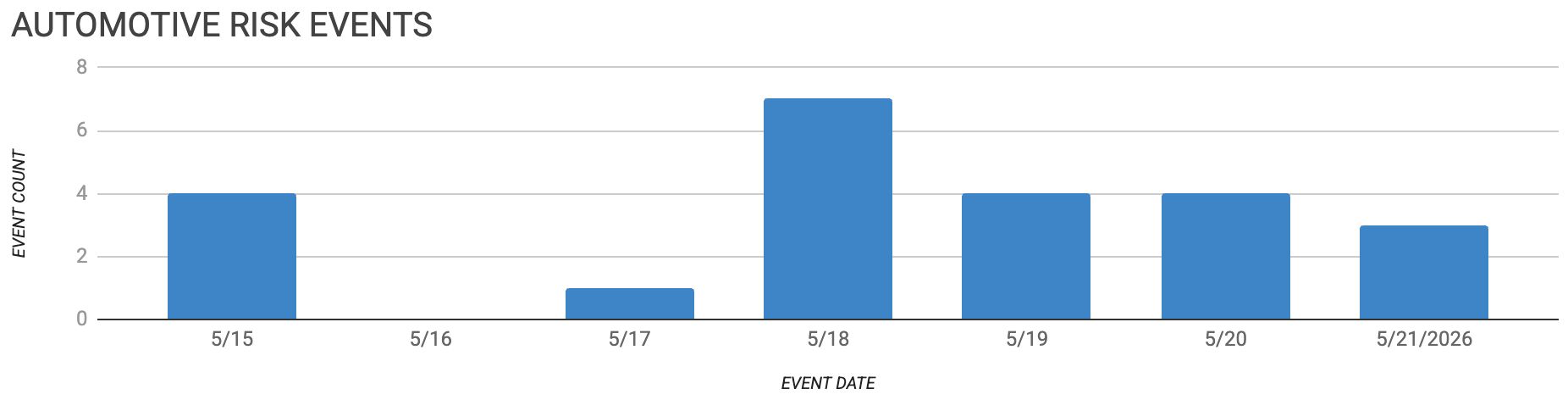

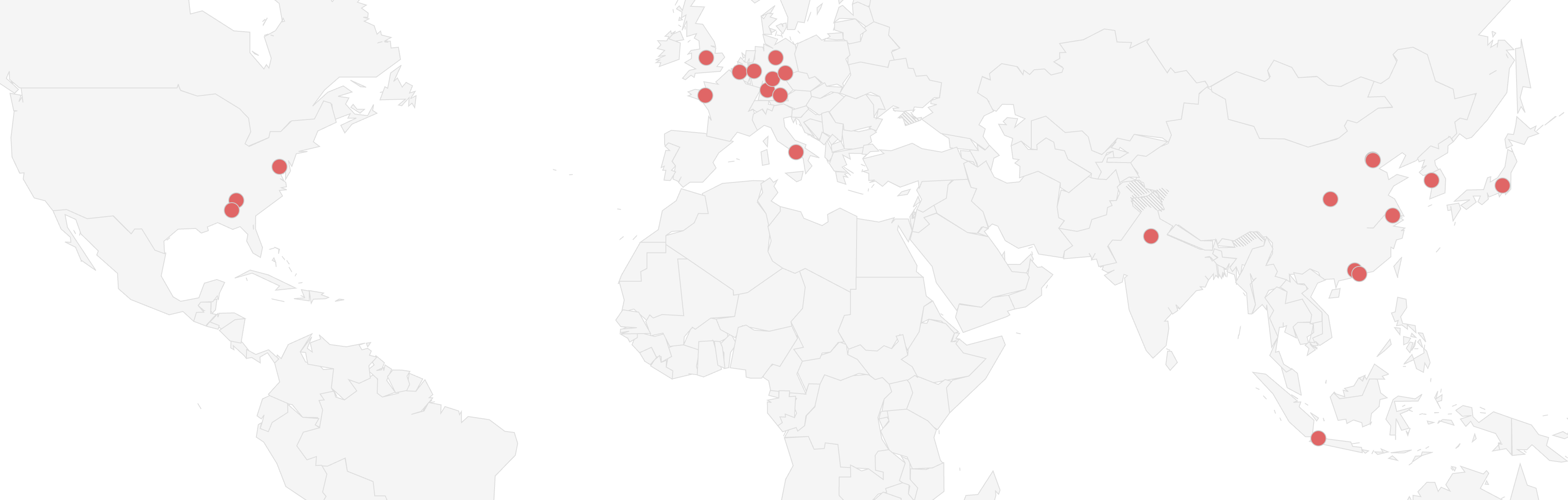

Automotive Supply Chain Risk Digest #483

May 15 - 21, 2026, by Elm Analytics

Dear Reader,

“Never, ever in 26 years have all six OEMs shown an increase.”

That line opens the latest Automotive Leaders Podcast. After a year of tariffs, EV write-offs, and disruption from every direction, the 2026 Plante Moran Working Relations Index still climbed across the board. Ford, Toyota, Stellantis, Honda, GM, and Nissan all moved up.

Elm Analytics’ own Sig Huber joined host Jan Griffiths and Dr. Angela Johnson of Plante Moran to dig into why. Sig raises the question underneath the scores: was this year’s collaboration a real shift, or a survival response that reverts once the pressure eases? He also names a reckoning this newsletter tracks weekly. Decades of low-cost sourcing came at the expense of resilience, and the bill is now coming due.

The WRI says relationships are improving. The harder question is whether they hold.

Give it a listen, then read on.

Warmly,

Nick Gaydos

Editor

Contents

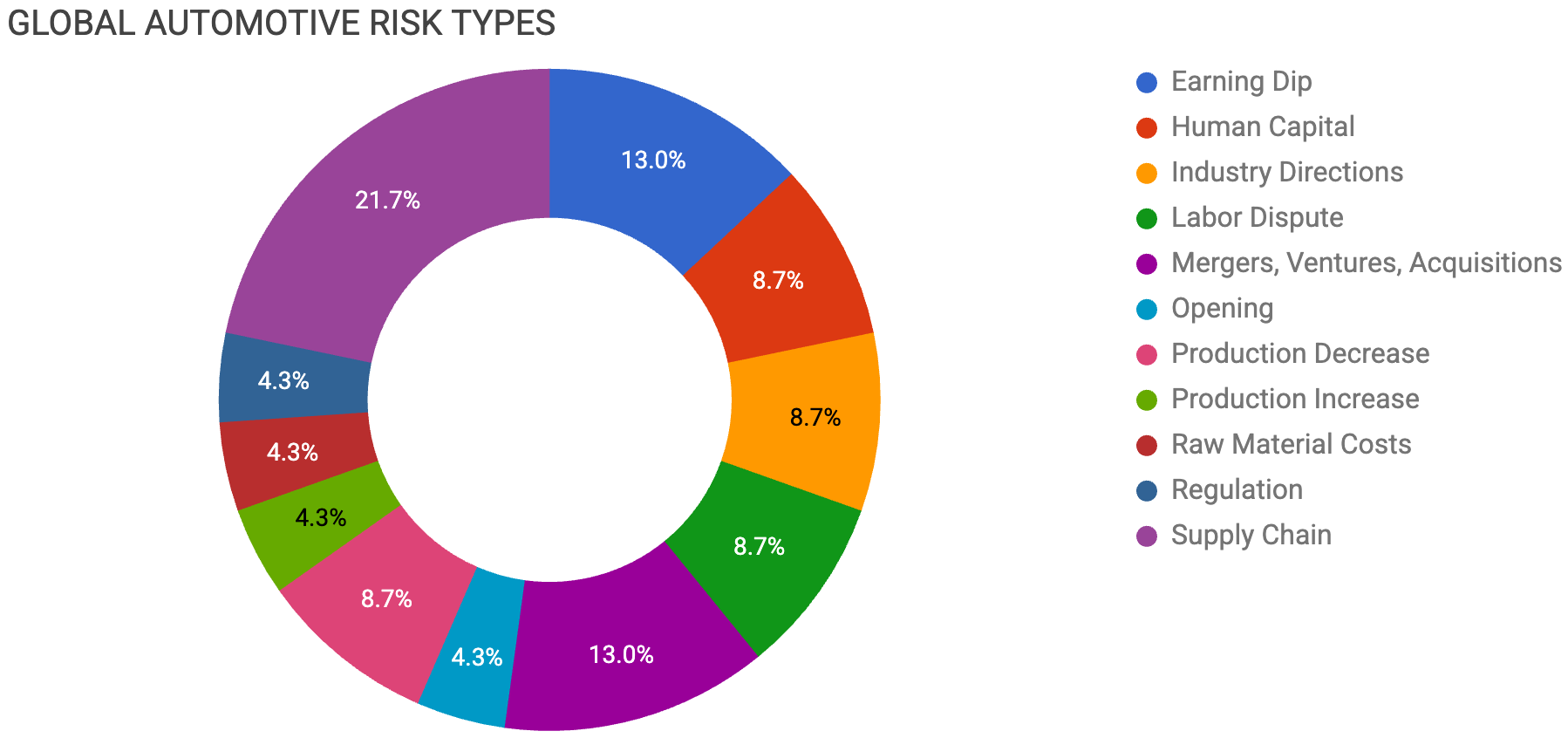

EARNING DIP

JLR targets deep cost cuts

Subaru delays independent EV

Eberspacher revenue and EBIT fall

HUMAN CAPITAL

Inalfa lays off 127 Georgia workers

ZF warns of more cuts

INDUSTRY DIRECTIONS

Ford plans seven European models

SDV readiness separates automakers

LABOR DISPUTE

VW labor blocks closures

MERGERS, VENTURES, ACQUISITIONS

Stellantis plans Voyah Europe JV

Nidec dissolves GAC, Stellantis JVs

Xpeng acquires Indonesian assembly entity

OPENING

Vertex opens Alabama molding plant

PRODUCTION DECREASE

VW reduces German overcapacity

Tesla abandons India factory

PRODUCTION INCREASE

Stellantis plans affordable Italian EVs

RAW MATERIAL COSTS

Lithium nears $28,500 per ton

REGULATION

EU reconsiders Chinese chip sanctions

SUPPLY CHAIN

Tariff uncertainty drives localization

BYD delays Great Tang launch

Blade Battery transition delays BYD

Xiaomi brings EV components in-house

Svolt targets hybrid battery production

Earning Dip

Jaguar Land Rover is targeting $2.3B in spending cuts over two years after posting an annual after-tax loss of about $330M, driven by US tariffs, currency headwinds, and persistent warranty costs. The late-August cyberattack that paralyzed global production for weeks cost an estimated $1.35B in revenue and helped push wholesales down 23% to 308k vehicles, below the company's break-even point. A Q4-2025 tariff bill of about $154M on vehicles exported to the US from the UK and its Slovakia plant has made some model derivatives and sales channels unviable. CEO PB Balaji said JLR plants are now at full capacity with no excess to share, directly rejecting a report that China JV partner Chery could assemble cars at a UK plant.

Subaru is taking a $362M charge and delaying its independently developed EV in Japan as slowing demand forces a tilt back to hybrids and combustion. The Oizumi plant, nearing completion for a 2028 opening, will launch with internal combustion and hybrid vehicles, adding EVs later depending on demand. US tariffs erased $1.42B from earnings and drove a 90% collapse in operating profit, a heavy blow for a company that draws more than 70% of global sales from the US and imports about half that volume from Japan. The company said it will keep developing core EV components but significantly cut the resources allocated to the effort. Subaru has limited its EV exposure by sharing development and assembly with Toyota, so the writedown is smaller than peers, but the tariff damage is the larger structural threat given its U.S. import dependence.

German supplier Eberspacher, which makes exhaust technology, air-conditioning systems, and vehicle electronics, reported 2025 revenue down 6.6% to $5.7B amid weak global car markets, US tariff policy, and Middle East tension. The family-owned company has cut costs by ending production at its plant in Thuringia and halting operations at its site in Rhineland-Palatinate. Headcount fell to 10,374 from 10,680, though Eberspacher said it currently has no plans for further job cuts.

Human Capital

Roof systems supplier Inalfa filed a WARN notice to permanently lay off 127 workers across two manufacturing facilities in Acworth, Georgia, with separations between July 17 and 31. The two Cherokee County sites will lose 83 and 44 jobs, respectively. Inalfa supplies panoramic roofs, sunroofs, and convertible roof systems to more than 40 vehicle brands across 16 global manufacturing sites. The company did not state a reason for the cuts in the filing.

German supplier ZF will keep production of electric motors and inverters in-house rather than buying the components externally, but warned that hundreds more job cuts are needed at its Schweinfurt and Auerbach sites in southern Germany. The decision sits within a broader overhaul that already includes 7.6k job cuts agreed last October. ZF said it would avoid forced redundancies wherever possible. Keeping e-motor production in-house is a notable counterpoint to peers like Nidec exiting the e-axle space, suggesting ZF still sees the powertrain as core rather than a commoditized buy.

Industry Directions

Ford will launch seven new models in Europe by 2029 to revive passenger car sales that have slid from over 1M a decade ago to just 426k last year, dropping it to eighth place. Five will be passenger cars, including a small electric car and a small electric SUV built at a Renault plant in northern France using Renault technology, plus three SUVs offered as hybrids and full EVs. Ford criticized Europe’s EV push, arguing that CO2 targets should reflect actual demand and support plug-in hybrids and range-extenders rather than full EVs only. The Renault-built EVs continue a pattern of legacy automakers borrowing platforms to cut costs and shorten time-to-market, the same logic driving the Stellantis-Leapmotor and Ford-Geely arrangements.

An analysis by Accenture and the Center of Automotive Management warns that platform decisions made years ago will determine which automakers survive the shift to software- and AI-defined vehicles. SDV-related revenue could reach $46B by 2030 and $133B by 2035, with average revenue per vehicle climbing from about $85 today to $460. Leaders will capture the gains through subscriptions and autonomous features, while laggards become commodity hardware suppliers. The report studied VW, Mercedes, BMW, Stellantis, Toyota, Tesla, Nio, BYD, Geely, and Xpeng, and concluded that automakers without SDV readiness by 2026-27 risk being locked out of the AI-defined vehicle market entirely. For suppliers, the divide matters because SDV leaders will pull more software and electronics value in-house, squeezing the addressable market for traditional component makers.

Labor

Volkswagen’s top labor representatives said they will not allow any German plant closures, while remaining open to proposals to secure underused sites. The position upholds a 2024 restructuring deal that ruled out closures in exchange for 35k job cuts by 2030. CEO Oliver Blume has floated the idea of plant-sharing with Chinese partners and is negotiating a possible sale of the Osnabrück plant to a defense company to address overcapacity. Works council head Daniela Cavallo and IG Metall leaders said they would fight anything that breaches the 2024 job security commitments.

Mergers, Ventures, Acquisitions

Stellantis and Chinese partner Dongfeng plan a joint venture to manufacture and sell Dongfeng's Voyah-branded EVs and plug-in hybrids in selected European markets, with potential production at the Stellantis plant in Rennes, France. Stellantis will lead the venture with a 51% stake, aligning with proposed Made-in-Europe local-content rules. This is Stellantis's second deal in two weeks to produce Chinese cars in Europe, following the Leapmotor agreement for Spain. Stellantis separately signed a non-binding deal with Jaguar Land Rover to explore product and technology collaboration in the U.S. The Rennes link is notable because Stellantis previously flagged it as one of four European plants with surplus capacity, so the Voyah deal reads as a way to backfill a site that might otherwise face closure.

Nidec is withdrawing from the e-axle business, calling it a red ocean of fierce competition, and will dissolve both of its joint ventures: one with GAC in China and one with Stellantis in Europe. The Chinese JV, founded in 2019, is already in exit negotiations, while talks with Stellantis over the Tremery, France, operation appear to be only a matter of time. Nidec reported a loss of about $510M in its e-axle business in the first half of the current fiscal year, including provisions for contract losses and facility impairments. The exit removes a major independent e-axle supplier from the market and leaves Stellantis to find an alternative for the Tremery plant, which was converted from diesel engine production and targeted an annual capacity of over 1M units.

Chinese EV maker Xpeng has acquired a 90.1% stake in Indonesian assembly entity EIDO from Erajaya Group, accelerating localized production in Southeast Asia's largest auto market. Xpeng entered Indonesia in March 2025 and delivered its first locally produced X9 MPV from an Indonesian plant in July, using a completely-knocked-down assembly model. Distribution, sales, and after-sales will continue under Erajaya entities while EIDO focuses on manufacturing. The deal fits a broader Xpeng localization push that also includes contract production with Magna Steyr in Austria and talks with Volkswagen about acquiring a European factory.

Opening

Korean supplier Vertex Innovations is investing $13.5M to convert a 120k ft² facility in Auburn, Alabama, into a plastic injection molding plant that will serve Korean automakers and Tier 1 suppliers across North America. The investment is one more node in the cluster of Korean supplier activity around Alabama, which hosts Hyundai and Kia assembly and a growing base of their component suppliers building closer to the customer.

Production Decrease

Volkswagen says it has nearly completed its plan to cut more than 700k vehicles of German production capacity without closing plants, achieving the reduction by scaling back production lines at sites including Zwickau, Emden, and Wolfsburg. The freed-up space in Wolfsburg will house the Gamechanger project, a faster, more efficient production method built around megacasting, the large-scale casting approach Tesla pioneered. The Osnabrück plant remains the unresolved piece, with VW negotiating a possible sale to a defense company, and Chinese partner Xpeng now mentioned as a potential user consistent with the labor position that closures stay off the table while alternative uses are explored. Xpeng separately confirmed it is weighing a new European plant as its Magna Steyr contract line in Austria nears capacity.

Tesla has confirmed it will not build a manufacturing facility in India, ending nearly a decade of on-and-off negotiations. The standoff was structural: Tesla wanted lower import tariffs before committing capital, and India wanted a factory commitment before cutting its 110% duty. The deeper issue is that Tesla’s existing factories run at roughly 60% capacity, with Giga Berlin at about 65% in Q1 2026, making a new plant hard to justify in a market where Tesla has sold fewer than 400 vehicles total. Tesla’s India retreat and its halted Mexico project both point to a demand problem rather than a capacity problem, a signal worth weighing for suppliers planning around Tesla volume.

Production Increase

Stellantis will produce a new range of affordable small EVs for Europe starting in 2028 at its Pomigliano d’Arco plant near Naples, under multiple brands and with partners to speed development and cut costs. The E-Car project aligns with a European Commission push, championed by President Ursula von der Leyen, to build a homegrown, affordable small car and prevent the Chinese conquest of the segment. Chairman John Elkann has argued that EU regulations have made compact cars expensive to build by adding weight and cost. Producing affordable small EVs in a high-cost European plant is the central tension here, which is why the project leans on shared platforms and partners, the same cost logic behind the Leapmotor and Dongfeng tie-ups.

Raw Material Costs

More than 15 major Chinese automakers, including BYD, Xiaomi, and several joint ventures, have raised vehicle or option prices as lithium and chip costs surge, marking a shift from years of price wars to cost-driven inflation. Battery-grade lithium carbonate has nearly tripled in under a year to about $28.5k per ton, while AI demand has diverted chip production and pushed automotive memory prices up roughly 180% in three months, adding $400 to $1k per intelligent vehicle by UBS estimates. Aluminum and copper at multi-year highs added roughly $300 to the raw material cost of a mid-size EV. China’s auto industry profit margin fell to 3.2% in Q1 2026, with high-end NEV makers better able to absorb the shocks than mid- and low-end manufacturers near break-even. This is the upstream cost wave that connects directly to the battery capacity and pricing stories below, and it signals margin pressure flowing toward suppliers across the chain.

Regulation

The European Union will propose temporarily lifting sanctions on a Chinese semiconductor supplier after automakers warned of supply chain chaos within weeks if the sanctions remain in place. The company was listed in the EU’s 20th sanctions package for supplying dual-use goods to Russia, but automakers said they have not had time to diversify and that their stocks would deplete quickly. The episode echoes last year’s Nexperia disruption, when a corporate-and-government feud over the Chinese-owned chipmaker triggered automotive chip shortages. The pattern is becoming familiar: legacy low-tech chips concentrated in Chinese-controlled supply remain a single point of failure that can halt production, and diversification is proving slower than the geopolitical risk is moving.

Supply Chain

Industry experts advise automakers and suppliers to bet on supply chain localization, robotics, and factory automation to weather prolonged tariff uncertainty. Nearly two-thirds of suppliers are considering reshoring, per MEMA, though tariffs have also raised cost volatility for US parts and complicated investment decisions. The Supreme Court’s strike-down of more than $170B in tariffs collected from April 2025 through February, plus the July USMCA review, has deepened the uncertainty that makes committing capital difficult. Roland Berger noted that localization is constrained by US labor shortages, putting automation at the center of any reshoring push. The recurring advice across these trade pieces is flexibility… build it into supply chains and contracts, because the rules are still moving.

BYD has delayed the launch of its Great Tang full-size electric SUV to June 8 after cumulative pre-sale orders topped 100k units, with several dealers not yet receiving their first vehicles. The delay traces to a broader production squeeze: Chairman Wang Chuanfu acknowledged that demand for models using BYD’s second-generation Blade Battery and flash-charging platform has outrun battery manufacturing capacity. The constraint is hitting deliveries across BYD’s Dynasty, Ocean, Denza, and Yangwang lines, not just the Great Tang.

The same capacity squeeze is delaying BYD’s Fang Cheng Bao sub-brand, where the Tai 3 flash-charging SUV slipped from mid-April to May, and executives were stationed at production bases in Shaanxi, Anhui, and Zhengzhou to ramp output. Wang said the core issue is the comprehensive transition from first- to second-generation Blade Battery, which requires halting and retrofitting older production lines. BYD expects the line upgrades to wind down through May and capacity to recover after June. The episode is a useful reminder that even the most vertically integrated player in the industry can be throttled by a single component transition. BYD’s April sales fell 15.5% year over year for an eighth straight monthly decline despite the order backlog.

Xiaomi has established a wholly owned subsidiary, Beijing Xiaomi Jingxu Technology, to produce core EV components, including batteries, electric motors, and electronic control systems. The move pushes Xiaomi toward greater supply chain independence after it has relied on suppliers like CATL and BYD Fudi for batteries. A separate 15 GWh battery plant, a joint venture involving CATL, BAIC, and Xiaomi, is expected to start production later this year near Xiaomi's Yizhuang plant. Xiaomi's vertical integration mirrors the broader Chinese pattern of automakers bringing battery and motor production in-house to control costs and supply, as seen in BYD's fully integrated model.

Svolt Energy plans to mass-produce hybrid solid-liquid batteries by September at costs on par with traditional liquid lithium-ion cells, positioning the technology as the mainstream route until all-solid-state batteries mature. Hybrid solid-liquid cells, previously called semi-solid-state, use both liquid and solid electrolytes and offer improved safety. Svolt expects a 100kWh version to reach large-scale production by the end of September. CATL and BYD are targeting 2027 for small-batch all-solid-state production, leaving a multi-year window during which hybrid cells will fill the gap. Cost parity is the key claim, as semi-solid chemistry has historically commanded a price premium, limiting it to flagship models.