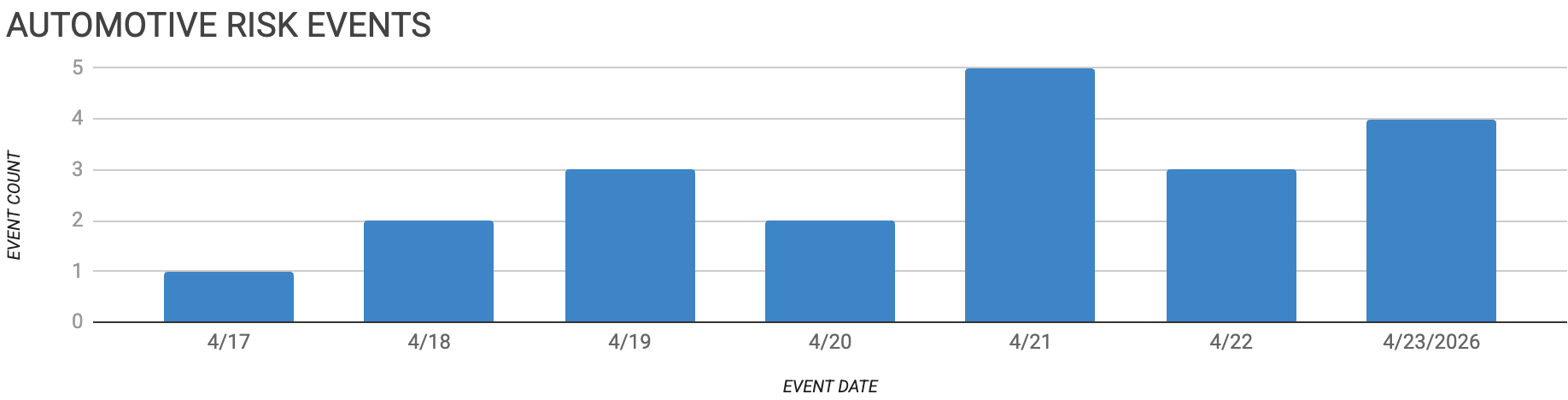

Automotive Supply Chain Risk Digest #479

April 17 - 23, 2026, by Elm Analytics

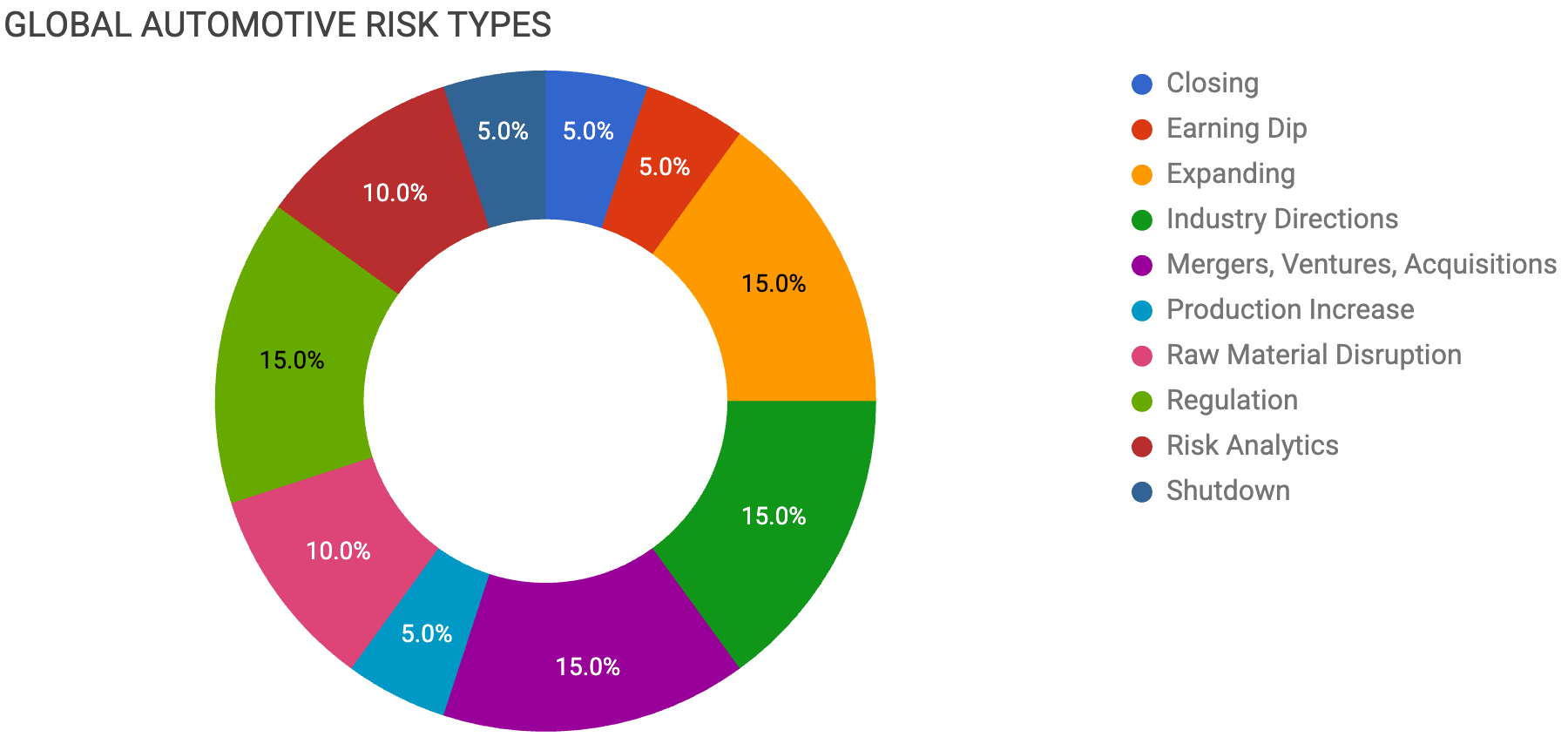

Contents

CLOSING

Nemak to close Austria plant

EARNING DIP

Hyundai profit drops on tariffs

EXPANDING

Vibracoustic expands Mexico production capacity

SiEngine opens Qingdao chip facility

Valeo grows Wuhan R&D operations

INDUSTRY DIRECTIONS

GM delays next-gen electric trucks

SDV delays driven by integration complexity

China JVs pivot to global exports

MERGERS, VENTURES, ACQUISITIONS

Stellantis explores selling European plants

Hangsheng Autoliv launch electronics joint venture

Sony Honda scales back EV venture

PRODUCTION INCREASE

Serra Verde boosts rare earth output

RAW MATERIAL DISRUPTION

Japan faces aluminum supply crisis

Aluminum shortages worsen EV demand pressures

REGULATION

US says tariffs will remain

New limits proposed on auto imports

Changan considers Spain production plant

RISK ANALYTICS

Automaker confidence declines amid tariffs

Suppliers expect worsening pricing pressure

SHUTDOWN

Honda cuts China ICE capacity

Closing

Nemak, a Mexico-based aluminum components supplier, plans to close its Herzogenburg, Austria, plant by the end of Q1 2027, cutting about 330 jobs. The company, citing deteriorating market conditions and low production volumes, will work with customers to relocate remaining products to other Nemak sites. Nemak only recently acquired the plant from GF Casting Solutions, a subsidiary of Swiss industrial company Georg Fischer. The closure is another signal of tightening conditions for aluminum component suppliers in Europe as automakers rationalize their supply bases.

Earning Dip

Hyundai Motor reported a 31% drop in Q1 operating profit to $1.7B, hit by 15% US tariffs and supply chain disruptions tied to the Middle East conflict. Rising prices for steel, nickel, lithium, platinum, and other raw materials added roughly $134.8M in cost pressure. CEO Jose Munoz said Hyundai will not be able to fully reallocate lost Middle East sales to other regions due to manufacturing constraints, and noted the Middle East had been the company’s highest-margin market. Hybrid vehicle sales provided a bright spot, reaching nearly a quarter of Hyundai’s total US sales as consumers responded to soaring gasoline prices.

Expanding

German anti-vibration systems supplier Vibracoustic is expanding in Querétaro, Mexico, with a second manufacturing plant that will increase production capacity for engine mounts, chassis bushings, and advanced vibration-control systems.

After completing initial construction, Chinese automotive chip designer SiEngine Technology has launched operations at a new subsidiary in Qingdao, further expanding its industrial presence in northern China. The facility includes an R&D center and is focused on its smart cockpit chip and ADAS chip.

Meanwhile, French supplier Valeo is expanding its headlight factory and R&D operations in the Wuhan Economic and Technological Development Zone, where it has operated since establishing a lighting joint venture in 1995. The Wuhan site now ships nearly 4M headlights annually to global markets and houses over 1.5k engineers, roughly one-third of Valeo’s total R&D workforce in China.

Industry Directions

General Motors has indefinitely delayed its next-generation full-size electric truck program, informing suppliers that refreshed versions of the GMC Sierra EV, Chevrolet Silverado EV, and Hummer had been halted with no new timetable. The current electric trucks will continue production at Factory Zero in Detroit-Hamtramck, but GM is diverting resources to its new T1-2 gas engine platform at Orion Assembly and has engaged suppliers to develop an extended-range EV propulsion system similar to those planned by Ford and Stellantis. GM has taken more than $7B in EV write-downs to date. Supplier executives and analysts do not expect a new generation of GM’s electric truck line until 2030 or beyond.

Elektrobit CEO Maria Anhalt said European automakers are not losing the software-defined vehicle race due to a talent shortage, but rather because of integration complexity and duplicated effort. Poorly defined interfaces between suppliers lead to what Anhalt called “integration hell,” a situation where conflicts between infotainment and telematics code can take months to resolve. In contrast, Chinese automakers gain their edge through faster decision-making, modular development, and parallelized workflows, approving architecture changes in weeks rather than months. Anhalt said the fix is pragmatic: stop reinventing software for every vehicle, apply higher SDV levels only to user-facing systems like cockpits, and reuse code across models, brands, and generations.

A growing number of China-based joint ventures are transforming their factories from domestic-only operations into global export hubs, driven by idle capacity and the cost advantages of China’s supply chain. Yueda Kia has exported more than 500k vehicles from its Yancheng plant, while Beijing Hyundai’s exports surged 49% in 2025 to 82k units. The shift extends beyond simple capacity reallocation: JVs are now exporting Chinese electrification and intelligent driving technologies through partnerships such as Stellantis-Leapmotor and joint ventures such as Smart (Mercedes-Benz/Geely) and Spotlight (Great Wall/BMW). The trend marks a reversal of the traditional JV model, with China moving from importing foreign technology to exporting automotive manufacturing capability, integrated supply chains, and faster product development to global markets.

Mergers, Ventures, Acquisitions

Stellantis has identified four factories in Europe that it may sell or share to address overcapacity. Sites in Rennes (France), Cassino (Italy), Madrid (Spain), and a fourth location are under discussion. Earlier this month, Dongfeng representatives toured the Rennes and Madrid plants. While current talks center on sharing facilities to fill excess capacity in exchange for access to Chinese technology, outright sales could also occur. Next month, CEO Antonio Filosa is expected to outline further strategic steps at a capital markets day.

Hangsheng Electronics, a Chinese automotive electronics supplier, and Autoliv, a Swedish safety technology company, have formally launched their joint venture, Suzhou Hangsheng Autoliv Automotive Electronics. The launch took place at Hangsheng’s manufacturing base in the Changshu Economic and Technological Development Zone. Focused on automotive safety electronics, the JV brings together Hangsheng’s focus on smart cockpits, connected-vehicle systems, and new-energy controls with Autoliv’s safety technology.

Honda and Sony are scaling back operations of their Sony Honda Mobility joint venture, absorbing employees back into the parent companies just a month after canceling the first and second Afeela EVs planned for North America. With about 400 employees, the venture fell victim to the same market forces that led Honda to cancel three EVs in March and book up to $15.8B in restructuring charges. Although production of the Afeela 1 sedan had begun at Honda’s East Liberty, Ohio, plant in fall 2025, the companies said they will continue discussions on future collaboration, focusing on software and advanced driver assistance systems.

Production Increase

Brazil’s Serra Verde Group is the target of a $2.8B acquisition by USA Rare Earth. While heavy rare-earth elements are currently dominated by China, the group expects about one-third of future production to come from these elements. The company’s Pela Ema operation in Goias currently produces approximately 100 metric tons of rare-earth oxides per year. However, production is being upgraded to reach about 6.4k tons annually by the end of next year. Approximately 32% of output will be terbium and dysprosium. These less common elements are essential for high-performance magnets used in EV motors and other automotive applications.

Raw Material Disruption

Japanese automakers and suppliers are currently facing an aluminum supply crisis due to the Iran conflict, which has disrupted key shipping routes in the Middle East. Domestic carmakers sourcing about 70% of aluminum imports from the region have seen prices jump 13% since hostilities began. Toyota supplier Denso, responding to the shortage, has already cut output by around 20k units per month. Most Japanese manufacturers hold roughly two months of inventory, so disruptions could begin by late April or early May. JPMorgan analysts warn that, even with a peace deal, the industry faces a ‘black hole’ due to refinery damage in Abu Dhabi and Bahrain, as well as ongoing shipping delays.

The underlying vulnerability runs deeper than the immediate conflict. Gulf smelters, which account for roughly 10% of global primary aluminum output, depend on a continuous power supply. Any interruption risks permanent damage to pot lines. Restarting idled facilities typically costs $50M to $100M per 100k tonnes of capacity. Rehabilitation takes 6 to 12 weeks, so even a brief disruption translates into months of reduced supply. Automakers face heightened risk: electric vehicles require 300 to 400 kg of aluminum each, compared to 210 to 250 kg for conventional vehicles. This intensifies demand pressure precisely as supply tightens.

Regulation

US Trade Representative Jamieson Greer told Mexico’s auto and steel industries during meetings in Mexico City that they should not expect USMCA renegotiation to eliminate tariffs, saying “tariffs are here to stay” and the US will never return to a zero-tariff world. The message landed hard in an industry where US buyers purchased 2.8M of the 4M vehicles Mexico produced in 2024, and where 60k auto-industry jobs were lost last year due to the 25% Section 232 duty. The two sides agreed to launch formal bilateral USMCA negotiations in Mexico City the week of May 25.

The Trump administration is also exploring additional measures to raise the cost of importing vehicles from Mexico and Canada, including a potential minimum US parts-content requirement and limits on automakers’ ability to reduce tariff rates under the USMCA. The considerations reflect frustration that tariff policies have yet to produce substantial reshoring of auto manufacturing, with the US still heavily reliant on imports for vehicles priced at $30k or less. One option under discussion could subject USMCA-compliant vehicle imports to an effective tariff of roughly 10%, higher than what Detroit automakers currently pay. Commerce Secretary Howard Lutnick called USMCA “bad industrial policy” and said it needs to be reconsidered, while Mexico’s deputy economy minister said there is no discussion of increasing auto tariffs or rules of origin at the negotiating tables.

Chinese automaker Changan is considering opening a plant in northern Spain, with the Aragon region under consideration, as it joins a growing list of Chinese manufacturers locating production in the country. European production would help Changan avoid EU tariffs of up to 30% on battery-electric cars imported from China, and the company plans to launch 8 new models in Europe over the next 3 years, with $2.3B in regional investment by 2030. Spain has become increasingly attractive to Chinese automakers, with Leapmotor set to produce at Stellantis’s Zaragoza plant, Chery assembling at a former Nissan site in Barcelona, and Santana Motors partnering with Dongfeng and BAIC. Spanish Prime Minister Pedro Sanchez visited Beijing this week as part of his effort to deepen economic ties with China.

Risk Analytics

Automaker confidence fell 3.6 points in Q1 to 54.6 on the Automotive News Auto Industry Confidence Index, with sentiment about future performance dropping to 49.6, indicating more automakers than not hold a pessimistic outlook. US tariffs, rising input costs, and geopolitical instability were cited as major challenges, and 50% of automaker respondents said they were pessimistic about industry health over the next six months. Average transaction prices and incentive pressure were the greatest areas of concern, with 44% of respondents expecting pricing performance to deteriorate. Nearly two-thirds of automakers said they were concerned about financial distress in their supply chains.

Suppliers scored even lower at 54.5, down from 57.1 in Q4 2025, with 60% of supplier executives pessimistic about industry health over the next six months. While current performance scored a relatively strong 63.9, future sentiment dropped to 45.1 as suppliers expect input costs to rise and pricing power with automakers to weaken further. Nearly half of suppliers expect their pricing leverage to deteriorate over the next six months, while just 4% expect it to improve. One supplier executive called it the most challenging environment in four decades, and 54% of parts makers expect financial distress across the supply chain to worsen.

Shutdown

Honda will shut down one of its joint-venture gasoline car plants with Guangzhou Automobile Group in June and is considering suspending another plant jointly owned with Dongfeng next year, further shrinking its China manufacturing footprint. Closing one ICE plant at each JV would halve Honda’s gasoline production capacity in China to about 480k units per year and cut total capacity from 1.2M to roughly 720k vehicles. Honda’s China sales fell about 24% in 2025 to just under 647k vehicles, nearly half the 1.2M cars it sold in 2023, as it lost ground to Chinese EV makers like BYD. The EV plants in Guangzhou and Wuhan are expected to begin producing EVs and plug-in hybrids developed under the leadership of Honda’s Chinese JV partners from 2028 or later.

Subtext = Non-China automotive OEMs handing vehicle manufacturing and development work to their competitors.

In the short-term, I kind of get it. Their strategy over the last 15ish years failed, and now its time to get revenue from where you can and rent out the assets to pass on financial liabilities. But, it digs a very big hole that will be hard to climb out of after the recession.