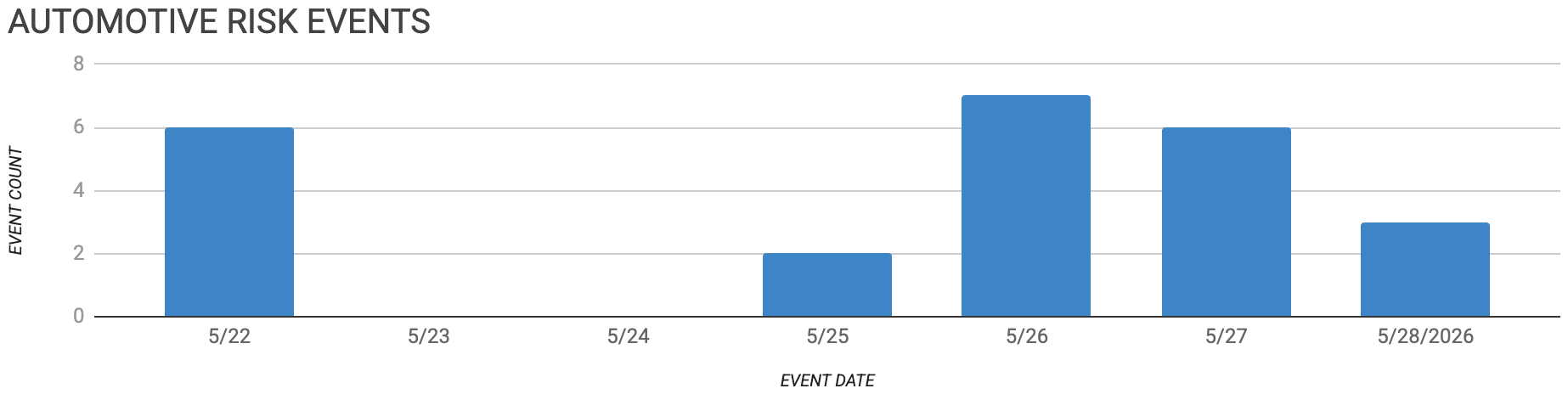

Automotive Supply Chain Risk Digest #484

May 22 - 28, 2026, by Elm Analytics

Contents

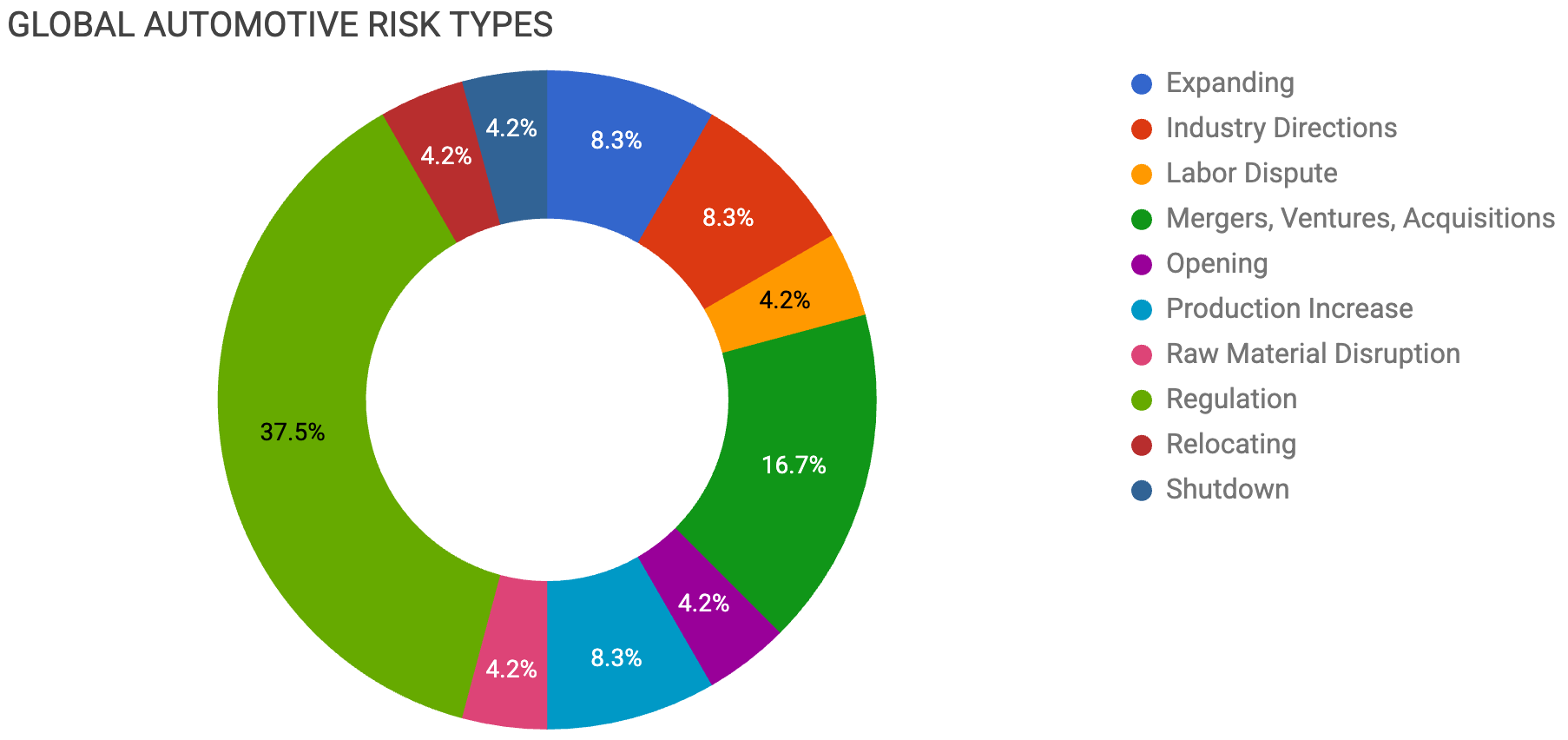

EXPANDING

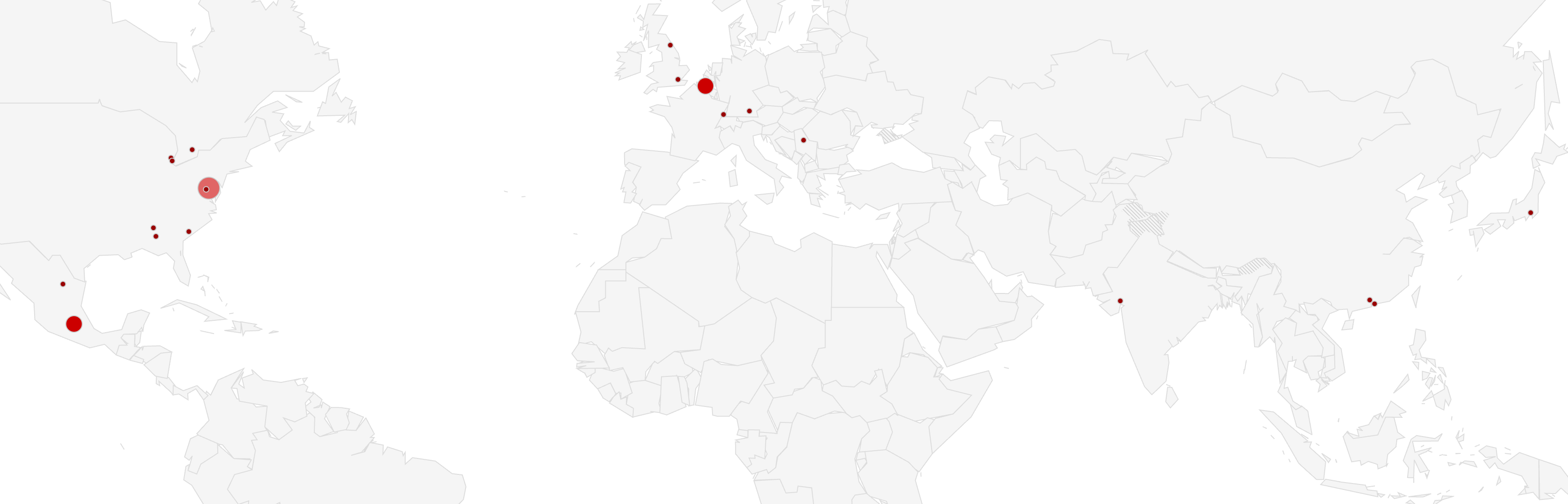

Tata expands Gujarat capacity

Stellantis expands Mulhouse EV production

INDUSTRY DIRECTIONS

Chinese exports require compliance readiness

Mexico exports strain supplier cash

LABOR DISPUTE

UAW pressures USMCA labor rules

MERGERS, VENTURES, ACQUISITIONS

Chinese investment deepens Serbia supply

Webasto forms China roof venture

Nissan rethinks Sunderland e-axles

Stellantis eyes Leapmotor Mexico production

OPENING

Tuskegee supports CPT stamping plant

PRODUCTION INCREASE

BYD launches in-house driving chip

Stellantis pipeline may aid Brampton

RAW MATERIAL DISRUPTION

China restricts Japan magnet materials

REGULATION

Washington targets Mexico content rules

US-Mexico begin USMCA talks

Automakers face transactional tariff policy

Volvo wins connected-car approval

Section 232 tariffs expand

UK export quota creates risk

USTR delays chip tariffs

EU delays Chinese chip sanctions

Mexico-EU remove EV tariffs

RELOCATING

GM shifts small cars to Mexico

SHUTDOWN

Honda pauses Ridgeline production

Expanding

Tata Motors plans to add 300k units of annual capacity in Gujarat over three years to meet rising demand in India. This expansion will push total passenger vehicle capacity over 1M units. Fuel costs are driving record interest in electric models. However, supplier bottlenecks are capping production.

Stellantis will invest $1.17B to build electric vehicles at its Mulhouse plant in France starting in 2029. This project is part of a broader $70B strategy to launch 60 new products and simplify platforms. The investment aims to use European capacity as Stellantis shifts to electrification. While consolidating platforms reduces complexity, it demands high capital for new assembly tooling.

Industry Directions

This Gasgoo analysis provides insight into the compliance considerations behind Chinese automakers’ export activities. Intelligent connected vehicles now require attention to software, data, cybersecurity, intellectual property, and regulatory systems, all of which must meet specific market standards prior to launch. For suppliers supporting Chinese OEMs in international markets, compliance has become an integral part of launch readiness rather than a post-engineering legal requirement.

Mexican light vehicle exports reached record levels in the first quarter of 2026, yet the surge masks a liquidity crisis for specialized suppliers. Payment cycles have stretched to 180 days, putting cash flow under pressure and limiting suppliers’ ability to purchase materials. Meanwhile, the heavy-vehicle segment saw production drop by 22%, exacerbating revenue challenges. USMCA tariff benefits are being ignored by many firms, with utilization falling to just 1.09% as companies absorb new duties rather than pass them on. Tier 2 and Tier 3 providers are currently trapped between high production demand, delayed payments, and compressed margins, making it increasingly difficult to cover day-to-day costs. Without better access to trade finance, the 75% regional content requirement remains a high hurdle for smaller Mexican shops, which lack the working capital to secure the necessary inputs.

Labor

The UAW is pushing for higher wages in Mexico and tougher labor rules during the USMCA review. Union leaders suggest the US should leave the pact if demands for stronger production quotas are not met. Automakers warn that tighter rules will increase consumer prices and costs. There is a risk that the USMCA review may raise content and wage rules faster than suppliers can adapt.

Mergers, Ventures, Acquisitions

Chinese companies plan to invest another $1.09B in Serbia across projects, including auto parts, tires, lighting, powertrain, energy, AI, and robotics. Named companies include Minth Group, Shandong Linglong Tire, Changzhou Xingyu Automotive Lighting System, Weichai Power, Zhejiang EV-Tech, and others. Serbia already hosts Stellantis assembly at Kragujevac, where Fiat and Citroen models are built. The investment deepens Serbia’s role as a lower-cost European supply base, backed by Chinese capital and a free trade pact with China.

Webasto is forming a joint venture with China’s Zhejiang Fujia Technology to develop glass roof systems for the local market. The partnership will focus on smart shading and solar technology to meet the high demand for features in China.

Nissan may drop JATCO’s planned e-axle plant in Sunderland, England, which was supposed to supply 3-in-1 e-axles for Nissan’s nearby EV production from 2026. The project was planned at about $56M, with 340k units of annual capacity and 183 jobs, but sluggish EV demand and Nissan’s broader restructuring have prompted the company to rethink component investments. For now, e-axles are expected to keep moving from Japan to the U.K. The decision would reduce local EV content at Sunderland just as Nissan prepares to produce the electric Leaf, Qashqai, and Juke there.

Stellantis CEO Antonio Filosa sees a chance to build Leapmotor vehicles in Mexico and Canada. This would boost factory use. He ruled out similar plans for the US due to trade tensions. The partnership allows Stellantis to share development costs and access advanced Chinese battery technology.

Opening

The city of Tuskegee received a $400k grant to build infrastructure for a new $163M CPT America stamping plant. This facility will produce metal assemblies for Southern auto manufacturers.

Production Increase

BYD has launched China's first in-house 4nm smart driving chip for Level 3 and Level 4 autonomous systems. The Xuanji A3 chip enables BYD to double its computing power while maintaining full control over its ADAS supply chain. BYD now builds nearly all its vehicle parts, including chips from its five wafer fabs. This level of vertical integration is unique among global automakers, giving BYD a major cost advantage. Skipping outside chip suppliers lets BYD update software features faster than rivals tied to third-party roadmaps.

Stellantis says it could introduce 11 new Chrysler, Dodge, Jeep, and Ram models by 2030. This may benefit Brampton Assembly in Ontario, which ceased vehicle production in 2023. The Jeep Compass program, once bound for Brampton, shifted to Belvidere, Illinois. Unifor still seeks a replacement mandate and rejected a proposal to build Leapmotor EVs from knockdown kits at the plant. Timing matters for suppliers: a future vehicle pipeline helps Brampton’s odds but does not solve the current volume gap.

Raw Material Disruption

China has restricted exports of heavy rare earths and gallium to Japan for four months due to a diplomatic dispute. Japan is the largest magnet maker outside China but relies on Beijing for key materials like dysprosium and terbium. Shin-Etsu and others have stopped taking new magnet orders due to the supply crunch. This move mirrors past Chinese trade actions using mineral controls as leverage. Stockpiles and Australian mining projects help, but replacing the Chinese supply will take years.

Regulation

Washington is demanding stricter rules of origin requiring a minimum level of US content for cars built in Mexico. Proposed changes would also require all steel receiving low tariffs to be melted and poured in North America to block Chinese material. The current deal only requires 40% of a vehicle to be made in high-wage factories. Closing these loopholes is a priority for US steelmakers who see a flood of Chinese parts entering Mexico. A US-specific content floor could disrupt established regional supply chains and force Tier 1s to relocate more work.

The US and Mexico will begin formal talks this week to revamp the USMCA, focusing on economic security and rules of origin. Canada is currently excluded from these bilateral rounds as Washington highlights significant trade differences with Ottawa. The negotiations aim to ensure the pact benefits US small businesses and manufacturers. Mexican officials view the 50% steel tariff as unsustainable and want a more systemic approach to the industry. The exclusion of Canada suggests that the US is using a divide-and-conquer strategy to pressure each partner into accepting better terms.

US automakers are using the current 15% tariff on EU and Japanese imports as a baseline for upcoming USMCA talks. Trade experts warn that policy has become more variable and transactional, adding immeasurable risk to capital planning. New Section 301 investigations could soon lead to additional tariffs on sectors with significant trade imbalances. The shift from stable generational rules to fluid trade policy is forcing suppliers to adopt more flexible sourcing models. Uncertainty regarding the duration of these deals makes it difficult for OEMs to commit to long-term import strategies.

Volvo Cars received US approval to continue selling its connected vehicles despite being owned by Geely, a Chinese company. The authorization follows discussions regarding the company's data security and technology governance. Volvo plans to start producing the XC60 SUV in South Carolina in late 2026 to boost its local capacity. The brand is also reversing its plan to go fully electric by 2030 and will keep hybrids in its lineup. This approval provides a clear pathway for other Western brands with Chinese investors to navigate new software security rules.

Toyota's decision to build the GR Corolla in Britain could trigger higher 27.5% tariffs for all UK-made cars if export quotas are exceeded. A trade deal currently allows 100k vehicles per year to enter the US at a 10% rate, but the cap is reset every January. The high demand for Range Rovers and Minis is already pushing the industry toward this limit. There is no formal mechanism in the UK to manage the flow of vehicles and prevent a low-cost Mini from being hit with the higher tax. Automakers may be forced to rush shipments at the start of each quarter to secure the lower tariff rate.

US Trade Representative Jamieson Greer stated that no imminent tariffs on semiconductors are expected, though protection is needed for reshoring efforts. The focus is on ensuring the timing and amount of duties support companies like Micron as they expand domestic plants. The government wants to allow firms to import some chips during the transition phase to avoid production stops. Micron is currently investing $30B in a Virginia project to build advanced memory chips. Sequencing these tariffs is critical for an industry where 90% of chips are still made abroad.

The EU has proposed a nine-month delay in sanctions against a Chinese chipmaker to prevent a severe disruption to automakers. Yangzhou Yangjie Electronic will remain on the list for aiding the Russian military, but the reprieve allows car firms to find new suppliers. European car makers became heavily reliant on the firm after previous sanctions hit other Chinese rivals. The move highlights the automotive sector's vulnerability to rapid shifts in trade sanctions. Unanimous agreement from EU countries is required to finalize the temporary reprieve for the supply chain.

Mexico and the EU will scrap mutual tariffs on electric vehicles and batteries this week as part of a modernized trade deal. The move aims to insulate both regions from US trade policy and reduce dependence on Chinese supply chains. Current Mexican exports of parts to Europe are subject to a 10% tax, which will be eliminated under the new framework. The deal positions Mexico as a strategic bridge between the EU and North American markets. For suppliers, the updated rules of origin will require new audits to ensure materials meet the duty-free standards.

Relocating

General Motors will move production of the Chevy Groove and Aveo from China to its Ramos Arizpe plant in Mexico in 2027. The project is part of a $1B investment and aims for a capacity of 80k units by 2030. The move offsets the loss of the Blazer, which is relocating to Tennessee. Relocalizing these high-volume models helps GM meet the local government's domestic production goals. The strategy aligns with a broader $4B plan to increase North American truck and SUV output to reduce reliance on offshore sites.

Shutdown

Honda will halt Ridgeline production in Alabama for 18 months, starting in late 2026, to update the truck to meet emissions rules. The pickup cannot meet current efficiency standards and requires a revised V6 engine and new components. During the break, the plant will increase production of the Odyssey and Passport crossovers by up to 20% to fill the gap. Supplier-related constraints prevented a continuous transition to the updated 2028 model. Retailers expect crossover sales to offset volume losses, but specific Ridgeline part suppliers face a prolonged period of idle capacity.