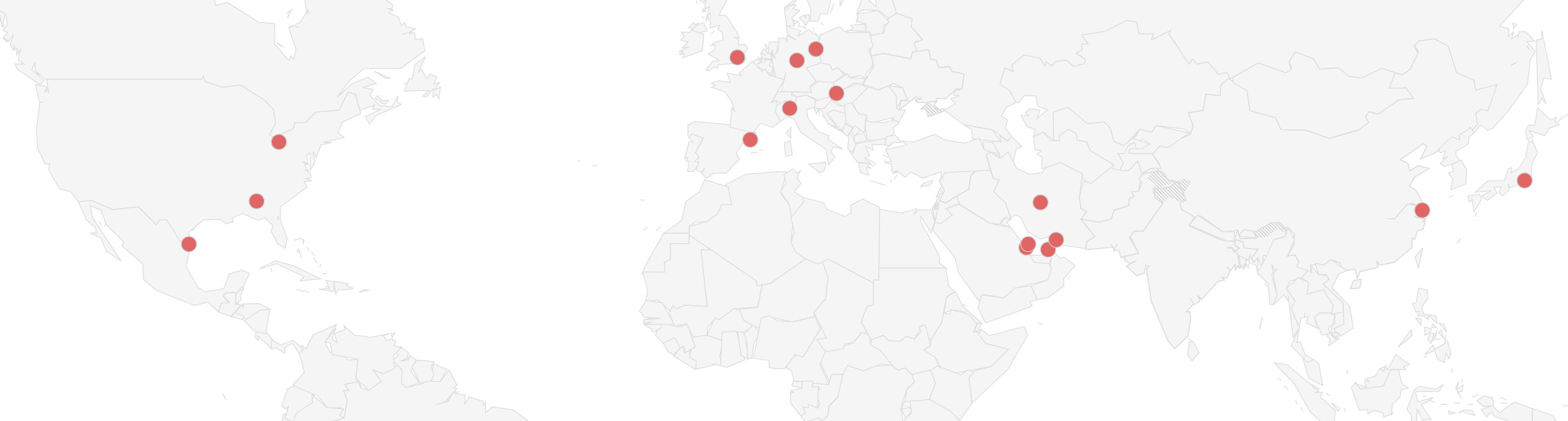

Automotive Supply Chain Risk Digest #472

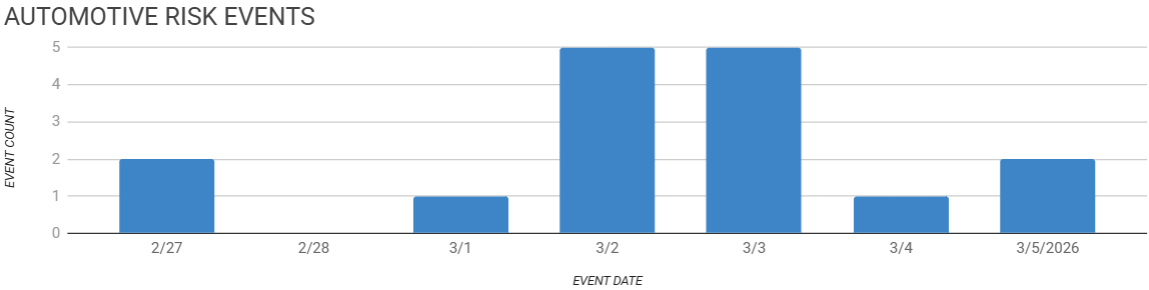

February 27 - March 5, 2026, by Elm Analytics

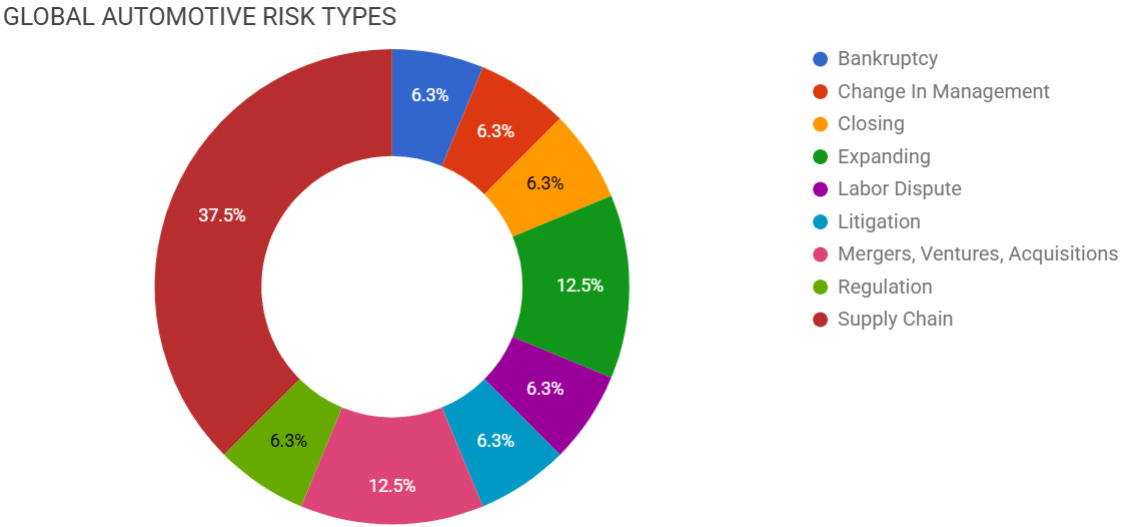

Contents

BANKRUPTCY

First Brands sells factories to survive

CHANGE IN MANAGEMENT

Auto CEO turnover hits record pace

CLOSING

First Brands shutters four Ohio sites

EXPANDING

Shinhwa expands Alabama production footprint

Astotec boosts pyrotechnic initiator capacity

LABOR DISPUTE

IG Metall labor push falls short at Tesla Berlin

LITIGATION

Wingtech threatens $8B Nexperia claim

MERGERS, VENTURES, ACQUISITIONS

MG narrows hunt for Europe facility

GKN drops European magnet plant

REGULATION

Italy seizes CEVA Logistics funds in probe

SUPPLY CHAIN

Iran conflict rattles global supply chains

Hormuz rerouting slows parts shipments

Gulf disruption tightens automotive logistics

Qatar LNG shutdown heightens energy risk

Europe suppliers face gas-cost pressure

Qatar LNG restart may take weeks

Bankruptcy

Bankrupt auto supplier First Brands is selling its remaining factories, including three that supply Ford, to avoid liquidation.

With four potential buyers in the mix, the company is operating week to week as talks continue, while automakers, including Ford, provide advance payments and other funding to keep production running.

Ford’s attorney called the support unprecedented:

“This may be the most expensive parts deal in the history of auto supply.”

- Mark E. Freedlander, attorney for Ford Motor Co.

The case highlights the risk of severe production disruptions and financial fallout when key suppliers come under distress.

Change In Management

Since early 2025, nine global automakers, Toyota, BMW, Nissan, Stellantis, Renault, Volvo, Jaguar Land Rover, Porsche, and Hyundai, have replaced their CEOs.

The leadership shake-up comes as the industry faces rising tariffs, tougher Chinese competition, and the shift to EVs and software-defined vehicles.

Analysts say boards are placing more weight on technology, AI, and digital expertise as automakers adjust strategy to volatile EV demand and new mobility rivals.

Some CEO changes followed business crises or strategic disagreements, including at Stellantis and Renault, while others were part of planned succession.

The rapid turnover highlights the pressure on automakers as they try to protect legacy vehicle profits while funding major investments in electrification and software.

Closing

First Brands will close four facilities in Ohio, including its headquarters in Cleveland and plants in Greenville, Tiffin, and Bowling Green, with 1.3k layoffs set by April 30

Expanding

Shinhwa Auto USA is investing $37M to expand its plant in Auburn, Alabama. The project brings Italian toolmaker SAPP into the operation and adds dedicated tooling capacity. That gives Shinhwa a more vertically integrated US manufacturing base for aluminum die casting, machining, and component assembly.

Austria’s Astotec Automotive has committed $10.7M to grow capacity at its plant in Pápa, Hungary. The site produces pyrotechnic igniters and micro gas generators for automotive safety systems, including airbags, seatbelt pretensioners, and battery disconnect devices.

Labor

IG Metall lost ground in the works council elections at Tesla’s Grünheide plant, winning 13 of 37 seats and falling short of the majority needed to press for collective bargaining.

The result leaves the factory as the only German automotive plant without a union contract.

Ongoing labor tensions at a site operating at about 40% of capacity could continue to weigh on production stability.

Litigation

Wingtech Technology may seek $8B in compensation under the China-Netherlands investment protection treaty if Dutch authorities keep blocking its control of Nexperia.

The dispute follows a court decision suspending Nexperia’s Chinese CEO and restricting Wingtech’s voting rights while an investigation into possible mismanagement continues.

Because Nexperia’s chips are widely used in vehicles, the case could prolong semiconductor supply risk for automakers.

Mergers, Ventures, Acquisitions

MG plans to build a European factory by 2027 and has shortlisted five countries as it looks to avoid 45% EU tariffs on Chinese-built EVs. The move could broaden regional supplier sourcing as the brand localizes production.

GKN has reportedly canceled its planned European rare-earth magnet plant, which was set to begin a pilot operation in Germany and could have supplied Schaeffler.

The project was one of only a few magnet production efforts planned in Europe and aimed to reach 4k metric tons of annual capacity by 2030.

It was said to have been dropped late last year, before GKN PM’s $1.44 billion takeover by Detroit-based American Axle & Manufacturing, now called Dauch Corp. The business was considered non-core, with uncertain profits due to changing EV demand and increased competition from China.

Regulation

Italian authorities seized $31.8M from France’s CEVA Logistics units in a tax and labor investigation tied to alleged false invoicing and labor-law violations.

CEVA supports automakers including Ford, Stellantis, Renault, and Volkswagen with parts transportation, sequencing, and logistics services.

Because many vehicle plants run on just-in-time schedules, disruptions at a provider like CEVA can quickly interrupt parts flow and threaten plant uptime.

Supply Chain

The US- and Israel-led attack on Iran, along with Iran’s retaliation, has intensified global supply chain disruptions.

Energy markets, shipping routes, and logistics costs are all affected. Iran’s closure of the Strait of Hormuz, a key energy chokepoint, has raised oil prices and threatened the supply of natural gas, oil, and petrochemicals.

Shipping lines are avoiding the area, and rerouting vessels around the Cape of Good Hope may add up to two weeks to transit times. This reduces vessel capacity and increases freight and insurance costs.

Vessel traffic through the Strait of Hormuz fell about 70% after the strikes, while Jebel Ali Port temporarily suspended operations and Gulf airspace closures cut global air cargo capacity by 18%.

Major carriers, including MSC, Maersk, CMA CGM, COSCO, and Hapag-Lloyd, halted or restricted bookings, rerouted services, and in some cases imposed war-related surcharges of $1.5k to $4k per container.

What does this mean for automotive supply chains?

Higher energy prices, increased risk to petrochemical feedstock, and longer shipping lead times may raise production costs and disrupt the movement of parts and raw materials.

For automotive manufacturing, the bigger risk is execution: Asia-Europe flows are slowing, booking options are tightening, and just-in-time plants in Germany, the UK, the US, and Mexico could begin to feel component delays within weeks if disruptions persist.

While most are talking about the impact on oil, liquified natural gas (LNG) seems to have found itself in the eye of the perfect storm.

Qatar, one of the world’s largest LNG suppliers, has halted production, sending natural gas prices in Europe and Asia sharply higher.

With global LNG supply already tight and export facilities, including those in the US, already running at full capacity 🔊, lost Qatari volumes cannot be replaced quickly.

As a result, major importers such as China, Japan, and South Korea may face supply shortages if the shutdown lasts more than a few days. Europe looks especially vulnerable because gas inventories are already low.

This disruption has significant implications 🔊 for automotive manufacturing. A prolonged LNG shortfall could drive up electricity and industrial energy costs, increasing expenses for energy-intensive operations like metals processing and component manufacturing.

The greatest supply chain risk is in Europe, where suppliers of aluminum, steel, chemicals, and glass, all highly sensitive to natural gas prices, face heightened exposure if Qatari LNG remains offline.

Qatar’s complete LNG shutdown could last at least a month.

Restarting operations would require about two weeks, with an additional two weeks needed to reach full capacity.

These are worryingly difficult times for the majority of the business world. I suggest a thorough and comprehensive Context review of inward and outward elements of any current business system (not just your own operating model) for clarity of potential material impacts and what the tipping point could be (i.e. as an example not getting much time at present, what if Middle East investment funding gets pulled from the US). Stuff not looked at can surprise you.

Obviously, it also now a good time to review business continuity plans.