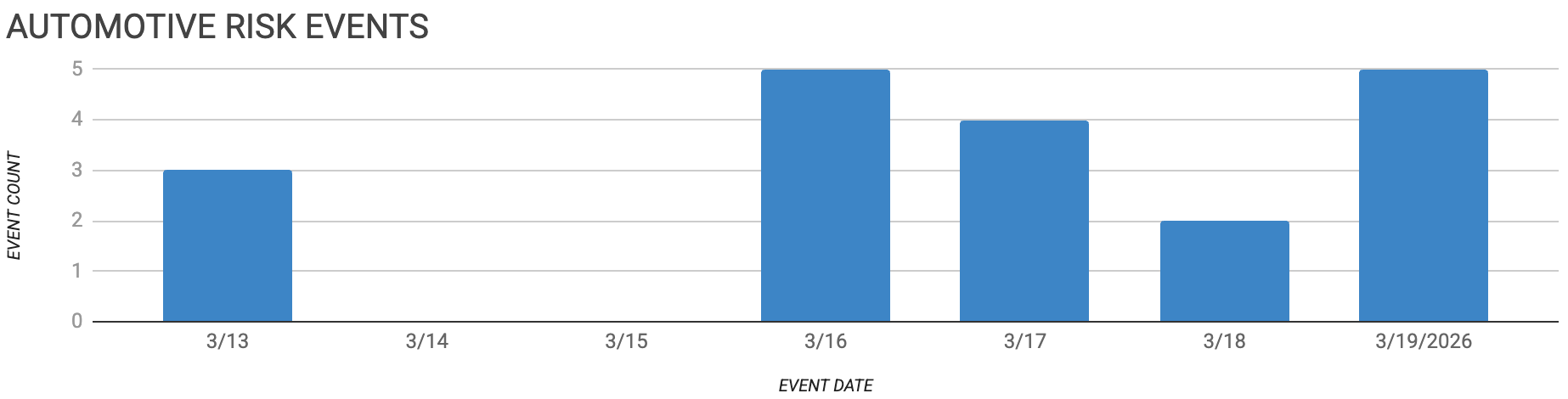

Automotive Supply Chain Risk Digest #474

March 13 - 19, 2026, by Elm Analytics

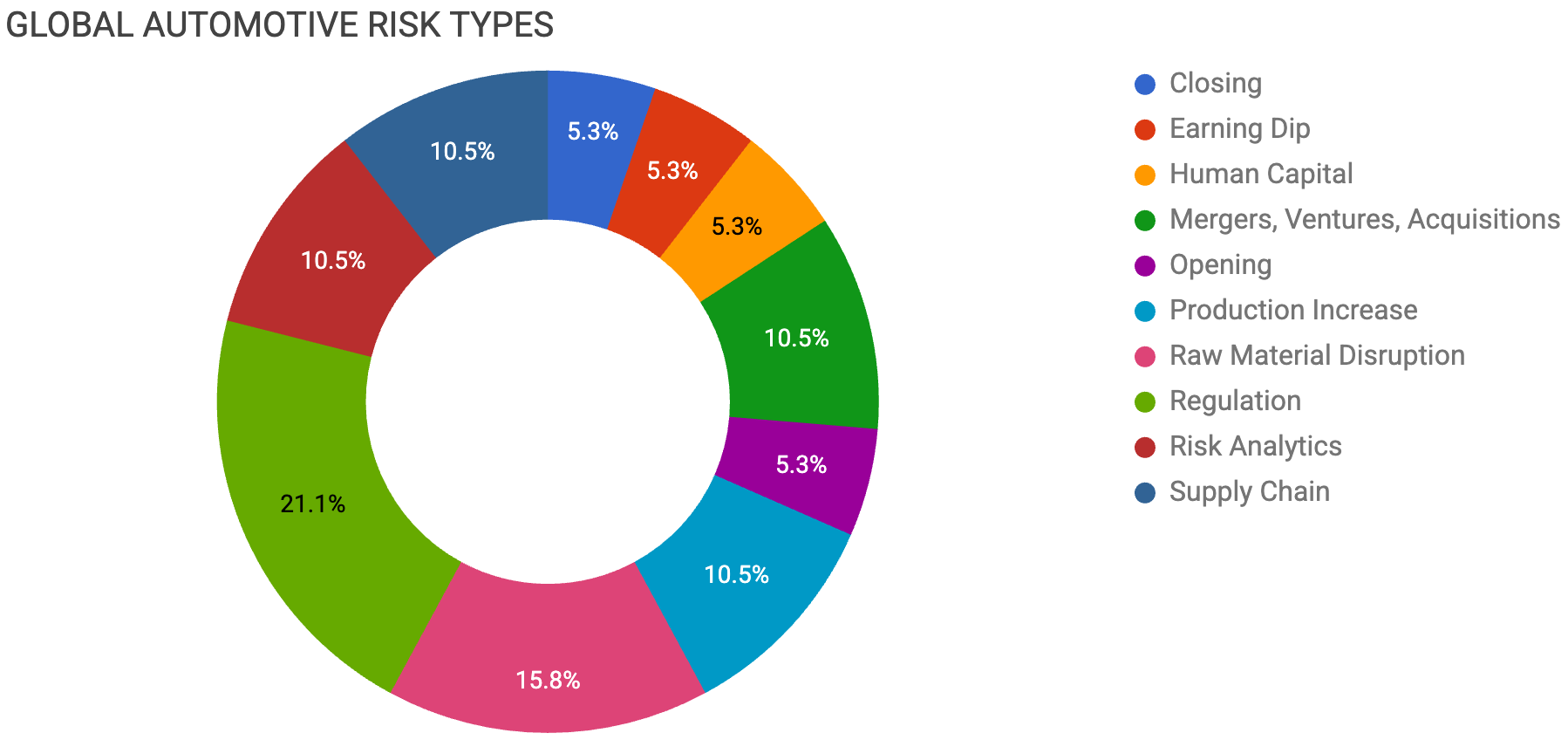

Contents

CLOSING

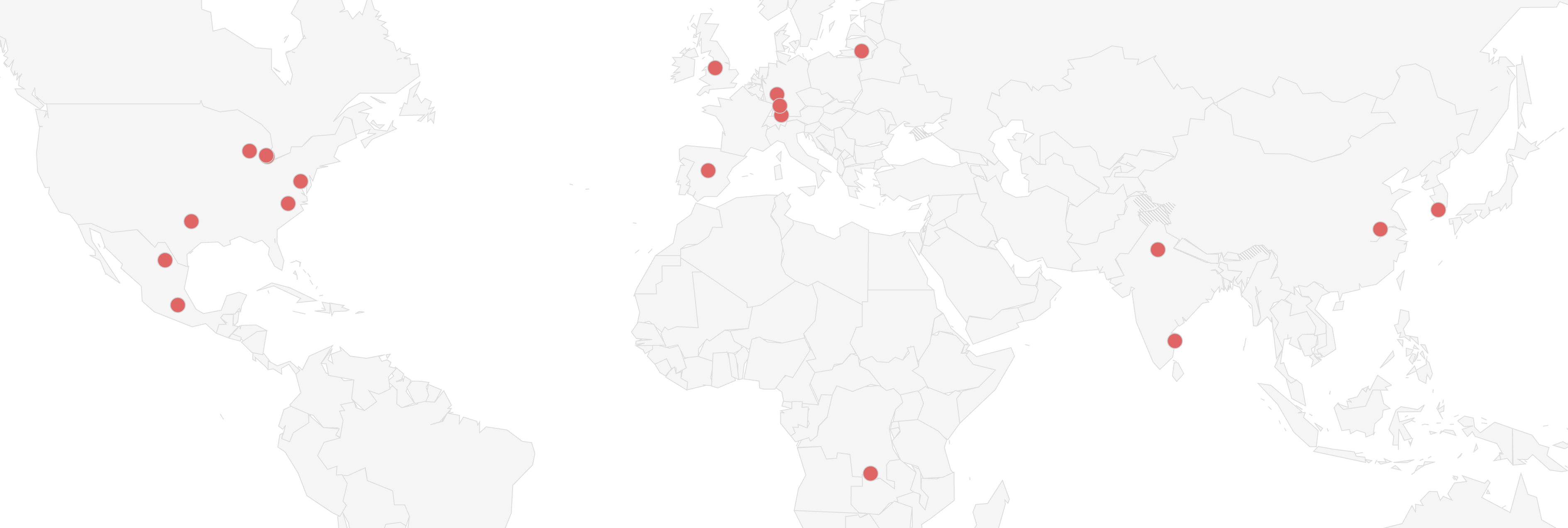

Aumovio closing Lithuania plant amid restructuring

EARNING DIP

ZF losses driven by EV exit

HUMAN CAPITAL

Bentley cuts jobs amid weak demand

MERGERS, VENTURES, ACQUISITIONS

Mercedes Geely expand EV partnership talks

Center Rock combines GHSP Stoneridge units

OPENING

VinFast delays NC plant, cuts workforce

PRODUCTION INCREASE

Leapmotor Stellantis to start Spain EV production

VW Anhui starts ID UNYX production

RAW MATERIAL DISRUPTION

ABS supply risk from Middle East

TPL halts PO production amid shortage

Glencore taps cobalt stocks amid crunch

REGULATION

Tariffs cost automakers billions

VW rethinks Mexico exports under trade pressure

New US trade probes cloud outlook

USMCA review deepens cross-border uncertainty

RISK ANALYTICS

IEEPA tariff refund guidance and pitfalls

BCG automotive supplier study 2026

SUPPLY CHAIN

India gas shortages disrupt auto production

Iran conflict risks demand and logistics

Closing

Aumovio plans to close its electronics plant in Kaunas, Lithuania, by mid-2028 as part of a global restructuring program expected to cost about $54M. The decision reflects weaker demand in Europe, underused capacity, and rising logistics complexity.

Earning Dip

ZF posted a $2.3B loss in 2025, driven mainly by $1.7B in write-downs tied to its exit from unprofitable EV programs. Revenue fell about 6%, and the company is cutting up to 14k jobs in Germany as EV demand continues to lag expectations.

Human Capital

Bentley will cut 275 jobs in the UK after its operating profit fell 42%, citing tariffs, weaker demand in China, and lower deliveries.

The company will delay further expansion of its EV programs due to limited customer interest, even as it prepares new launches. These actions underscore that demand remains volatile and that progress in electrification in the luxury market fluctuates.

Mergers, Ventures, Acquisitions

Mercedes and Geely are reportedly in early talks to expand their cooperation on future EVs to accelerate development and reduce costs in China.

The potential partnership would build on their existing Smart joint venture and reflects the industry’s growing reliance on Chinese engineering capability and scale.

Center Rock is combining GHSP with Stoneridge’s control devices unit to form a $550M supplier with broader electronics and systems capabilities.

The integration will span 12 global sites and 2k employees, with no site closures planned. Despite a $17.9M operating loss in 2025, the deal aims to improve scale and efficiency.

Overall, the combination reflects ongoing supplier consolidation and private equity-led restructuring as companies seek more scale and stronger capabilities amid rising technology complexity and margin pressure.

Opening

VinFast plans to restart construction on its delayed North Carolina EV plant in 2026, but it has pushed production back to 2028 and cut its projected workforce from 7.5k to 1.4k.

The $4B project has faced repeated delays, while the company posted a $2.8B net loss in 2025.

If VinFast does not begin production by mid-2026, North Carolina can reclaim the site, adding further pressure to the project’s timing and overall viability.

The situation highlights ongoing uncertainty around EV investment execution and demand, creating added risk for regional sourcing, capacity planning, and supplier commitments.

Production Increase

Leapmotor will begin building EVs in Spain with Stellantis in October, likely starting with the B10 SUV.

The partnership helps the company avoid tariffs, improve access to the local market, and develop lower-cost EVs, adding to competitive pressure across Europe’s supply chain.

Volkswagen Anhui has started production of the ID. UNYX 08 in Hefei, marking the first VW vehicle developed with Xpeng.

The SUV uses Xpeng’s Edward platform and reached production readiness in just 24 months.

The launch highlights the growing reliance on Chinese partnerships and local supply chains as automakers work to stay competitive in EVs.

Raw Material Disruption

LG Chem and Lotte Chemical have warned customers that ABS supply could be disrupted, and that force majeure could be declared if Middle East-related risks continue to affect feedstock availability.

ABS is a resin used in dashboards, door trims, and center consoles.

Supply could tighten by late March. Prices have already risen about 30% over the past two months, reaching about $1,550 per ton.

The companies have not declared force majeure, but they are urging customers to diversify sources and prepare for tighter supply.

This creates near-term risk for parts supply, higher material costs, and production continuity across the automotive supply chain.

TPL has suspended Propylene Oxide production at its Manali facility in India after losing access to propylene due to an Indian government directive prioritizing domestic fuel needs.

Because PO is used to make polyurethane for seats, dashboards, and insulation, the shutdown could tighten material availability for automotive interiors. The move adds fresh cost and continuity risk to an already strained supply chain.

Glencore is using cobalt held on China’s Wuxi exchange to supply EV battery customers after export curbs in Congo tightened global availability.

The restrictions have pushed cobalt prices up 160% since February 2025 and reduced Wuxi inventories by more than half since late January.

This raises ongoing raw material cost and availability risks for EV battery and electrification supply chains that depend on stable cobalt flows.

Regulation

Recent US tariffs have cost automakers $35.4B, with Toyota alone facing $9.1B and the Detroit 3 facing $6.5B in 2025.

Sourcing and production networks are being actively reshaped as companies respond by raising prices, shifting production, such as GM moving Buick to Kansas, and cutting imports, including VW’s ID Buzz.

Volkswagen’s model of building vehicles in Mexico and exporting up to 70% to the US is threatened by tariffs, costing the company $3.1B in the first nine months of 2025.

As a result, CEO Oliver Blume says these tariffs make exports "no longer economically viable."

This challenge is not unique to Volkswagen; Audi is also affected, with exports accounting for up to 90% of its Mexico-built vehicles.

Consequently, US sales for Audi have dropped 12% as tariffs impact pricing and competitiveness.

In response to these difficulties, VW is now considering shifting production to the US and expanding the Scout plant to build capacity. However, this move would be expensive, take years, and require a clearer trade framework.

The US and Mexico began USMCA review talks on March 18, with tariffs, especially a 50% US duty on steel, at the center of the discussion.

Broader talks are also focused on rules of origin, supply chain security, and reducing reliance on non-USMCA imports.

Mexico is pushing to preserve the agreement and eliminate tariffs, while the US is linking renewal to concerns about the presence of Chinese companies, labor standards, and energy policy.

The outcome will determine whether the pact is extended to 2042 or enters an annual renegotiation cycle, creating ongoing uncertainty for cross-border trade.

Risk Analytics

Foley published the last of their post-IEEPA-tariffs playbook series:

5. Refund-Related Issues for Companies That Indirectly Paid IEEPA Tariffs

6. Avoiding Common Pitfalls When Dealing with Refund-Related Issues

7. Understanding the Future Landing Spot for Tariffs

8. Setting Up to Receive IEEPA Tariff Refunds

Supply Chain

Natural gas shortages tied to the Iran-Israel conflict are disrupting India’s auto supply chain, with suppliers to Maruti Suzuki, Tata Motors, and Mahindra already reporting fuel constraints for production processes such as casting and painting.

India imports about 50% of its natural gas, and supply has tightened after Qatar halted output and shipments through the Strait of Hormuz declined, forcing the government to prioritize household energy over industry.

Smaller suppliers are already cutting output, with Kirloskar Ferrous halting some production and Hindalco declaring force majeure, while some OEM plants are running below capacity.

This creates immediate risk for production continuity and volume growth in a high-demand market, tightening capacity and increasing supply chain fragility.

German automakers, including BMW and Volkswagen Group, are monitoring the Iran conflict as a growing risk to Middle East demand and logistics.

While operations remain stable for now, Audi is already seeing a "temporary dent" in regional sales, and Skoda has flagged rising uncertainty in a market that had recently delivered over 10% growth for the VW Group.

Meanwhile, BMW is watching potential disruptions to aluminum flows routed through Dubai.

On the supply side, suppliers are also assessing logistics exposure: Bosch notes reduced air freight volumes, and Schaeffler warns that disruption to Suez Canal shipping would be critical.

Together, these developments highlight rising geopolitical risk to both demand and key logistics corridors, raising concerns about downstream impacts on materials flow and premium vehicle sales.