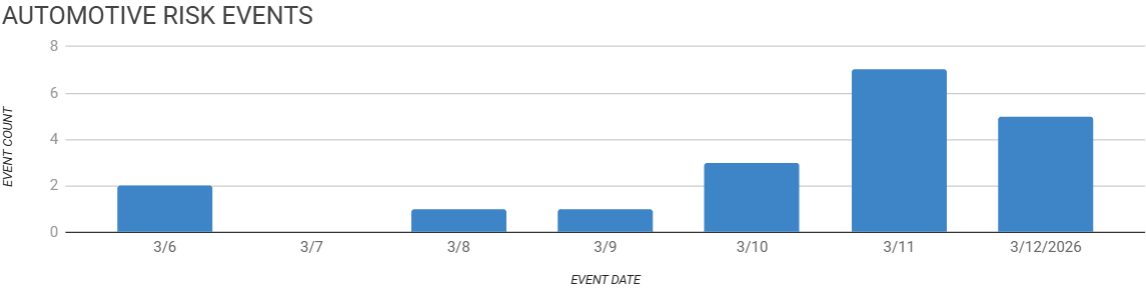

Automotive Supply Chain Risk Digest #473

March 6 - 12, 2026, by Elm Analytics

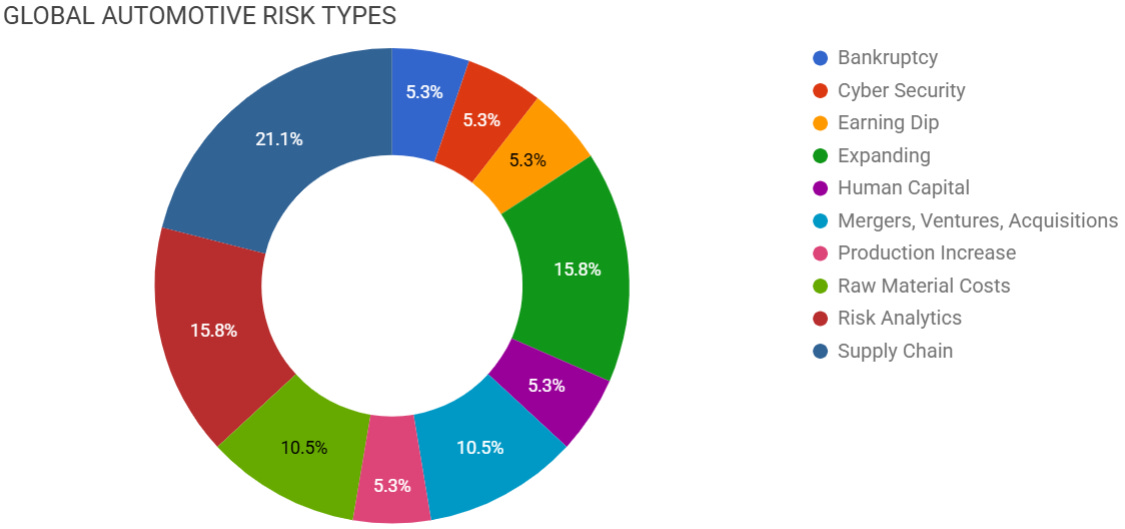

Contents

BANKRUPTCY

First Brands sells Walbro business

CYBER SECURITY

Hackers claim wiper attack on Stryker

EARNING DIP

Honda faces loss after EV pullback

EXPANDING

Renault targets global sales growth

NIO expansion plans face chip costs

Newman Technology expands Ohio production

HUMAN CAPITAL

SK Battery cuts Georgia workforce

MERGERS, VENTURES, ACQUISITIONS

Denso bids to acquire chipmaker Rohm

Stellantis explores Chinese investment partnerships

PRODUCTION INCREASE

Rivian R2 launch to boost deliveries

RAW MATERIAL COSTS

Diesel price spike pressures supplier margins

Aluminum supply disruption shifts sourcing

RISK ANALYTICS

Auto sector faces geopolitical economic shocks

Middle East war impacts automotive economics

Strait of Hormuz disruption threatens oil supply

SUPPLY CHAIN

Hormuz closure strains global LNG supply

War threatens Japanese auto export supply chains

Helium shortage worsens chip supply constraints

Ford introduces three-year supplier planning outlook

Bankruptcy

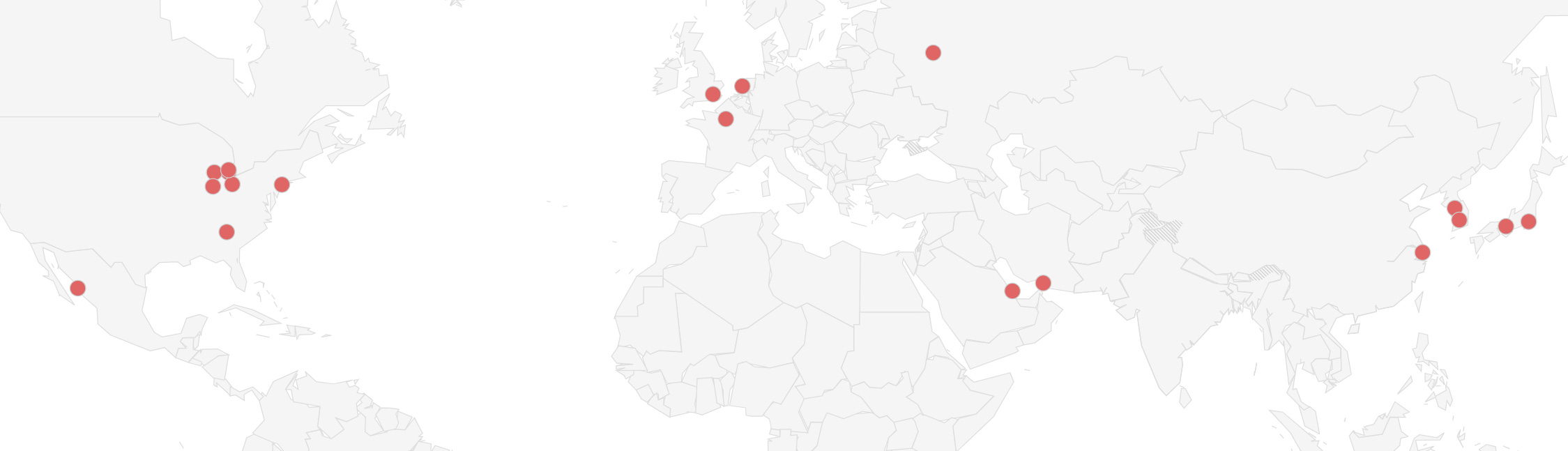

First Brands will sell its Walbro business to Active Dynamics Group for $50M as it moves through bankruptcy restructuring. The deal preserves 600 jobs in Michigan, Arizona, and Mexico and transfers a product line that includes fuel systems, carburetors, fuel pumps, and ignition components.

Cyber Security

Meanwhile, in cybersecurity, Iran-linked hacktivist group Handala claims it launched a data-wiping attack against Stryker, disrupting systems at the Michigan-based medical manufacturer and supplier.

Reports of wiped devices, halted operations, and ordering issues show how a cyberattack tied to a geopolitical conflict can spill into commercial supply chains far from the battlefield.

For automotive companies, the message of vigilance is clear: a civilian manufacturer can become collateral damage and lose the digital systems needed to keep production and supply moving.

Earning Dip

Shifting to corporate strategy, Honda expects its first annual loss since 1957, driven by up to $15.7B in EV restructuring charges and the cancellation of three planned US EV models.

The company says the move reflects weak EV demand, the end of US policy support, and rising competition from Chinese manufacturers. This signals a clear shift, as automakers increasingly pull back on EV investment to adapt to changing market realities.

Expanding

In a related move, Renault aims to lift global sales by more than 20% by 2030 and to have half of its vehicle sales come from outside Europe.

Over the next 5 years, it plans to launch 36 new models, several of which are tailored for markets such as India and South America.

The company also plans to cut EV costs and simplify vehicle designs to compete more effectively with lower-cost Chinese brands.

Continuing the trend of global challenges, China’s NIO plans to expand overseas over the next 2 to 3 years, but says the memory chip shortage is raising costs and could disrupt production.

The company expects chip and raw material shortages to increase the cost of each vehicle, but it plans to keep prices unchanged.

Newman Technology plans to invest $74M to expand its Mansfield, Ohio, facility, adding new injection molding production lines. The project is expected to create 70 jobs on top of the site’s existing 627 positions.

Newman, a Tier-1 supplier owned by Japan’s Sankei Giken Kogyo, makes door assemblies, exhaust systems, exterior trim, structural reinforcements, and molded plastic components for the auto industry.

Human Capital

However, the EV slowdown continues to affect other parts of the supply chain. SK Battery America cut 958 jobs, about 37% of its workforce at its Georgia plant, as weaker US EV demand eased pressure on battery output.

The factory had supplied Ford’s canceled electric F-150 Lightning program and also serves Volkswagen and Hyundai.

SK said it remains committed to building a US battery supply chain, but the cuts show how quickly softer EV demand and policy changes can ripple through battery manufacturing capacity and affect employment.

The layoffs are another sign that EV-related production footprints are being reset as automakers and suppliers adjust to slower demand growth.

Mergers, Ventures, Acquisitions

Denso has proposed acquiring Rohm, a Kyoto-based chipmaker with a strong presence in automotive semiconductors, as access to semiconductors becomes more important for EVs and self-driving systems.

The bid follows a strategic partnership announced in May 2025 and reflects a broader industry shift toward securing semiconductor technology and supply through deeper supplier ties or direct ownership.

Stellantis is reportedly considering deals that would let Chinese automakers such as Xiaomi and Xpeng invest in its European operations, including possible stakes in brands such as Maserati and access to manufacturing capacity.

The talks reflect pressure on Stellantis’ European business, including overcapacity, intense competition, and high costs tied to the EV transition.

For Chinese partners, the appeal is faster access to European manufacturing.

For Stellantis, the potential gains include advanced EV and software technology.

The discussions also point to a broader strategic shift, as Stellantis directs more investment to North America and seeks external support to stabilize its European operations.

Production Increase

Meanwhile, Rivian plans to begin R2 deliveries this spring and expects the model to drive a 53% increase in total deliveries this year.

The company also expects the R2 to generate most of its volume growth in 2027. The launch matters because Rivian is relying on the R2 to scale production well beyond its current higher-end lineup.

Raw Materials

Rising diesel prices are quickly squeezing supplier margins across North America.

APMA’s Flavio Volpe said transportation usually makes up 5% to 6% of operating costs, so a 20% increase in fuel prices can add about 1% to total costs.

That is a meaningful hit in a business where margins are often only 6% to 7%.

Smaller suppliers are especially exposed because freight makes up a larger share of their cost base, and they have less ability to absorb the increase or pass it through.

Adding to sourcing headaches, disruptions tied to the Iran war are forcing Japanese and South Korean auto suppliers to look for alternative aluminum sources, including talks with Russia’s Rusal for primary foundry alloy used in wheels, engine blocks, and cylinder heads.

The shift follows a force majeure declared by Aluminium Bahrain and delayed loadings by Emirates Global Aluminium, two major Gulf suppliers to Japan and South Korea, after shipping through the Strait of Hormuz was disrupted.

Some Japanese buyers who had voluntarily avoided Russian metal since the 2022 invasion of Ukraine are now reconsidering purchases as prices rise and alternative supply tightens, while others are also exploring sources in India and elsewhere in Asia.

The situation shows how conflict-driven disruption in one trade lane can quickly force uncomfortable sourcing decisions for critical automotive raw materials.

Risk Analytics

Taken together, the auto sector is being hit by a confluence of shocks: rising oil prices, uncertainty over AI’s impact on jobs, tariffs, reduced consumer sentiment and spending, and war-driven geopolitical risk.

Stress in the $1.7T private credit market adds a parallel financing risk we're watching, as it has recently heightened fears of tighter credit and higher borrowing costs for automakers and suppliers.

S&P Global: Economic implications of war - Middle East war and the automotive industry

Reuters Graphics: How the Strait of Hormuz closure affects global oil supply

Supply Chain

It is important to note that the closure of the Strait of Hormuz affects much more than just oil supply and competition for liquified natural gas.

For example, the Middle East accounts for 10% of Japanese vehicle exports.

Aluminum production, which is energy-intensive, is becoming increasingly constrained (see the force majeure under Raw Materials above).

Additionally, about a third of the world’s helium supply is also restricted, putting extra pressure on Asia’s electronics industry and worsening the memory-chip shortage, with demand already outpacing supply by 40% to 50%.

Petrochemical shipments, such as ethylene glycol, are slowing too, which is impacting the production of automotive plastics.

Ford plans to give suppliers a 3-year outlook on vehicle programs to improve planning and help address quality issues.

The company will also introduce a two-way scorecard and a help desk to improve communication and resolve problems faster.

The effort is part of a broader push to rebuild supplier relationships after several years of strained ties.