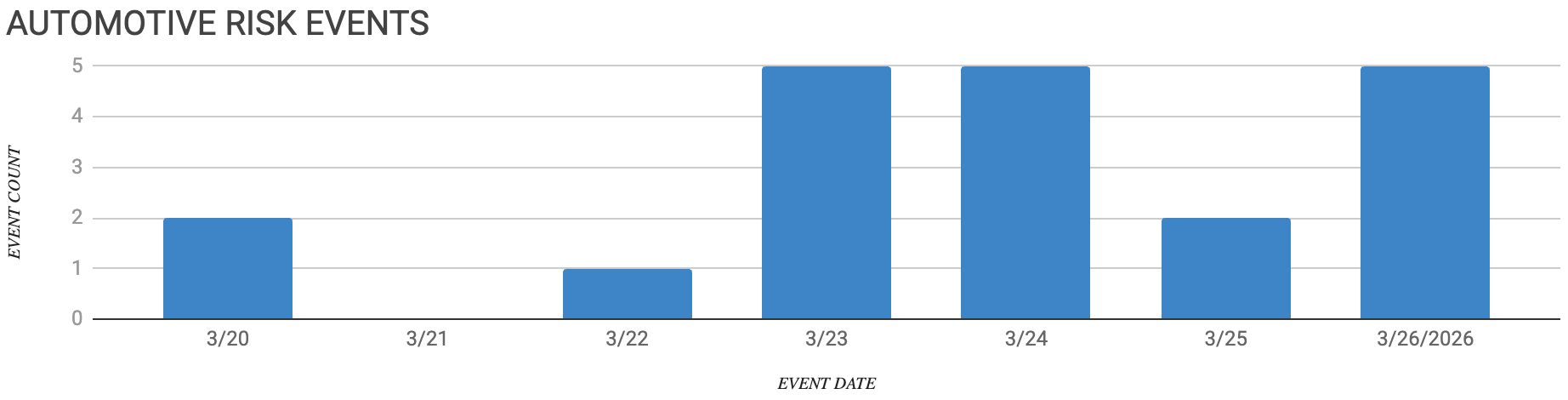

Automotive Supply Chain Risk Digest #475

March 20 - 26, 2026, by Elm Analytics

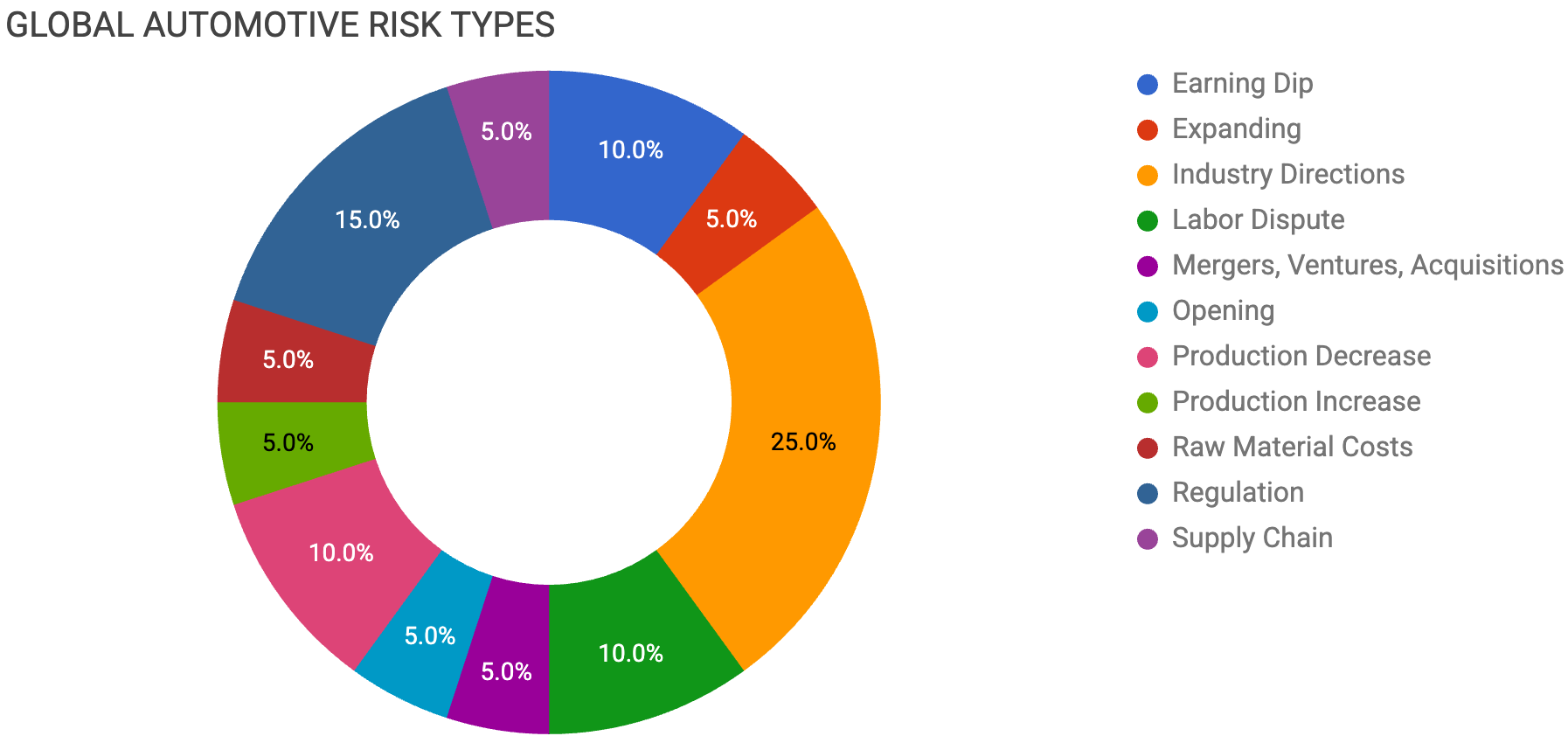

Contents

EARNING DIP

US vehicle sales forecast to fall

FedEx surcharges signal Iran war volatility

EXPANDING

Toyota invests $1B in US plants

INDUSTRY DIRECTIONS

Iran war hits India auto output

Oil shock boosts Asia EV demand

Toyota warns tariffs demand restructuring

Toyota pushes suppliers to raise productivity

Battery plants pivot from EVs

LABOR DISPUTE

GM Silao wage vote risks strike

Japanese wage hikes raise supplier costs

MERGERS, VENTURES, ACQUISITIONS

GM China venture faces uncertain future

OPENING

Valeo opens Texas plant for GM

PRODUCTION DECREASE

Honda cancels Afeela EV program

UK vehicle output posts sharp decline

PRODUCTION INCREASE

Hyundai targets 80% US-built sales

RAW MATERIAL COSTS

EU rules accelerate green steel adoption

REGULATION

European automakers absorb major tariff costs

USMCA review shapes North America trade

EU Australia deal boosts mineral sourcing

SUPPLY CHAIN

Iran conflict threatens Europe supply chains

Earning Dip

US new light-vehicle sales are forecast to fall 6.5% in Q1-2026, with March deliveries expected to drop 15% year over year as high prices and consumer uncertainty tied to the Iran conflict keep buyers out of showrooms.

The loss of federal EV tax credits is adding to the pressure, with EV sales estimated to be down 28% for the quarter and the seasonally adjusted annual rate at 15.5 million units. For supply chain planners, weaker near-term retail demand points to tighter production schedules and lower order volumes across the supplier base.

That softer auto demand is also showing up in freight markets.

FedEx reported higher fuel surcharges and flight re-routing away from the Middle East after the Iran war began. Analysts warn that higher gasoline prices will likely weigh on consumer spending and freight volumes in the months ahead.

Suppliers that depend on air freight for time-sensitive components should closely track surcharge increases and quickly assess alternative routes as Middle East disruptions continue.

Expanding

Even with current demand headwinds, Toyota is signaling a long-term commitment to North American manufacturing with a $1B investment split between its Georgetown, Kentucky, and Princeton, Indiana, assembly plants.

Georgetown will retool to launch three new EVs, including the 2027 Highlander and a Subaru-badged sibling, with batteries supplied from Toyota’s $13.9B complex in Liberty, North Carolina.

Princeton, meanwhile, will expand production of Grand Highlander and Sienna. For suppliers in Toyota’s North American network, the move offers a clear forward-program signal and aligns with Toyota’s broader $10B US commitment through 2030.

Industry Directions

While Toyota adds capacity in North America, the war in Iran is disrupting production in other key markets. In India, which imports about 50% of its natural gas from the Middle East, suppliers to Maruti Suzuki, Tata Motors, and Mahindra are reporting gas shortages at their factories.

S&P Global Mobility has therefore cut its 2026 India light-vehicle production forecast from 7.4% growth to 6.3%. The conflict is also pushing fuel prices higher worldwide. And although US EV interest is at its annual peak, analysts warn that the jump may not turn into lasting purchases.

The oil shock linked to the Iran conflict is driving a sharper rise in EV demand across Asia-Pacific. Before the route was effectively closed, about 80% of the oil moving through the Strait of Hormuz was headed there.

BYD in the Philippines and VinFast in Vietnam say sales rates are running at double or even quadruple their 2025 averages. In New Zealand, dealers reported electric and hybrid sales at four times the usual Saturday pace in mid-March.

For Asia-Pacific suppliers exposed to EVs, that points to a supply-constrained market that could last as long as the Hormuz disruption continues, especially with BYD’s overseas shipments already more than doubling in the first two months of the year.

That Iran-driven demand surge in Asia stands in sharp contrast to the structural cost burden weighing on North American operations.

Toyota COO Mark Templin has called the US tariff regime the biggest challenge of his career. The industry has identified more than $35B in tariff costs, with Toyota’s share above $9B, and Templin has made clear that pricing changes alone will not close the gap.

Suppliers should expect Toyota to push on all three response levers he identified: pricing, efficiency, and footprint, with more efficiency mandates, manufacturing footprint changes, and cost-reduction measures ahead.

The cost-reduction message reached suppliers directly days later. At the annual Toyota Supply Partners Convention, Toyota CEO Koji Sato told 700 executives from 484 supplier companies that the industry is fighting for survival and that productivity gains are not optional.

He pointed to several concrete actions, including the new Smart Standard Activity protocol, which eases overly strict cosmetic quality requirements, reduces supplier waste, and frees up resources for reinvestment. He also highlighted efforts to consolidate software platforms and powertrain variants.

Toyota’s network of suppliers will likely treat this as a clear action notice: incoming CEO Kenta Kon, who takes over on April 1, has made lowering Toyota’s break-even point a top priority.

Pressure on EV program economics is also reshaping the battery supply chain. Billions of dollars committed to new cell manufacturing capacity are being redirected away from automotive use.

Ford and LG Energy Solution are shifting newly built Michigan plants from EV cell production to battery energy storage systems after GM and Stellantis exited their respective LG joint ventures. LG has also secured new contracts with Tesla and Toyota to use that capacity.

For battery material and cell component suppliers, the pivot suggests that North American EV ramp-up timelines are stretching, and that near-term volumes will increasingly come from grid storage customers rather than automotive OEMs.

Labor

A more immediate supply chain disruption risk is emerging at GM’s Silao, Mexico, assembly plant. The union representing workers has proposed a 10% salary increase for the 2026-2028 contract period.

Workers will vote on the proposal on April 9 and 10, and the strike deadline is April 15 if no agreement is reached with management. Silao is a critical hub for GM truck and crossover production, so any work stoppage would quickly ripple through North American Tier-1 and Tier-2 supplier schedules.

Labor cost pressure is not limited to Mexico. In Japan, Rengo, the country’s largest union federation, reported an average wage increase agreement of 5.26% for 2026.

That marks the third straight year of hikes above 5%, with Toyota, Hitachi, and NEC all meeting full union demands.

For automotive supply chain professionals sourcing from Japanese Tier-1 and Tier-2 suppliers, wage inflation on this scale is likely to feed directly into component pricing talks and contract negotiations throughout the year.

Mergers, Ventures, Acquisitions

While labor costs climb in Japan, GM’s China joint venture faces a deeper structural challenge. SAIC-GM sales have fallen 75% from a 2017 peak of 2 million units to 562,000 in 2025, and the JV’s core contract expires in June 2027 with renewal terms still unresolved.

GM is investing $1.4B to revive Buick and Cadillac through locally developed EV and software-defined vehicle platforms. It is also exploring exports to new markets after the US and Mexico tariffs cut that business by 40% in 2025. Suppliers tied to SAIC-GM programs should expect ongoing volume uncertainty and watch JV contract developments closely as the June 2027 deadline nears.

Opening

Even as GM’s China-based supply footprint shrinks, the automaker is building new supply infrastructure in the US. French supplier Valeo is investing $225M in a McAllen, Texas, facility to produce central compute units for GM’s next-generation vehicle architecture.

That architecture is set to debut on the Cadillac Escalade IQ in 2028 and then expand quickly to other models. Located near the Mexico border, the plant is meant to serve both US and Mexican assembly operations and is a clear example of the nearshoring and software-defined vehicle investment trend reshaping the North American supply base.

Production Decrease

Honda’s EV retrenchment reached a major milestone with the cancellation of all Afeela-branded vehicles under its joint venture with Sony. The move follows Honda’s broader decision to cancel three 0 Series EVs and book up to $15.8B in restructuring charges.

The Afeela 1 sedan, already in production at Honda’s East Liberty, Ohio, plant, is being discontinued along with its planned crossover successor. The two partners are also reviewing the venture’s future as a whole.

Suppliers that committed tooling, engineering resources, or capacity to Honda’s 0 Series architecture or the East Liberty program now face direct exposure to those cancellations.

Honda’s pullback is part of a wider output contraction across global markets. In the UK, vehicle production fell 17% year over year in February, while commercial vehicle output dropped 74%. Exports, which make up 80% of total UK vehicle production, fell 11% for passenger cars and 65% for commercial vehicles.

The Society of Motor Manufacturers and Traders said those figures predate the Iran crisis, which suggests March could be weaker still. EU proposals that may discriminate against UK-built vehicles in a trading relationship worth nearly $89B a year add another layer of structural risk for suppliers operating in the UK.

Production Increase

Against that backdrop of weaker output elsewhere, Hyundai is pursuing an aggressive North American localization strategy. CEO Jose Munoz said at the company’s annual shareholder meeting that Hyundai aims to build 80% of US-sold vehicles domestically with about 80% US supply chain content by 2030.

The plan is backed by $26B in US investment and a pipeline of 36 new or significantly enhanced models through 2030.

With Hyundai and Kia reporting combined tariff costs of $5B in 2025, localization has become a financial necessity. US-based suppliers should expect active outreach as Hyundai works to increase US content from roughly 60% today to its 80% target.

Raw Material Costs

The push to localize and decarbonize supply chains is also speeding up the adoption of green steel in Europe.

A new EU automotive emissions framework allows low-carbon steel to offset up to 7% of a vehicle’s tailpipe CO2, giving the market a regulatory demand signal it has long lacked. VW has signed supply agreements with Salzgitter and Thyssenkrupp for green steel deliveries starting in 2026.

Analysts estimate the premium would add only $175 to $220 per vehicle for a model using 800kg of steel. For steel and materials suppliers, the EU framework may finally break the chicken-and-egg deadlock that has kept green steel investment below the level needed to scale supply.

Regulation

The regulatory and cost burden on European automakers is substantial. VW Group absorbed $3.2B in US tariff costs in 2025 alone, while BMW and Stellantis added about $1.5B and $1.3B, bringing the visible total for major European OEMs to more than $6B for the year.

VW CEO Oliver Blume has said publicly that the build-for-export model no longer works for some vehicles, and Stellantis expects another $1.8B in tariff costs in 2026 under the new US-EU trade framework. Suppliers with production in Mexico or Europe that depend on the US as an export market should now treat tariff exposure as a permanent structural cost rather than a temporary disruption.

In North America, the USMCA review process, which began on March 16, will determine whether cross-border flows of vehicles and parts can resume without the 25% tariffs that have reshaped production economics across the region.

Canada’s proposed tariff-remission overhaul would create tradable credits for the five automakers with Canadian assembly operations, Ford, GM, Honda, Stellantis, and Toyota, allowing brands without local production to buy tariff relief.

Even so, industry representatives are clear that restoring tariff-free USMCA trade remains the main objective. Suppliers with Canadian or Mexican content in US-bound vehicles should closely monitor the review, as its outcome will set the cost baseline for North American supply chains through the end of the decade.

The EU is also reducing supply chain dependence in another direction by finalizing a free trade agreement with Australia after eight years of negotiations.

The deal removes tariffs on Australian critical minerals entering the EU, including lithium, manganese, and aluminium. It is explicitly framed as a response to overreliance on China for battery and EV supply chain inputs, and it bans export restrictions on raw materials.

That gives European battery and EV manufacturers a more secure sourcing alternative. For automotive supply chain professionals seeking to monitor critical mineral exposure, the EU-Australia FTA is a meaningful diversification option that should grow in importance as EV volumes scale through the end of the decade.

Supply Chain

That push to diversify critical mineral supply chains becomes more urgent as the Iran conflict heightens broader supply chain risks.

The Vienna Supply Chain Intelligence Institute in Austria warns that if the conflict lasts more than two months, European automakers could face critical shortages of semiconductors and battery cells.

About one-third of the helium used in chip production comes from Qatar, and strong AI-driven demand for memory chips has left no slack in the system.

Automakers, including VW and BMW, say they have seen no immediate impact.

Even so, the institute argues that Europe’s supply chain resilience has weakened since the pandemic, leaving the industry more exposed to prolonged disruption than during the last major supply crisis.