Automotive Supply Chain Risk Digest #476

March 27 - April 2, 2026, by Elm Analytics

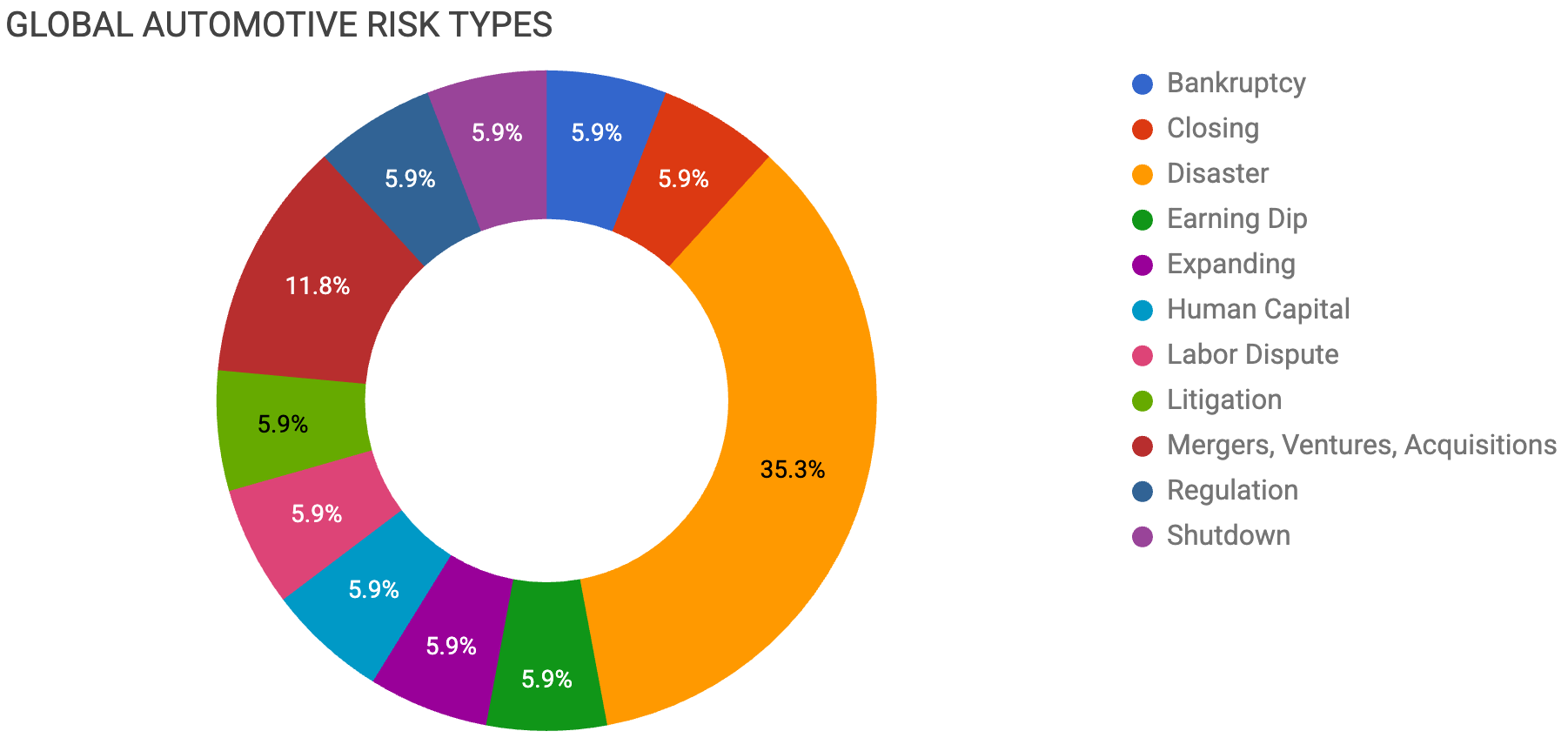

Contents

BANKRUPTCY

EV startup collapses, workers unpaid

CLOSING

Astemo plant closes after contract loss

DISASTER

March Plant Fires:

Michigan fire disrupts supplier output

Norway supplier fire halts JLR

Tennessee fire raises delivery risk

Ohio glass fire threatens OEM supply

Fatal Korea fire hits engine components

Texas chemical fire risks material flow

EARNING DIP

Ford sales fall due to fire/supply shortage

EXPANDING

Mercedes invests to expand US production

HUMAN CAPITAL

BYD 100k job cuts amid EV competition

LABOR DISPUTE

Webasto Michigan workers unionize

LITIGATION

ZF pricing dispute halts Stellantis production

MERGERS, VENTURES, ACQUISITIONS

Stellantis considers Canadian assembly of Chinese EVs

GM Chinese JV may produce in Mexico

REGULATION

US auto investments delayed over policy uncertainty

SHUTDOWN

GM idles Detroit EV plant amid weak demand

Bankruptcy

BeyonCa, a luxury EV startup founded by former Volkswagen executives in China, has shut down without producing a single vehicle, leaving hundreds of employees unpaid.

Despite backing from Renault, Dongfeng, and a Saudi investor group, the company never reached mass production.

Planned partnerships and a proposed factory never materialized, and management has gone silent on employee wage claims, prompting legal action.

The collapse underscores the competitive risks facing Chinese EV startups, the exposure investors carry in early-stage ventures, and the consequences of weak supply chain execution.

Closing

Customer concentration risk is also playing out domestically.

Astemo Americas will close its Tallapoosa, Georgia, plant after its primary customer terminated a contract covering parts for four vehicle models, resulting in about 60 layoffs.

The facility sits adjacent to Honda’s transmission operations, a proximity that makes the dependence on a single OEM all the more visible.

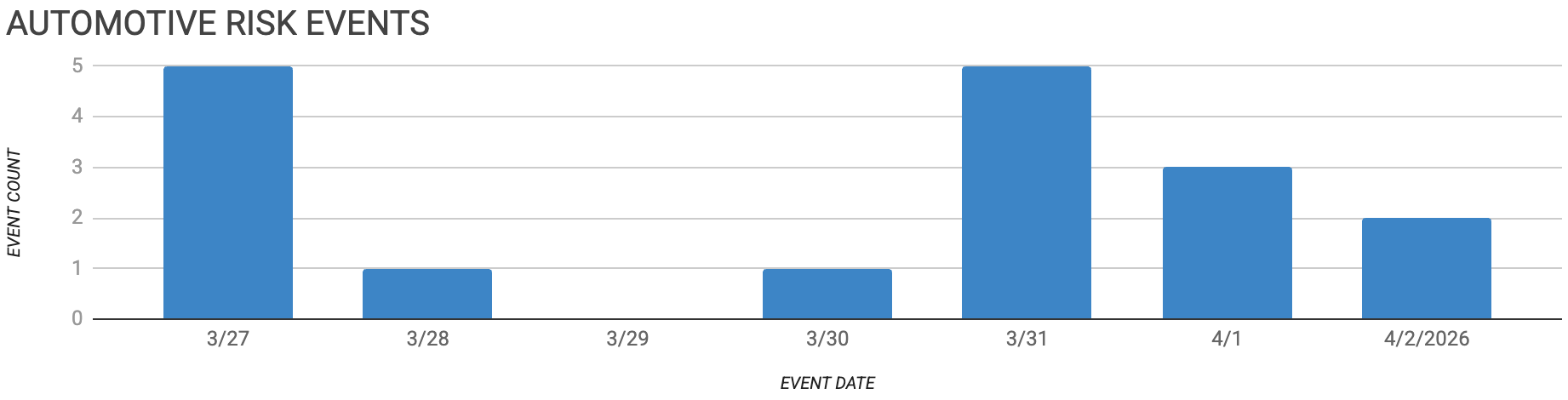

Disaster

Since March 1, 2026, several plant fires have highlighted how concentrated and interdependent automotive supply chains remain.

The most important incidents are not just the fires themselves, but the degree to which they affected Tier-1 suppliers, upstream chemical inputs, and just-in-time production networks.

The list below prioritizes events based on likely supply-chain impact rather than headline severity alone.

🟠 March 31–April 1, 2026 — Walker, Michigan — Challenge Manufacturing

Severity: 🔥🔥🔥🔥⚪ High-Medium.

What was manufactured: Precision metal stampings, welded assemblies, modular automotive parts.

Impact: Direct Tier 1 exposure; potential ripple into body-in-white and assembly operations.

Potential customers affected: Major OEM platforms and large automotive customers.

Notes: Challenge is deeply embedded in automotive production networks; machine damage or cleanup time may affect near-term availability.

Source: Local reporting / Yahoo

🟠 March 31, 2026 — Solihull, UK — supplier-fire-linked JLR production pause

Severity: 🔥🔥🔥🔥⚪ High-Medium.

What was manufactured: Supplier-side incident; not the OEM plant itself.

Impact: Very high because the fire reportedly forced an OEM production pause.

Potential customers affected: Jaguar Land Rover Solihull operations.

Notes: JLR said the pause was due to a parts-supply issue, and later reporting linked it to a fire at a supplier in Norway; the supplier name has not been publicly disclosed. This is a clear example of supplier-side fire risk translating into OEM downtime.

Source: Reuters / BBC / Wards / Automotive Logistics

🟠 March 25, 2026 — Chattanooga, Tennessee — Gestamp plant

Severity: 🔥🔥🔥⚪⚪ Medium.

What was manufactured: Structural stampings, welded assemblies, hot-stamped parts, chassis/body components.

Impact: Contained fire, but still meaningful Tier-1 risk due to just-in-time synchronization.

Potential customers affected: Volkswagen, BMW, Mercedes-Benz.

Notes: Even contained fires can create short-term delivery delays or quality checks at Tier-1 stamping plants.

Source: WDEF / Chattanooga Fire Dept.

🟠 March 22, 2026 — Moraine, Ohio — Fuyao Glass America plant

Severity: 🔥🔥🔥🔥⚪ High-Medium.

What was manufactured: Automotive glass.

Impact: Direct relevance to OEM final assembly and replacement-glass supply.

Potential customers affected: Major automakers using Fuyao glass, aftermarket glass channels.

Notes: Classic just-in-time risk; glass disruptions can halt assembly if inventory is tight.

Source: WCPO / WYSO / Dayton 24/7 Now

🔴 March 20, 2026 — Daejeon, South Korea — Anjun Industrial auto parts plant

Severity: 🔥🔥🔥🔥🔥 High.

What was manufactured: Engine valves / auto parts.

Impact: Direct supplier disruption with clear exposure to Hyundai and Kia engine programs.

Potential customers affected: Hyundai, Kia.

Notes: Fatal fire at a critical auto parts supplier; high-confidence risk for engine-component continuity and recovery timing.

Source: Reuters

🟠 March 12, 2026 — Pasadena, Texas — LyondellBasell Bayport Choate chemical plant

Severity: 🔥🔥🔥⚪⚪ Medium.

What was manufactured: Propylene oxide, propylene glycol, propylene glycol ether, TBA, isobutylene, ETBE.

Impact: Indirect but important exposure through coatings, plastics, antifreeze, and other auto inputs.

Potential customers affected: Chemical customers supplying OEMs and Tier 1s.

Notes: Chemical feedstocks sit far upstream in the automotive supply chain, so visibility is often limited, and impacts can ripple across multiple upstream suppliers before reaching OEMs. That makes this more of a systemic materials-risk event than a simple single-site disruption.

Full disclosure: Elm Analytics’ supplyAware™ platform helps teams better understand multi-tier plant risk and mitigation, including fire impact, through our Facility Risk module, developed in partnership with Aon.

Earning Dip

The financial toll of supplier fires is most visible at Ford. US sales fell 8.7% in Q1, driven mainly by a 16% drop in F-Series volumes as the fire at Novelis’ aluminum plant continues to constrain supply.

The disruption is delaying high-margin fleet deliveries, and full supplier output is not expected until summer, pointing to an uneven recovery through mid-2026.

Ford plans to offset the shortfall by raising truck production and skipping summer shutdowns, though near-term inventory gaps may still affect peak selling periods.

The company is also shifting its mix toward larger SUVs. Separately, EV sales dropped 70%, and hybrid sales fell 19%.

The combined picture underscores Ford’s continued exposure to single-source supplier risk, with effects spanning production, revenue mix, and inventory stability.

Expanding

While Ford manages the fallout from supplier disruption, other OEMs are investing to reduce that exposure.

Mercedes-Benz plans to put $4B into US manufacturing by 2030, signaling a deeper push to localize production and manage trade risk.

The company will expand output at its Tuscaloosa plant, add new ICE and EV models, and bring GLC SUV production to Alabama.

At full capacity, the plant could reach 340k units, raising demand for both local suppliers and skilled labor.

The investment gives Mercedes-Benz more flexibility to navigate uneven EV demand, evolving trade rules, and ongoing supply chain disruptions.

Human Capital

The pressure to localize is not limited to Western OEMs.

BYD cut its workforce by about 100k employees in 2025, a 10% reduction that brought total headcount to 870k as the company shifted from volume growth toward cost control.

Despite the cuts, BYD posted record revenue and delivered 4.6M vehicles, including over 1M exports.

Profit fell 19%, however, weighed down by pricing pressure and continued investment in EV and battery technology.

The company is targeting 1.5M exports in 2026, supported by new fast-charging battery technology and sustained R&D spending.

As EV competition intensifies, the pricing pressure behind these moves will likely drive further supply chain cost optimization, squeezing margins and reshaping supplier demand.

Labor

Cost pressures are surfacing on the labor side as well. Webasto workers in Michigan voted to unionize, a decision covering 475 employees who support Ford and other Detroit Three programs.

The vote followed earlier labor tensions at the site. The outcome points to rising union activity within the supplier base, with potential implications for labor costs and workforce stability across OEM supply chains.

Litigation

Supplier cost disputes are creating their own production risk.

Stellantis halted production at its Toluca, Mexico, plant on March 14 after ZF Chassis Modules stopped shipping suspension modules from its Windsor, Ontario, facility due to a pricing dispute.

The stoppage immediately paused assembly of the Jeep Cherokee and Compass.

ZF also threatened to cut shipments to Stellantis’s Windsor, Canada, plant, which would have disrupted production of the Chrysler Pacifica and Dodge Charger.

A Michigan court intervened with a temporary restraining order requiring shipments to continue, preventing a second shutdown.

In Mexico, Stellantis expects a separate court order to restore supply and allow operations to resume shortly.

The financial stakes are substantial: Stellantis says it had already paid more than $26M and accepted earlier price increases before the supplier sought an additional $70M, triggering litigation.

The dispute illustrates how pricing conflicts can halt production and create parallel risk across multiple plants, especially under just-in-time inventory conditions.

Mergers, Ventures, Acquisitions

Stellantis is also rethinking its North American footprint beyond supplier disputes.

The company is evaluating a plan to assemble Leapmotor EVs at its idled Brampton, Ontario, plant using knock-down kits from its Chinese partner.

The proposal follows Stellantis’s decision to shift previously planned Jeep production to the US, leaving the Brampton facility without a product.

Government and labor groups have pushed back, arguing the plan would rely heavily on imported components and offer limited engagement with local suppliers.

That opposition is sharpened by the fact that Stellantis received more than $500M in subsidies tied to domestic production and employment commitments, now under dispute.

Trade dynamics add further complexity: reduced Canadian tariffs on Chinese EVs, combined with potential US restrictions, could limit export options and constrain the plant’s scale.

The plan signals a move toward cost-driven sourcing but introduces risks around localization, supplier participation, and exposure to shifting trade policy.

GM is pursuing a different localization path. The company and its SAIC-GM-Wuling joint venture are planning to manufacture vehicles in Mexico, using existing GM facilities to avoid tariffs and strengthen its competitive position in regional export markets.

Regulation

GM is not alone in reshaping its regional production strategy.

Toyota, Hyundai, Volkswagen, and Nissan are collectively planning tens of billions in US investments to expand production and reduce tariff exposure.

Final commitments, however, remain tied to uncertainty around USMCA renewal and potential vehicle duties.

Toyota’s $10B plan and Hyundai’s $26B commitment both hinge on clearer trade policy.

Localization targets reflect the same urgency: Hyundai is aiming for 80% of US sales to come from domestic production, while Nissan is accelerating US production shifts despite higher costs.

Executives stressed that long lead times across supply chains and manufacturing require stable policy before capital is committed.

The trend points to continued investment in US capacity, but trade policy uncertainty remains a key constraint on supply chain planning and localization timelines.

Shutdown

Even as automakers commit capital to US production, EV demand remains a weak spot.

GM temporarily idled its Factory Zero plant in Detroit starting March 16, laying off about 1.3k workers as demand for the Hummer EV, Silverado EV, and other high-priced models weakened.

The shutdown is the second in three months and follows earlier shift cuts, underscoring ongoing production adjustments to match softer EV demand.

The plant is expected to restart in mid-April, but GM has already scaled back its broader EV plans, including write-downs and the pause of battery investments.

Policy changes, particularly the removal of EV tax credits, have further reduced demand and lowered planned EV volumes.