🎂 Automotive Supply Chain Risk Digest #469

February 6 - 12, 2026, by Elm Analytics

The Digest Turns 9 (Yes, Really)

Dear Reader,

This issue marks the 9th anniversary of the Automotive Supply Chain Risk Digest... which feels both impossible and exactly right, given how much supply chain chaos the world can pack into a single year.

Thank you for reading, sharing, challenging, and contributing. Every forward, every quick reply, every “this helped us make a decision” note is fuel. We aim to keep this practical: what’s changing, why it matters, and what you may want to do next.

Whether you’ve been here since the early days or you joined somewhere along the way, I’m genuinely grateful you’re part of this. Special thanks to the regular insightful commenters, recommenders, and the heart-icon faithful (Mark, you’re still undefeated!).

Onward to year nine. Same mission. Sharper lens... and hopefully fewer fire drills.

Warmly,

Nick Gaydos

Editor, Automotive Supply Chain Risk Digest

Contents

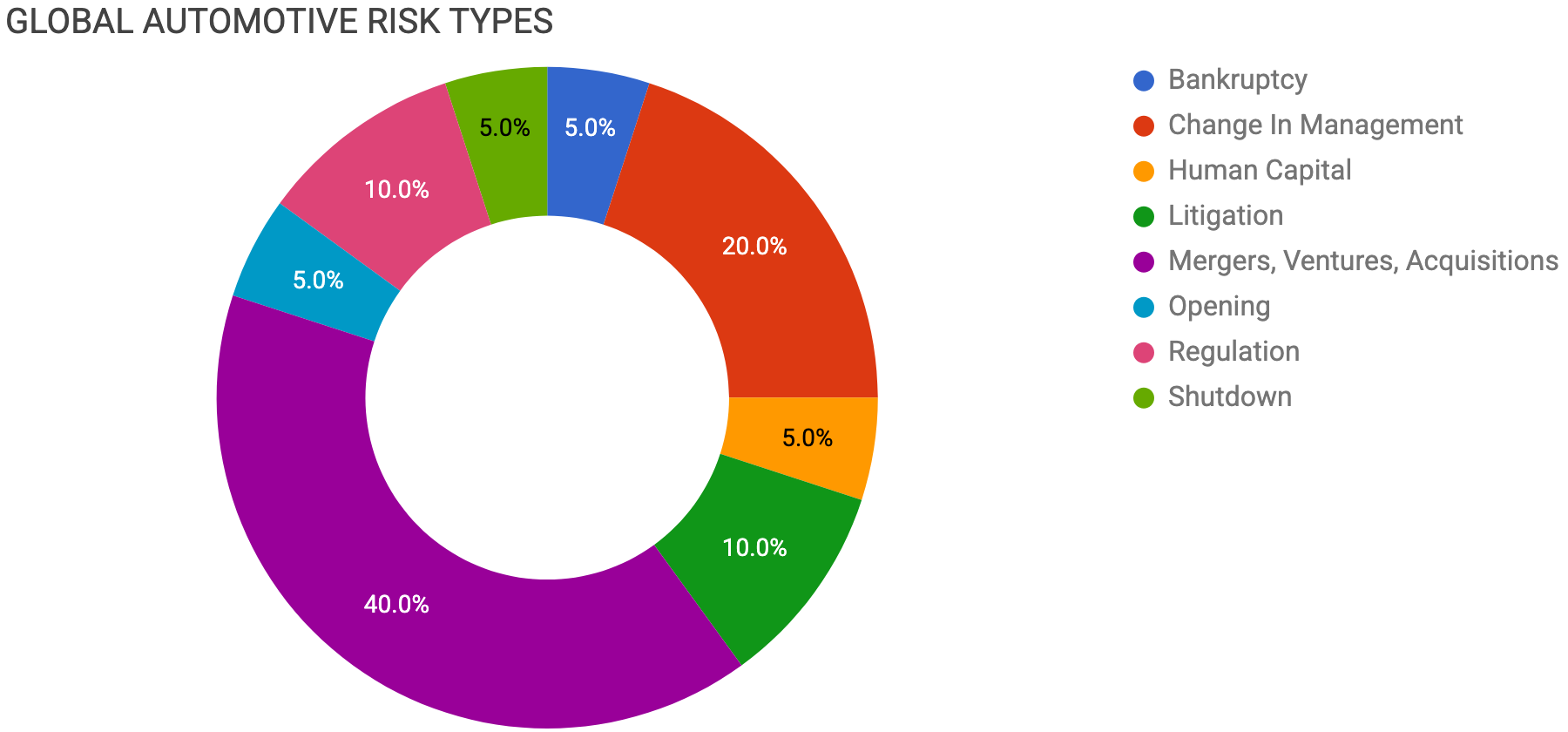

BANKRUPTCY

GM suppliers to mitigate risk with sub-tier mapping

CHANGE IN MANAGEMENT

Toyota taps CFO Kon as CEO

Honda CFO to lead American Honda

GM hires Gast to drive partnerships

Tesla elevates Ward to global sales

HUMAN CAPITAL

GM cuts Ramos Arizpe shift, trims output

LITIGATION

Renault faces German stop-sale IP dispute

Sunwoda settles Geely battery defect claim

MERGERS, VENTURES, ACQUISITIONS

Stellantis takes $26B EV strategy writedown

NextStar stake sold to LG by Stellantis

Samsung battery venture exit also considered

Reuters: Stellantis EV pivot looks permanent

ACC cancels Italy and Germany gigafactories

France funds Imerys Emili lithium project

Chery targets 2026 Barcelona production start

BYD and Geely bid for Nissan/Mercedes Mexico plant

OPENING

Evoring opens Hungary EV driveline plant

REGULATION

EPA endangerment finding reversed by Trump

Dutch court orders Nexperia governance probe

SHUTDOWN

Albemarle halts Kemerton conversion expansion

Bankruptcy

GM held an urgent supplier call this past week to assess exposure to the bankrupt supplier, First Brands, and urged suppliers to map sub-tiers to identify potential risks and avoid disruption.

First Brands, which owns brands including Fram and Raybestos, is operating under Chapter 11. Customers are helping fund a $48M cash advance.

The bankruptcy is a reminder of financial instability risk deep within the supply base, and why Tier-n mapping matters.

Change In Management

Toyota has named CFO Kenta Kon as CEO, effective April 1, replacing Koji Sato. The shift comes as Toyota braces for higher US tariffs, tougher competition, and new supply chain pressure tied to China.

Japan’s latest trade deal leaves a 15% US tariff in place on auto exports. At the same time, China has threatened to curb rare-earth exports, a move experts say could hit Japan’s auto industry quickly.

Inside Toyota, Kon is known for stockpiling semiconductors ahead of pandemic-era shortages and for tightening financial discipline at Woven by Toyota. Kon has stressed that a strong profit structure is key to keeping Toyota resilient in tougher conditions.

Overall, the leadership change signals Toyota’s push to protect financial stability and secure raw materials as tariffs and supply constraints squeeze costs, margins, and production.

Honda appointed CFO Eiji Fujimura as CEO of American Honda effective April 1, replacing Kazuhiro Takizawa, as it faces affordability pressure, increased tariff exposure, and cooling EV demand in its largest market.

Honda has sharply cut its global EV target, reduced Prologue EV volume plans, and is shifting production toward lower-cost gasoline trims. It is also exploring more US manufacturing to offset tariff costs. The leadership change points to continued volatility in the US powertrain mix and in the sourcing volumes that sit behind it.

GM tapped former Lucid strategy leader Claudia Gast to run strategy and corporate development with a mandate to pursue technology partnerships, starting March 1. She replaces Zach Kirkman (ex-Tesla), who is departing after joining in 2023. The hire suggests GM expects greater reliance on partnerships for EVs, software, and automated-driving capabilities, which could shift the supply base and increase integration risk.

Tesla has appointed Joe Ward, its EMEA VP, to lead global sales following the departure of Raj Jegannathan, its North America sales head. The change comes as Tesla’s deliveries have fallen for a second consecutive year and as competition intensifies. That has pushed Tesla to lean more on incentives and to reposition its story around autonomy and robotics.

Human Capital

GM will eliminate a shift at Ramos Arizpe and cut about 1.9k jobs as EV sales soften, reducing output by roughly half. The plant’s gasoline Blazer will be moved to the US earlier than planned, adding uncertainty to the Ramos Arizpe site. The decision creates near-term volume risk for suppliers across northern and central Mexico.

Litigation

Renault could face a stop-sale order in Germany for the Clio and Mégane after a court ruled in favor of Broadcom in a dispute over in-vehicle Ethernet technology licenses. For now, enforcement is suspended.

The case sits within a broader trend: OEMs are becoming more dependent on semiconductor-sector technologies and embedded networks, which increases IP and licensing exposure.

Broadcom pursued a similar action against Volkswagen in 2018, seeking up to $1B in damages. That dispute was resolved before any effective suspension of sales.

Sunwoda has reached a settlement with Geely’s VREMT regarding alleged battery cell defects in Zeekr 001 WE86 packs from 2021→2023. As part of the agreement, VREMT will withdraw its $323M claim.

Sunwoda will pay an additional $89M, and both parties will share any costs incurred after 2025. The affected packs will transfer to Sunwoda. This case demonstrates how cell quality issues can pose significant financial risks and operational disruptions for EV programs.

Mergers, Ventures, Acquisitions

Stellantis is set to absorb a $26B loss as it unwinds much of its US-focused EV strategy. Of this, $15.9B is linked to canceled EV programs and lower sales, while $2.2B stems from scaling back battery production plans. The reset also includes payments to suppliers, additional warranty and quality-related charges, and job cuts in Europe.

CEO Antonio Filosa explained that the company is correcting its “overoptimism on the electrification adoption” by redirecting capital toward hybrids and gas-powered models. He also highlighted a $13B US investment plan aimed at reviving nameplates and shifting some production to avoid tariffs.

For automotive supply chain risk teams, this abrupt pivot points to program cancellations, stranded battery capacity, and risks to tooling recovery. That directly affects suppliers’ revenue visibility and capital planning.

As part of its shift, Stellantis will sell its 49% stake in Windsor’s NextStar battery plant to LG Energy Solution, granting LG full control. The plant has already pivoted to prioritizing grid storage batteries over automotive applications.

Stellantis states it will continue sourcing from the facility and does not anticipate layoffs among the 1.3k workers. This move further signals softening EV demand and a redirection of battery capacity away from automotive programs.

Additionally, Stellantis is reportedly considering divesting from its StarPlus Energy battery joint venture with Samsung SDI, Bloomberg reported.

While a decision has not yet been finalized, an exit could be costly and protracted, potentially requiring a third-party stake sale. Any changes in ownership or pace could disrupt battery capacity timelines and sourcing stability for North American EV programs.

Automotive Cells Company (ACC), the Stellantis-, Mercedes-, and TotalEnergies-backed battery JV, has definitively shelved its planned gigafactories in Termoli, Italy, and Kaiserslautern, Germany.

The projects had been on hold since May 2024 due to weak EV demand. ACC will instead concentrate capacity in France, scaling to two production blocks of 13GWh and 15GWh. Production for Mercedes is expected to start there in mid-2026.

Stellantis reiterated plans to invest in gearbox and engine production at Termoli, and said current ACC employees will be offered roles within Stellantis. The cancellations tighten Europe’s battery localization pipeline and underline how demand swings can derail long-term sourcing plans and regional electrification strategies.

France will invest $54M in Imerys’ Emili lithium project as Imerys looks for additional backers. Production is now planned for 2030. Rising capex estimates and environmental scrutiny are keeping timing and cost risk elevated across the EU battery materials supply chain.

Chery says it will start building its own vehicles in Barcelona “as soon as possible” in 2026. That follows multiple delays from an original 2024 start and a later target of Q4 2025. Chery has cited EU tariffs on Chinese-made EVs as a commercial headwind.

The site is a joint venture with the revived Spanish brand Ebro at a former Nissan plant. It is positioned as a strategic foothold as Chinese automakers gain market share in Spain amid a domestic EV price war.

Chery says the Barcelona plant will build the Omoda 5 (EV + ICE) and later the Jaecoo 7. It also plans to use the facility as an export base for Latin America, targeting up to 150k units by 2029.

For automotive supply chain risk teams, repeated schedule slips and tariff-driven strategy shifts introduce timing and cost uncertainty into European localization plans. The knock-on effects can show up in sourcing decisions, logistics lanes, and supplier ramp schedules.

BYD and Geely are among the finalists to buy the 230k-unit Nissan-Mercedes plant in Aguascalientes. The plant has been closed after US tariffs and weak demand for the model hit exports.

Mexico’s 50% tariff on Chinese vehicle imports is pushing Chinese OEMs to consider local manufacturing more seriously, even as officials weigh the risk of US trade tensions. If a Chinese automaker wins the deal, it would reshape sourcing and increase the supply chain's exposure to geopolitical and trade risks.

Opening

Evoring Precision Manufacturing opened a new plant in Jászfényszaru, Hungary, with a $109M investment and plans for 450 jobs, producing EV gears and axles. The company is part of Zhejiang Shuanghuan Driveline Group, which supplies global customers including Tesla, Volvo, and ZF.

Regulation

The Trump administration reversed the EPA’s 2009 endangerment finding, the legal basis for the federal government’s regulation of greenhouse gas emissions from vehicles.

If the decision stands, it would remove federal GHG standards for all vehicle and engine types. The shift would unwind more than 10 years of emissions rules. It also follows earlier steps, such as rolling back California’s waiver, relaxing fuel-economy standards, and ending federal EV tax credits.

Automakers have argued that prior standards did not match market demand. But some companies, including Ford and Tesla, have warned that removing standards entirely could undermine the regulatory stability they need for long-term planning.

The repeal injects fresh uncertainty into North American powertrain strategies, EV investment plans, and supplier capacity decisions. With legal challenges expected, timelines and requirements could stay in flux.

A Dutch court has ordered a formal investigation into alleged mismanagement at Nexperia. The court also imposed interim controls: it suspended a director, appointed a temporary director, and transferred all but one share to an administrator.

The ruling limits Wingtech’s voting power while the case proceeds. The court raised concerns about unmanaged conflicts of interest, strategy changes made without internal consultation, amid looming sanctions, and potential non-compliance with agreements with the Ministry of Economic Affairs. It also pointed to restrictions on European managers and announced dismissals.

The court said internal divisions between Chinese operations and European and Southeast Asian units have “severely disrupted the production chain,” triggered financial and legal disputes, and put customer deliveries at risk.

The case is a warning sign for the continuity of semiconductor supply and the stability of governance at a key chip supplier. Geopolitical constraints could continue to disrupt production coordination and delivery schedules.

Shutdown

Albemarle is shutting down Kemerton’s remaining conversion train and scrapping expansion plans in Western Australia. Lithium prices remain too low to support the economics of Western hard-rock conversion. The decision reduces near-term capacity and increases the risk of supply concentration for battery-grade metals.