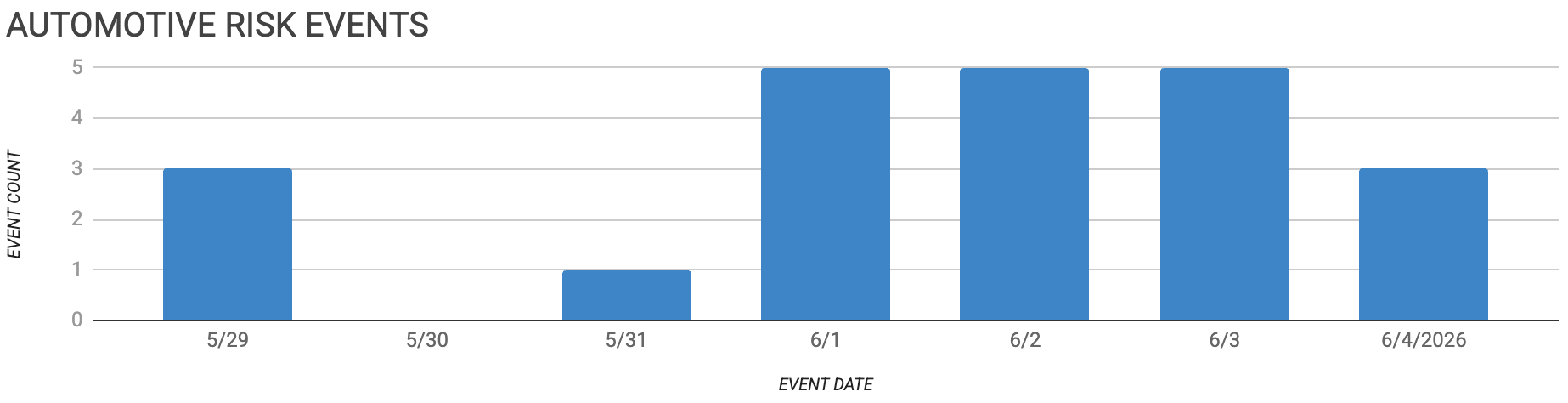

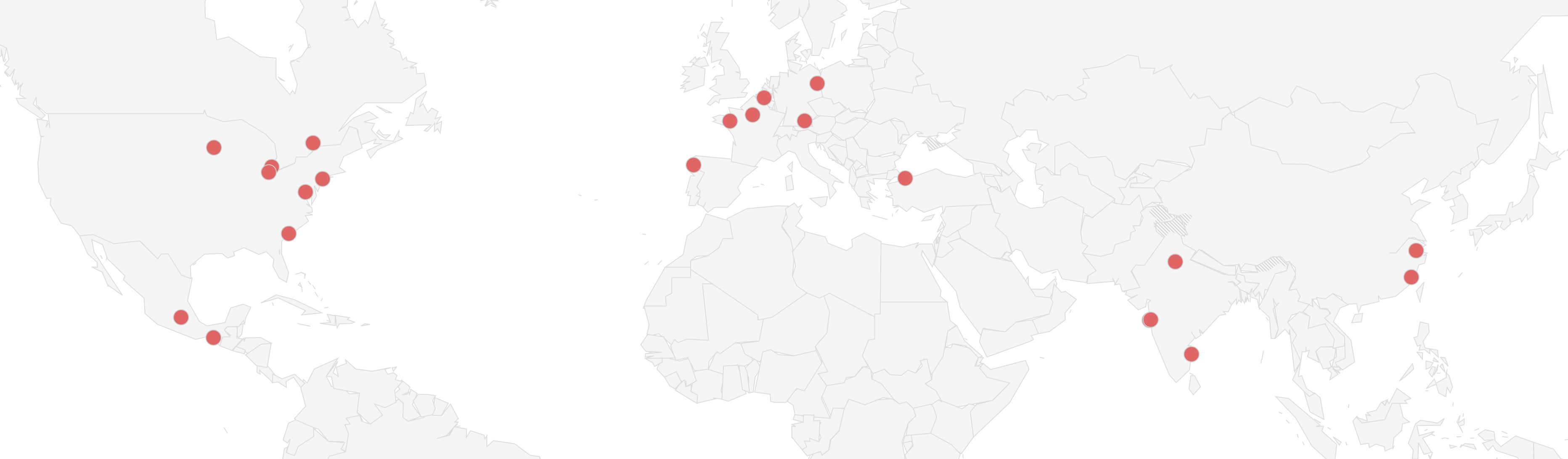

Automotive Supply Chain Risk Digest #485

May 29 - June 4, 2026, by Elm Analytics

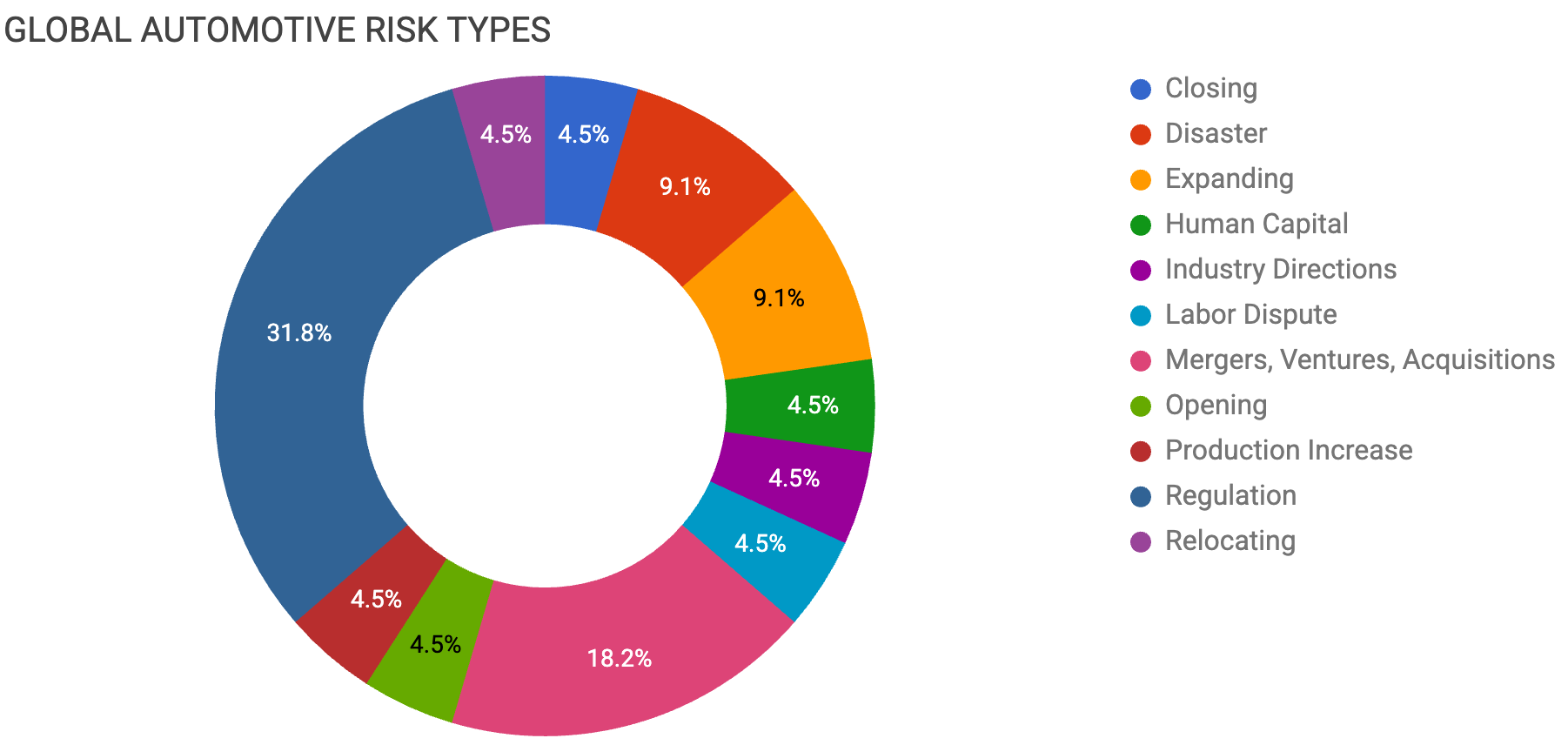

Contents

CLOSING

Autoliv exits Turkish airbag production

DISASTER

Hyundai Mobis Chennai building destroyed

Minda Noida fire damage under review

EXPANDING

OPMobility plans Ohio exterior-parts plant

Charleston expands automotive port capacity

HUMAN CAPITAL

Michelin, Renault cut French costs

INDUSTRY DIRECTIONS

Chinese OEM terms strain suppliers

LABOR DISPUTE

Dauch strike threatens GM axle supply

MERGERS, VENTURES, ACQUISITIONS

Tata licenses Chery EV platform

JTEKT sells Moroccan steering plant

Rheinmetall divests Power Systems unit

SAIC reduces Indian venture control

OPENING

SAIC plans MG factory in Spain

PRODUCTION INCREASE

Berlin builds Canada-bound Model Y

REGULATION

US eases metals-content tariff threshold

Section 301 proposal spares covered autos

Forced-labor duties threaten uncovered parts

Connected-car rules force China sourcing exits

US seeks stricter North American content

Mexico supplier gaps complicate compliance

Mexican auto exports fall sharply

RELOCATING

Nexperia adds US semiconductor production

Closing

Autoliv will close its only Turkish plant in Gebze and move production of seat belts, airbags, and steering wheels to undisclosed sites by mid-2028. This responds to weak demand in Europe, the Middle East, and Africa. The relocation will cost about $140M. The 2.2k jobs at Gebze are unlikely to be replaced elsewhere, given the outlook for demand. The site sits in the auto cluster east of Istanbul and supplies Ford, Hyundai, Mercedes-Benz, Renault, and Toyota. All assemble in Turkey, drawing on polyurethane foam for steering wheels and polyamide 6.6 for airbag fabric. The move continues cost-cutting under European operations head Magnus Jarlegren, who cut about 1.1k jobs across Germany, the UK, the US, and Italy in 2024. This is part of the 104k supplier job losses CLEPA has tallied over two years.

Disaster

A fire at Hyundai Mobis's Chennai plant destroyed a building that produced audio, navigation, chassis, and airbag components. Most of these parts are supplied to local Hyundai and Kia assembly plants. About 500 workers were evacuated with no casualties. Hyundai has disclosed a temporary production interruption while it assesses losses and secures alternative suppliers. Hyundai builds roughly 1M vehicles a year in India, including the Creta, Venue, and i20. Kia builds about 300k, including the Seltos and Sonet. With no second source named for the destroyed parts, the squeeze falls on in-line electronics and safety components. Requalifying a supplier takes longer than the dealer inventory cushion Hyundai is leaning on.

Auto components maker Minda Corporation disclosed a fire on May 30 at its plant in Sector 59, Noida, India, with no casualties, and the affected stock and machinery were insured. The company has not quantified the damage or the operational impact, which remains under assessment.

Expanding

OPMobility will build its 12th US plant in Rossford, Ohio, near Toledo, to produce exterior components, including bumpers, grilles, and tailgates, with output starting in the second half of 2027 and creating more than 500 jobs. The facility will run advanced injection molding, a double-sided paint line, and digital manufacturing, placing the supplier in a region the company says accounts for more than 40% of US vehicle production. The investment follows the opening of a North American headquarters in Troy, Michigan, and a stated goal to double US sales by 2030.

The South Carolina Ports Authority will expand roll-on/roll-off operations at its North Charleston Terminal by upgrading rail infrastructure and vessel parking, with work scheduled for completion in 2028. The Columbus Street Terminal already moves more than 250k vehicles a year, and motor vehicles and parts were the state's top export in 2025. The port handles just-in-time import and export flows for BMW, Mercedes-Benz, and Volvo, all of which are built in the state. Georgia's ports are investing alongside, having moved 779k units in 2025 and committed $100M to a new ro/ro berth. The added Southeast capacity backstops the BMW Spartanburg and Volvo Ridgeville export programs as volumes and vessel sizes climb.

Human Capital

Michelin and Renault are deepening cost cuts in France, days after President Macron promoted the country's ability to attract auto investment. Michelin plans to eliminate 1.5k positions, about 9% of its French workforce, over three years without forced terminations, citing an unstable economy and the burden of French taxes. Renault is in talks with unions to close its Villiers-Saint-Frederic light commercial vehicle engineering site, transferring most of its 400 employees to the Technocentre near Paris with no layoffs planned. Both face muted European demand and rising competition from lower-cost Asian rivals led by BYD.

Industry Directions

Chinese automakers are funding operations on suppliers' capital. They stretch payment cycles to 125-150 days, sometimes beyond 6 months. This contrasts with 36-60 days at Toyota, Volkswagen, and Mercedes-Benz. Combined with rigid annual price cuts averaging around 10%, these terms freeze supplier working capital. Pressure cascades down to Tier 2 and Tier 3 firms, which have the least bargaining power and the thinnest access to financing. Industry net margins have fallen from 7.8% in 2017 to 3.2% in early 2026. Even leaders' profits rely on NEV purchase tax breaks, which have now been cut to 5%. They also rely on the interest-free float from deferred payments rather than product strength. The structural risks for global buyers and joint venture partners are quality and continuity. Suppliers forced to front tooling and R&D costs while absorbing price cuts have little room for new investment. Some are cutting material standards and testing to survive, raising the odds that defects will propagate through a supply base on which much of the world now depends.

Labor

The strike authorization at Dauch Corporation has become a walkout. Hundreds of UAW workers left the line Monday at the Three Rivers, Michigan, plant, halting the supply of axles and axle tubes for GM's midsize and full-size pickups. GM has roughly two weeks of axle stock and no alternative supplier for the GM-specific parts, which comprise dozens of components and cannot be quickly substituted. As a result, its truck plants are running normally for now but face rising risk. The 970 hourly workers are seeking $30.50 an hour, up from $22, after a roughly 50% cut in 2008, while Dauch tries to keep the plant going with a skeleton crew of non-union contractors.

Mergers, Ventures, Acquisitions

Tata Motors will build its premium Avinya electric cars on Chery’s Freelander platform, which Chery developed with Jaguar Land Rover. Tata will build these cars in its new factory in Tamil Nadu, India. The first model is set to launch in 2027 as a kit from China for local assembly, with more parts sourced locally over time, and a second EV planned for 2029. This move replaced Tata’s dropped plan to use JLR’s own EMA platform, after JLR decided not to build EMA EVs in India. It also shows how Indian automakers are using licensed Chinese EV technology without buying stakes under India’s investment rules, meaning Tata will depend on a rival’s platform until it makes its own.

JTEKT will sell its Tangier subsidiary as part of a transfer of seven European-facing operations to Germany’s DUBAG Group, pending regulatory approval. The Moroccan plant is JTEKT’s first in Africa and the Middle East. It makes electric power steering systems and steering columns, targeting a capacity of 230k units. The plant was built for about $24M across roughly 122k ft² in Tanger Automotive City to supply Renault and the former PSA in Morocco. The divestment, alongside sites in France, the Czech Republic, Belgium, and the US, is part of JTEKT’s plan to restructure its European business back to profitability. For Renault’s Moroccan assembly, the change hands a steering-component source to a financial buyer. This introduces the continuity questions that accompany a private-equity carve-out.

Rheinmetall will sell its automotive Power Systems unit to investment firm Aequita for about $406M, completing its shift to a pure-defense company. The deal is expected to close in the fourth quarter, subject to approvals. Aequita will retain all of the unit's roughly 6.3k employees worldwide, and Rheinmetall has agreed to keep German workers and sites for three years after closing. The sale fits a broader European pattern of industrials rotating from automotive to defense amid the post-2022 military spending surge, and consolidates Power Systems' base under a buyer that also acquired Bosch's brake-components business in 2024.

SAIC will sell a further 10% of its Indian venture JSW MG Motor to partner JSW, cutting its own stake to 39% and making JSW the largest shareholder at 45%, after New Delhi’s investment curbs blocked SAIC from funding expansion. SAIC plans to reinvest about $63M of the proceeds to launch extended-range EVs and hybrids without changing its holdings. JSW MG is India’s second-largest EV maker and has committed up to $418M to more than double capacity to 300k units a year, though widening losses and gains by Mahindra are eroding its EV lead. The retreat mirrors BYD’s stalled $1B India plan and shows how the investment curbs are steadily transferring control of Chinese-built ventures to local partners.

Opening

While retreating in India, SAIC is planning its first European factory: a roughly $230M plant in Galicia, split between Ferrol and As Pontes, to build 120k MG-brand EVs a year. Construction starts in 2027, with first output in 2028, creating about 2.3k regional jobs, including 1k in direct manufacturing, and the company pledging to prioritize local component suppliers to meet EU content rules. Building inside the bloc lets SAIC sidestep the EU's tariffs on Chinese-made EVs. The Galicia build is one more Chinese OEM establishing EU production to convert a tariff disadvantage into a local supply base, with knock-on demand for regional Tier 1 and Tier 2 suppliers.

Production Increase

Tesla's Berlin plant has begun building the Model Y for the Canadian market. A US-Canada customs dispute triggered this shift. The plant promptly adapted its supply chains and homologation processes, thanks to high vertical integration. The site is scaling battery cell production from 8 to 18 GWh a year, enough for about 250k Model Ys. This will reduce its reliance on cells shipped from Texas and on complete batteries from Shanghai. Tesla reports Tier 1 localization in Europe at about 90%. The company holds a permit to expand the site to 1M vehicles per year. The cell build-out and regional sourcing are a kind of resilience play against the cross-continental battery logistics exposed in recent years. It is also a hedge against the same tariff friction now reshaping where vehicles get assembled.

Regulation

The US is trimming Section 232 tariffs on certain steel, aluminum, and copper goods effective June 8. From January 2028, imports qualify for a 10% rate if 85% of their content is US-made steel, aluminum, or copper, down from the current 95% threshold. Steel and aluminum otherwise remain at 50%. The lower domestic-content threshold eases qualification for derivative parts makers, while the equipment cuts mainly affect off-highway and HVAC applications rather than passenger-vehicle inputs.

Vehicles and auto parts already covered by the Section 232 auto tariffs would be exempt from new Section 301 duties that the administration proposed on June 2 on 60 trading partners over alleged failure to block forced-labor goods. Parts that comply with USMCA rules of origin are also carved out, but automotive products outside the auto parts tariff, including many electronics, interior materials, and sub-assemblies, would be hit. The duties could take effect in July, with comments due July 6 and a hearing July 7, and they follow the Supreme Court’s invalidation of the IEEPA tariffs, against which automakers and suppliers are already seeking about $19.9B in refunds.

The proposed rate is 10% for partners that restrict forced-labor imports, including Canada, Mexico, the EU, the UK, and Taiwan, and 12.5% for the rest, including China, India, Brazil, Japan, South Korea, and Vietnam. USTR frames the action as leveling the playing field for US producers undercut by cheaper goods produced with forced labor. For purchasing teams, exposure lies in uncovered automotive categories, where sub-assemblies and electronics could face a new 10% to 12.5% layer on top of existing tariffs, and the whole package is likely to face the same legal obstacles that felled the IEEPA duties.

Automakers are reworking supply chains ahead of the US ban on Chinese hardware and software in connected cars, which applies to software from the 2027 model year and hardware from 2030. GM has directed several thousand suppliers to source raw materials and parts outside China by 2027 and is moving the Chinese-built Buick Envision’s successor to Kansas in 2028, while Ford’s Lincoln Nautilus is still assembled in China through a Chinese joint venture. Volvo, majority-owned by Geely, secured special government authorization to keep selling connected cars, a pathway other exposed makers may need. The rule, finalized in January 2025, also applies to components from firms such as Tesla supplier Quectel and a Pirelli sensor-enabled tire flagged for its Chinese ownership. The burden falls on proving that connectivity hardware and embedded software are China-free across multi-tier supply chains, a documentation problem rather than a sourcing one for most Western automakers.

The US has demanded that Mexico raise regional content in North American vehicles to 82% from the current 75% to keep preferential tariff access, with half of that value required to come specifically from the US and no credit for Canadian parts. Presented during bilateral talks in Mexico City that excluded Canada, the proposal also raises the high-wage core parts calculation and would likely be handed to Canada as a take-it-or-leave-it term. USMCA’s current rules underpin nearly $1.6T in annual trilateral trade, and US negotiators signaled they intend to keep some tariffs on Mexican and Canadian goods even in a revised pact. A 50% US-value floor would force automakers and Tier 1 suppliers to re-source content away from Mexico and Canada toward US plants, a costly reshuffle of established North American sourcing.

The content push is exposing how thin Mexico’s lower-tier supplier base is. Industry groups count more than 1.1k procurement requirements worth $8.8B that local sources cannot meet in early 2026, with high-precision metallurgy the sharpest gap: only 7 domestic suppliers for aluminum high-pressure die casting, against demand from 24 OEM and Tier 1 projects. Roughly 70% of automotive steel and nearly all aluminum used in Mexico is imported, and high domestic financing costs keep Tier 2 and Tier 3 firms from scaling to qualify for major contracts. A federal development bank expects to open credit lines covering technical upgrades for up to 30% of small- and medium-sized suppliers by mid-2026, in line with a national goal to displace $14B in annual imports by 2030. Tighter USMCA content rules raise the stakes on these gaps: without deeper local capacity, the 82% proposal would be unmeetable from Mexican sourcing alone, pushing content toward the US as Washington intends.

US imports of Mexican vehicles and parts fell 11.3% in the first quarter, to $38.05B from $42.92B a year earlier, as Section 232 auto and metals tariffs reshaped North American trade flows. Passenger vehicles took the hardest hit, down 22% or $2.52B, and trucks fell 18.7%, while auto parts proved resilient at a 1.1% decline, evidence that integrated component flows are holding even as finished-vehicle trade contracts. The pattern was regionwide: total US auto imports from major suppliers dropped 15.1%, with Canada down 22.8%, Germany down 25.3%, and Japan and South Korea off by double digits. Sweden was the lone gainer, up 13.7% on Volvo’s US strength and its connectivity-rules authorization. Mexico is using the decline to argue that North America should be treated as one manufacturing ecosystem, but the resilient parts trade alongside collapsing vehicle imports shows that tariffs are biting hardest where assembly, not componentry, crosses the border.

Relocating

Nexperia will produce automotive power semiconductors in the US for the first time, partnering with Polar Semiconductor to make next-generation MOSFETs at Polar's wafer plant in Bloomington, Minnesota. The move comes as Nexperia risks losing its China operations: after the Dutch government seized control of the chipmaker in late 2025, its Chinese arm declared independence, and Nexperia Europe halted wafer shipments to China, disrupting the supply of the cheap basic chips that control brakes and windows. That standoff has already forced Nissan and Honda to cut production and pushed Bosch to curtail some output, while the owner, Wingtech, seeks $1.2B in damages and threatens to take over Nexperia's China business. Adding US wafer capacity hedges a supply line that runs through contested Chinese testing and packaging, but it does not resolve the near-term shortage now rippling through automakers and Tier 1 suppliers.