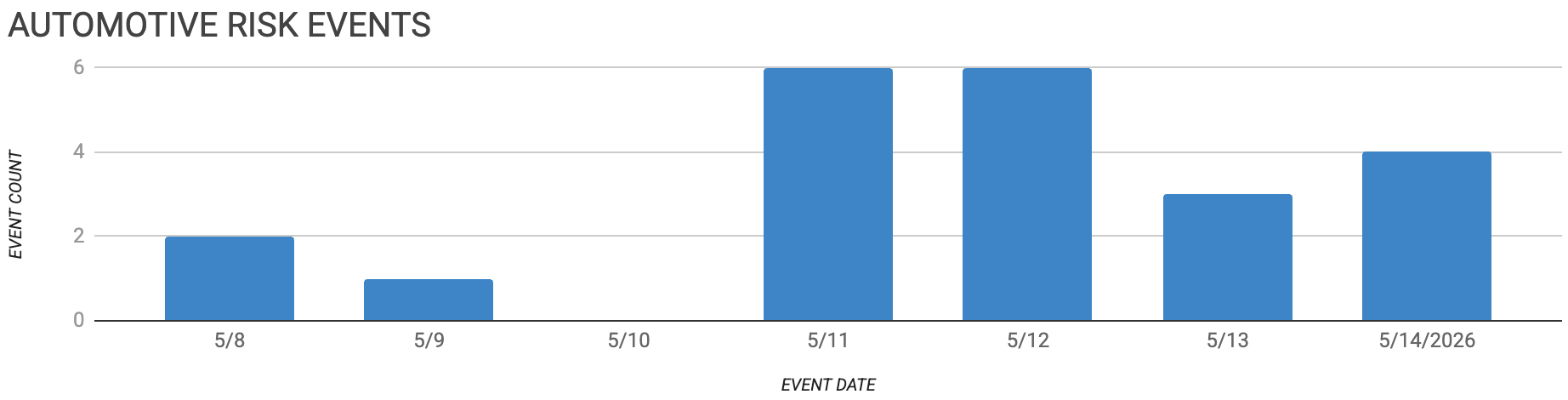

Automotive Supply Chain Risk Digest #482

May 8 - 14, 2026, by Elm Analytics

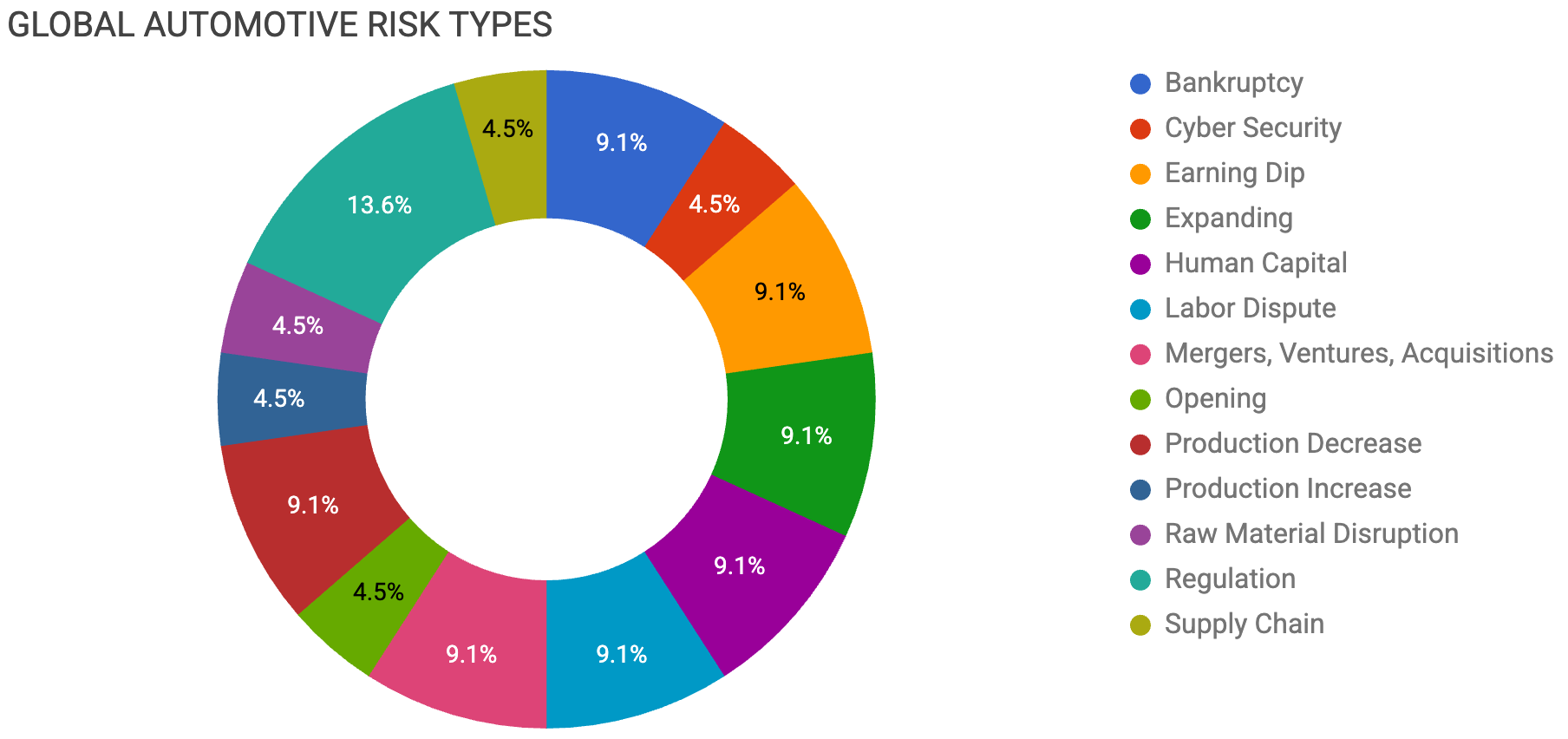

Contents

BANKRUPTCY

Michigan manufacturer enters Chapter 11

Toledo Molding sale preserves jobs

CYBER SECURITY

Auto cyberattacks increasingly target suppliers

EARNING DIP

Honda retreats from EV strategy

Toyota forecasts war-related profit drop

EXPANDING

DUCK IL opens Alabama plant

Tesla expands Berlin battery production

HUMAN CAPITAL

Automakers cut global workforce

VDA warns of EU job losses

LABOR DISPUTE

Samsung strike threatens chip supply

Unifor targets Ford labor talks

MERGERS, VENTURES, ACQUISITIONS

Huawei, JAC pursue Maserati EVs

Stellantis, Leapmotor expand Spanish production

OPENING

Toyota plans third India plant

PRODUCTION DECREASE

Honda Canada halts Ontario EV complex

Mazda delays dedicated EV launch

PRODUCTION INCREASE

GWM starts Ora 5 production

RAW MATERIAL DISRUPTION

Hormuz closure squeezes sulfur supply

REGULATION

Canada seeks Section 232 removal

USMCA review raises trade uncertainty

Chinese suppliers face decoupling pressure

SUPPLY CHAIN

Ford tightens supplier performance rules

Bankruptcy

Precision Manufacturing Group filed for Chapter 11 in Muskegon, Michigan, after reporting $3.5M in liabilities against $817k in assets. The company produces steel and aluminum components for automotive clients. Losses stem from major customers shifting to offshore sources and technical failures with a newly financed fiber laser. This insolvency highlights the fragile liquidity of smaller Tier n shops, facing rising capital costs, customer consolidation, and global competition.

The proposed $80M sale of Toledo Molding & Die to a JVIS USA affiliate would preserve 600 jobs at facilities in Bowling Green and Tiffin. Automakers, including Ford and Stellantis, provided interim funding to maintain production of critical interior and HVAC systems during the bankruptcy. The deal excludes customer-owned tooling to ensure production programs can continue without disruption. The use of week-to-week funding by OEMs underscores the high risk of line stoppages.

Cyber Security

Cybersecurity damages in the automotive sector reached $20B in 2025 as software-defined vehicles expand the digital attack surface. Reports indicate that 57% of cyberattacks now target suppliers rather than OEMs. A single vulnerability in a Tier 2 component can potentially impact millions of vehicles via remote exploits. For risk managers, this shift necessitates deeper visibility into the software security protocols of sub-tier electronic vendors.

Earning Dip

Honda reported a $2.7B net loss for the fiscal year after taking $9B in charges to scale back its electric vehicle strategy. The automaker is abandoning its 2040 target for a fully electric lineup in favor of next-generation hybrids. Cooling demand and the loss of federal subsidies in the US forced this retrenchment. This pivot mirrors broader industry moves to preserve margins by extending the life of internal combustion platforms.

Toyota warned that the ongoing war in Iran will cost the company $4.3B this fiscal year due to soaring material and energy prices. The automaker reported a 50% drop in quarterly profit as transportation expenses and paint costs climb. Despite record hybrid sales, the company expects full-year earnings to fall by 20%. Toyota's decision to absorb cost increases for its suppliers provides a liquidity cushion for its Japanese production base.

Expanding

South Korean supplier DUCK IL USA will invest $21M to establish its first US manufacturing facility in Auburn, Alabama. The plant will feature a clean room for producing electronic seat switches and dashboard controls. Initial operations will create 20 jobs with plans to supply GM, Hyundai, and Kia.

Tesla will invest $250M into its Berlin-Brandenburg factory to expand battery cell production. The site recently reached a production milestone of 750k vehicles and aims to reach 1M units per year eventually. This expansion comes as Tesla sales in Europe show signs of recovery following a year of stagnation.

Human Capital

Global automakers, including Nissan, Stellantis, and Renault, are cutting thousands of engineering and production jobs in 2026. These reductions aim to lower overhead as the industry shifts toward simpler software-defined vehicle architectures. Experts suggest legacy firms are struggling to dismantle organizational structures built for hardware complexity. This labor contraction reflects a permanent shift in the skills required for modern vehicle development.

Germany's VDA warned that 125k automotive jobs could vanish by 2035 under current European Union emissions regulations. The association argues that a strictly battery electric mandate threatens 50k positions in the domestic supply chain. They are advocating for a technology-open approach that includes hybrids and hydrogen. This projection signals a long-term capacity risk for traditional powertrain suppliers in Europe.

Labor

A potential strike by 40k Samsung Electronics workers in South Korea threatens to disrupt the global semiconductor supply chain. An 18-day stoppage could result in $22.4B in losses ($29M per hour!) and reduce global DRAM output by up to 0.9%. If the process halts briefly, all wafers are discarded. One wafer yields about 1.8k DRAM chips worth $3.3k–$3.5k each. A line stoppage wastes 3–4 months of regular DRAM wafers or 7 months of HBM wafers. Unlike vehicle assembly, semiconductor fabs require weeks of recalibration if lines are halted. Automotive purchasing teams should consider the implications of potential allocation constraints on HBM and standard memory chips.

Unifor will begin contract negotiations with Ford on June 22 to set the labor pattern for the Detroit Three in Canada. The talks precede a critical review of the USMCA trade agreement scheduled for July 1. Ford recently began preproduction of Super Duty trucks at its Oakville plant to meet heavy-duty demand. These negotiations will test labor stability as the Canadian industry navigates shifting EV policies and tariff pressures.

Mergers, Ventures, Acquisitions

Huawei and JAC are in talks with Stellantis to co-develop new energy vehicles for the Maserati brand. The project would utilize Huawei's technology stack and JAC's manufacturing footprint for production starting in late 2027. Maserati sales have fallen from 27k units in 2023 to under 8k in 2025. Partnering with a Chinese manufacturer could provide Maserati with the software capabilities needed to regain relevance in the Asian market.

Stellantis and Leapmotor will begin joint production of electric SUVs at the Zaragoza plant in Spain. The partnership allows Leapmotor to bypass European Union tariffs while filling underutilized capacity at Stellantis facilities. The two companies will also cooperate on parts purchasing to leverage Chinese battery technology and European supply chains. This model of technology-for-capacity swaps is becoming a primary survival strategy for European OEMs.

Opening

Toyota will build a third manufacturing plant in India with an initial annual capacity of 100k vehicles. Located in Maharashtra, the facility will produce a new SUV model starting in 2029 and create 2.8k jobs. The plant will handle the entire manufacturing process, from stamping to final assembly. This expansion targets the world's third-largest vehicle market and serves as an export hub for neighboring regions.

Production Decrease

Honda Canada has indefinitely suspended its plans for a $15B electric-vehicle and battery complex in Ontario. The decision does not impact current production at the Alliston facility, where 4.2k people are employed. Shifting customer demand and revised strategic objectives prompted the halt of the project. This suspension adds to a growing list of canceled North American battery projects following the repeal of federal EV incentives.

Mazda will delay its first dedicated electric vehicle launch until 2029 while cutting related investment by nearly half. The automaker is shifting R&D resources back to internal combustion and hybrid systems, including the new Skyactiv-Z engine. By acting as an intentional follower, Mazda avoided the multi-billion-dollar write-downs experienced by its peers. {Mazda’s strategy of exporting China-built EVs to Europe minimizes capital risk during a period of high regulatory uncertainty.}

Production Increase

Great Wall Motor started production of the Ora 5 compact SUV at its plant in Rayong, Thailand. The facility has an annual capacity of 80k units and utilizes 50% locally sourced parts. GWM plans to export 40% of its Thai production to other Southeast Asian markets. The plant is capable of running internal combustion and electric models on a single line to maximize capacity flexibility.

Raw Material Disruption

The closure of the Strait of Hormuz is creating a critical shortage of sulfur used to produce battery-grade nickel and lithium. Sulfur prices in Asia have jumped 50% to $880 a ton as seaborne volumes from the Middle East collapsed. Refineries in Indonesia and Australia are struggling to secure the sulphuric acid needed for high-pressure acid leach processing. A prolonged blockage threatens to halt the primary supply of battery materials for Chinese and Korean cell makers.

Regulation

Canadian industry leaders are calling for the removal of US Section 232 auto tariffs ahead of the upcoming USMCA review. The 25% duties currently apply to the non-US content of vehicles exported from Canada to the United States. This trade friction has led brands like Nissan and Subaru to stop selling certain US-made models in Canada. Stakeholders argue that North American integration is essential to competing with the growing influence of Chinese automakers.

US automotive trade costs are rising as 25% tariffs on parts and vehicles create tens of billions of dollars in annual costs. While some production has moved to the US, most manufacturers find it difficult to upend complex global supply chains. A mandatory review of the USMCA on July 1 could lead to even stricter regional-content requirements. The resulting uncertainty is stalling long-term investment decisions for both domestic and foreign OEMs.

Over 60 Chinese-owned suppliers are now deeply integrated into the US automotive parts network. These companies control roughly 5% of the country's 10k suppliers and provide critical systems such as steering, glass, and airbags. Recent legislative proposals aim to ban China-made safety components and vehicles from American roads. Decoupling from these entrenched Tier 1 and Tier 2 entities would require massive capital reinvestment and years of re-sourcing.

Supply Chain

Ford is implementing a no-bid list for suppliers that fail to meet strict quality and cost reduction targets. Parts makers are being required to enter into three-year plans that demand annual savings of 3% or risk losing future business. The automaker aims to save $1B in material and warranty costs this year following a record number of recalls. These aggressive procurement tactics may further strain Ford’s supplier relations, which already rank among the lowest in the industry.