Automotive Supply Chain Risk Digest #480

April 24 - 30, 2026, by Elm Analytics

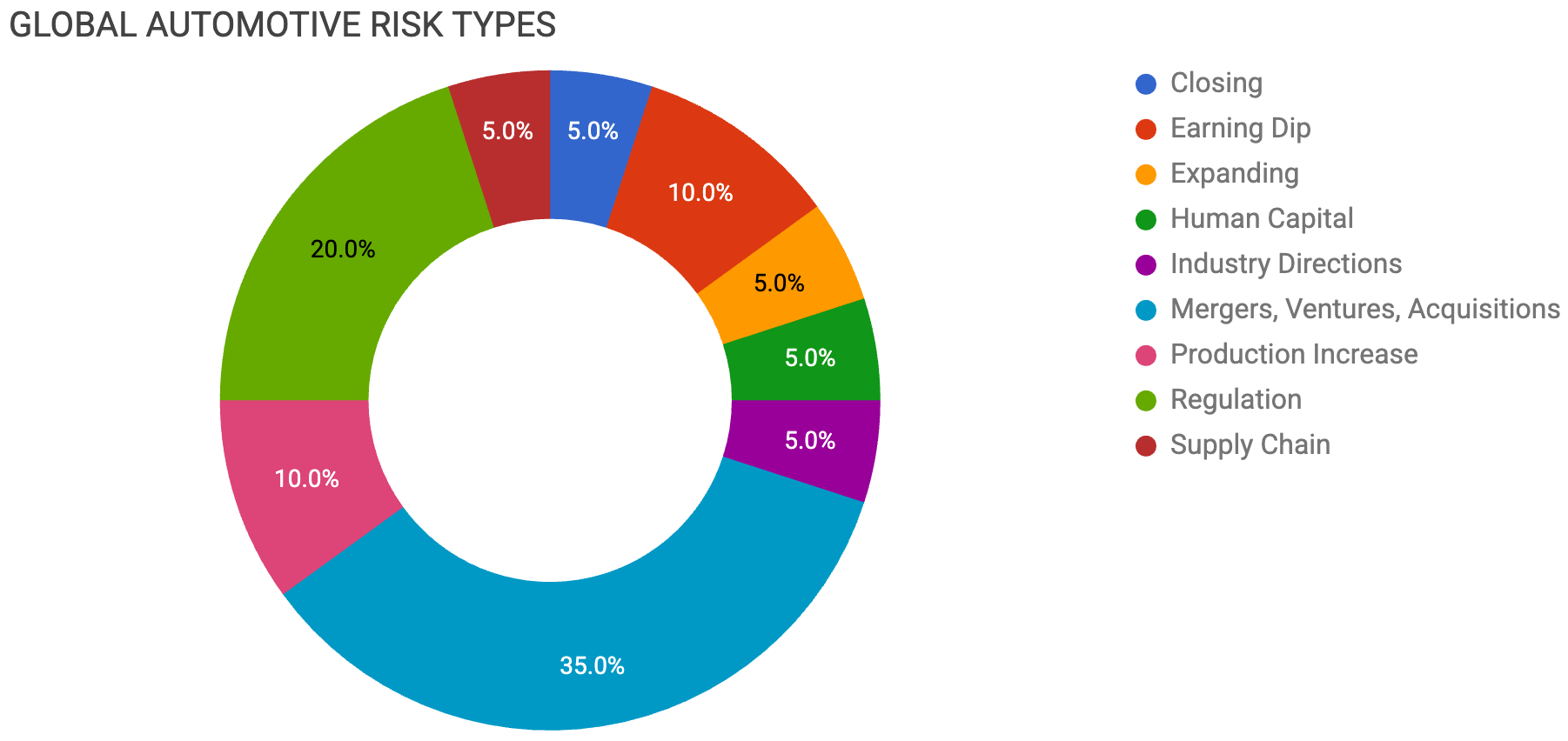

Contents

CLOSING

American Fine Sinter closing Ohio plant

EARNING DIP

Aston Martin losses narrow, debt grows

BYD profit drops amid China weakness

EXPANDING

GM boosts North American combustion capacity

HUMAN CAPITAL

Yanfeng layoffs follow Volkswagen changes

INDUSTRY DIRECTIONS

BYD discounts deepen China price war

MERGERS, VENTURES, ACQUISITIONS

Apollo buys Forvia interiors business

Aumovio sells Rheinbollen brake site

Adient acquires Romulus foam plant

Denso may abandon Rohm bid

Volkswagen may share European capacity

Hongqi eyes Stellantis Zaragoza plant

SAIC plans Spanish MG factory over Hungary

PRODUCTION INCREASE

Rivian Georgia capacity to reach 300k

Nexteer begins steer-by-wire production

REGULATION

Automakers book $2.3B tariff refund estimates

Canadian moldmakers squeezed by tariffs

USMCA may remove affordable cars from market

Atlantic Council outlines USMCA scenarios

SUPPLY CHAIN

Toyota suppliers face Iran disruptions

Closing

American Fine Sinter, the Tiffin, Ohio, subsidiary of Japan’s Fine Sinter Co., will gradually close its plant by March 2028, eliminating roughly 175 jobs. This move follows the parent company’s review of North American demand, which led to the decision to source future production from other group facilities. AFS makes sintered components for internal engines, transmissions, and vehicle suspensions, and the closure will roll out in steps starting later this year.

Earning Dip

Aston Martin reported a narrower Q1 pretax loss of $88.5M. Net debt climbed to $1.98B, driven by ongoing struggles, including US tariffs, a slowdown in China, and repeated product delays. Billionaire chairman Lawrence Stroll is providing a further $67.9M facility through his consortium to ease balance sheet pressure. CEO Adrian Hallmark also flagged that the Middle East conflict adds risk to full-year guidance.

BYD reported its sharpest quarterly profit drop since 2020. Q1 net profit fell 55.4% year over year to $599M, while revenue declined 11.8% to $22B. The drop was driven by a seventh straight month of domestic sales decline in March; however, overseas shipments grew, making BYD increasingly dependent on international expansion to offset weakness at home. The company has set a 2026 overseas sales target of 1.5M vehicles, which implies growth of more than 40% from 2025.

Expanding

In contrast to cutbacks elsewhere, General Motors is investing roughly $1.4B across three US plants and one Canadian plant that produce gas engines, transmissions, and metal castings, reinforcing its combustion-engine capacity as EV demand softens. The investment includes $300M at Romulus, Michigan, for transmission production; $150M at a Saginaw, Michigan, casting plant for engine parts; $40M at a Toledo, Ohio, transmission plant; and $505M at an Ontario facility for the next-generation V-8 engine.

Human Capital

Chinese supplier Yanfeng Automotive Interiors will lay off 153 workers at its Chattanooga, Tennessee, plant on June 29, ending a relationship dating to 2017 when it began supplying dashboards and door panels for VW’s Atlas SUV. Although the plant was expected to employ about 325 people at full production after a $55M investment, volume never reached that level. VW spokesperson Michael Lowder noted that the automaker periodically changes suppliers for specific components. He also confirmed that seating supplier Adient will stop supplying VW around July, resulting in the closure of Adient’s Athens, Tennessee, plant and 210 additional layoffs. VW recently ended ID.4 production in Chattanooga to focus on the gas-powered Atlas family.

Industry Directions

BYD's average discounts hit a record 10% in March as China’s automotive price war continues despite repeated efforts by Beijing regulators to halt it. The pressure is accelerating Chinese automakers’ overseas push into Brazil, the UK, Australia, and Canada, but it is also reshaping supplier payment dynamics. Following regulatory scrutiny, BYD has been forced to pay parts makers faster, shifting away from an IOU-based system that allowed it to delay invoice fulfillment for months. The change has loaded BYD’s balance sheet with interest-bearing debt, pushing its net debt-to-equity ratio to 25% after four years of net cash. The underlying issue is overcapacity: Chinese factories can produce 55.5M vehicles annually, while domestic sales were just 23M in 2025.

Mergers, Ventures, Acquisitions

Private equity firm Apollo has agreed to acquire Forvia’s Interiors Business Group in a carve-out transaction. This separates one of the world’s leading suppliers of instrument panels, door panels, and center consoles from its parent. The business has a global manufacturing and engineering footprint across Europe, North America, and Asia, and serves a diversified base of OEMs. Apollo’s automotive portfolio currently includes Tenneco, TI Automotive, and Panasonic Automotive. These groups collectively generate $28B in annual revenue across 50 countries. The transaction is expected to close in the second half of 2026, pending regulatory approvals.

Building on themes of strategic refocusing, German supplier Aumovio is selling its Rheinbollen site to RHB-Industries. The site employs about 320 people and produces brake calipers, electric parking brakes, and autonomous mobile robots. The buyer is a subsidiary of transformation consultancy Falkensteg, established specifically for this transaction. Aumovio was formed in September 2025 as a spin-off from Continental Automotive. The company cited consolidation of its European footprint and a sharper focus on its core business as reasons for the sale.

Adient has acquired a seating foam production plant in Romulus, Michigan, from Woodbridge, adding to its network of 10 foam plants in the Americas region and 30 globally. The deal includes the building, land, production equipment, inventory, and the existing workforce, with the UAW collective bargaining agreement remaining in place.

Denso said it has not gained agreement from Japanese chipmaker Rohm for its acquisition proposal and is now considering withdrawing the offer. The bid, made last month, would have expanded Denso’s control over power-management chips used in electric vehicles and data centers. The Toyota supplier has been investing heavily in semiconductor capabilities to secure supply for next-generation vehicles.

Amid these changes, a wave of Chinese automakers is moving to establish production in Europe, with Spain emerging as the preferred entry point.

For example, China’s SAIC Motor plans to build an EV factory in Spain for its MG brand, sidestepping the EU’s 45.3% tariff on China-built battery-electric cars. The decision effectively rules out Hungary, which had been the alternative despite its growing EV cluster around BYD. MG was Europe’s top-selling Chinese brand in 2025 with 307k registrations, up 37% from 2024, and Europe boss William Wang said the brand’s scale now makes local production a necessity. Investment size and production capacity are still being finalized, with output potentially starting as early as next year.

Another Chinese automaker is taking a different path. Hongqi, the luxury brand owned by state-owned FAW, is in talks to build vehicles at Stellantis’ Zaragoza plant, negotiating through their shared investee Leapmotor. This arrangement would allow Hongqi to avoid the cost of a new European factory while accelerating its plan to launch 15 EV and hybrid models across 25 European markets by 2028. The company is targeting 1M in annual sales by 2030, with at least 10% of sales outside China.

Volkswagen is now considering the inverse. CEO Oliver Blume told analysts that VW is exploring whether to bring its China-developed cars to Europe and to share its underused European factories with its Chinese partners, including SAIC, FAW, JAC, and Xpeng. The shift would mark a sharp break from VW’s traditional model and signal that Chinese-designed vehicles built in European plants are becoming a mainstream strategic option.

For European suppliers, the implications are substantial. Spain’s deep Tier 1 and Tier 2 base is one of the reasons the country is attractive. However, Chinese OEMs have historically brought much of their own supply chain with them, as BYD did in Hungary. Whether MG, Hongqi, and any VW-China hybrid arrangement meaningfully localize or simply transplant Chinese supply chains onto European soil will determine whether the existing supplier base wins new business or is gradually displaced. Either outcome adds pricing pressure to a European supplier market that is already oversupplied and consolidating.

Production Increase

Rivian is increasing initial production capacity at its Georgia manufacturing plant to 300k vehicles annually, a 50% jump from the original 200k estimate, to support its new midsize R2 platform. Vertical construction is expected to begin this spring, with vehicle production starting in late 2028. Rivian also recently announced a partnership with Uber to build up to 50,000 robotaxis at the Georgia plant.

Nexteer Automotive has started series production of its first steer-by-wire system, fitted to a passenger vehicle from an unnamed Chinese NEV manufacturer. The technology is increasingly seen as foundational for higher levels of automated driving, where steering, braking, and throttle all need to accept machine inputs.

Regulation

Several major automakers booked roughly $2.3B in expected refunds from US tariff payments in Q1. This follows a February Supreme Court ruling that struck down some Trump administration tariffs imposed under the International Emergency Economic Powers Act. Ford recorded $1.3B; GM, $500M; Stellantis, $467M; and Mercedes-Benz, an unspecified amount. These were booked as accounting estimates, not cash received. Up to $166B in reimbursements is due to importers who paid IEEPA tariffs. Companies acknowledged uncertainty over timing. President Trump warned he would “remember” companies that opt for refunds. The IEEPA tariffs were only one part of the broader regime. GM said tariffs will still cut $2.5B to $3.5B from its 2026 profits, while Ford put its net tariff cost at $1B.

Canada’s tool-and-die and moldmaking sector is being squeezed by US sectoral tariffs. Industry leaders warn that, without urgent federal action, capacity could shift south of the border, as tariffs erode profitability. Jon Azzopardi, president of Laval Tool in Windsor, told a parliamentary committee that 90% of his company’s output ultimately depends on US demand. He said the industry has gone “from being profitable to not profitable overnight” due to the recent tariff change. The April 6 change extended the 25% derivative tariff to the full value of imported goods, not just the metal content, directly impacting margins that typically run in single digits. The Canadian moldmaking industry exports about $7B annually to the US, with around 75% of activity concentrated in Ontario. During production, products often cross the border multiple times, and each crossing can trigger tariffs on accumulated value, further reducing profitability.

Foreign automakers have warned the Trump administration that they could pull their cheapest car models from the US market if USMCA is not renewed or is significantly weakened, the Wall Street Journal reported. The companies have told Trump’s economic advisers that they may not be able to build and sell affordable cars for the US market without meaningfully reduced tariffs on cars and parts made in North America. The auto industry has been pressing for an extension of USMCA, calling it crucial to American auto production. Trump’s 25% Section 232 tariff on Mexican and Canadian automotive exports replaced the duty-free trade under the agreement, and the three nations face a July 1 deadline for the trade deal review.

The Atlantic Council laid out three scenarios for USMCA’s July review: clean renewal with targeted modifications, no consensus leading to bilateral deals, or no consensus and no replacement. Each carries distinct supply chain consequences: the bilateral scenario forces manufacturers to operate under dual compliance regimes, while the no-deal scenario reverts trade to pre-NAFTA tariff levels. The analysis recommends supply chain teams treat the period before July as a planning window: rethink production footprints, strengthen US hubs, shift from just-in-time to inventory buffers, invest in dual sourcing, monitor supplier solvency, and run bill-of-materials audits to identify components that could lose preferred status. Companies with integrated North American platforms face the greatest exposure, particularly if Canadian upstream metals and subassemblies lose preferential access.

Supply Chain

Toyota Industries President Koichi Ito said Japanese suppliers are increasingly receiving two weeks’ notice that components will not be available, as the Iran conflict ripples through the auto industry’s supply base. Toyota supplier Denso projected $3.1B in operating profit for the fiscal year through March 2027, well below the $4B analyst estimate, and has factored in roughly $282M in profit hit from supply chain uncertainty. Toyoda Gosei warned that raw material disruptions could emerge as early as June, particularly thinners used in automotive paint, and has assumed 200k fewer vehicles in its production planning. Toyota Boshoku is now seeking short-term supply assurances from individual suppliers, as long-term commitments have become difficult to secure. Executives note that everything from door trims to seat urethane traces back to naphtha-derived resins.

A perfect follow on piece from last week. Notwithstanding the undertone of abdication of future design and development planning within the top ranks of 'western' OEMs, it appears the future of employment lays in the hands of tier 1 and 2, including their local value chains. By this I mean can they compete, or at the very least conjoin, with a volume hungry China supply base.

I foresee no specific change in the US administrations assertion tarrifs are the ultimate cash-cow. Creating an environment where USMC trade talks may turn out to have a more significant role than many realise, for the rest of the world.

If the US admin get this wrong, it is possible it becomes an active plan to degrade the systems that prop up the labour market surrounding the US automotive industry, which extends way further than just a narrow view of the value chains alone. If non-US entities already see no value in the US for entry level vehicles, it will compound up to medium level vehicles. The US admin gets what it ultimately appears to want, isolation from global manufacture and supply. But at what cost?

Therefore, the move of Chinese OEMs into the second largest economy (as of now!) becomes a balancing act. Should they take over the major European OEMs and value chains at the same time, this would possibly shrink the very working people market they need to buy their vehicles. Or, find a way to support jobs in Europe, thus recalibrating there own country's supply base. Tricky...!!!

One thing I do know, Mr William Wang (MG / SAIC) will have studied the minutest of detail. Not just from the quality of suppliers, contractors, but through to the legal ramifications of any error, for current and future EU automotive and car-buying labour market and the regulations that keep authorities away from the factories gates.

China, whether people want to believe it or not, is not solely in the hands of its premier alone, there is always a 5 year plan, this ethos permeates into their more studious organisations. There is also breadth and depth in their automotive model.

We in the 'west' need to step up, and plan for the longer-term rather than the next quarterly earnings report. Or else, well, actually all economies will lose out. The automotive industry really is that important to global economies...!!!