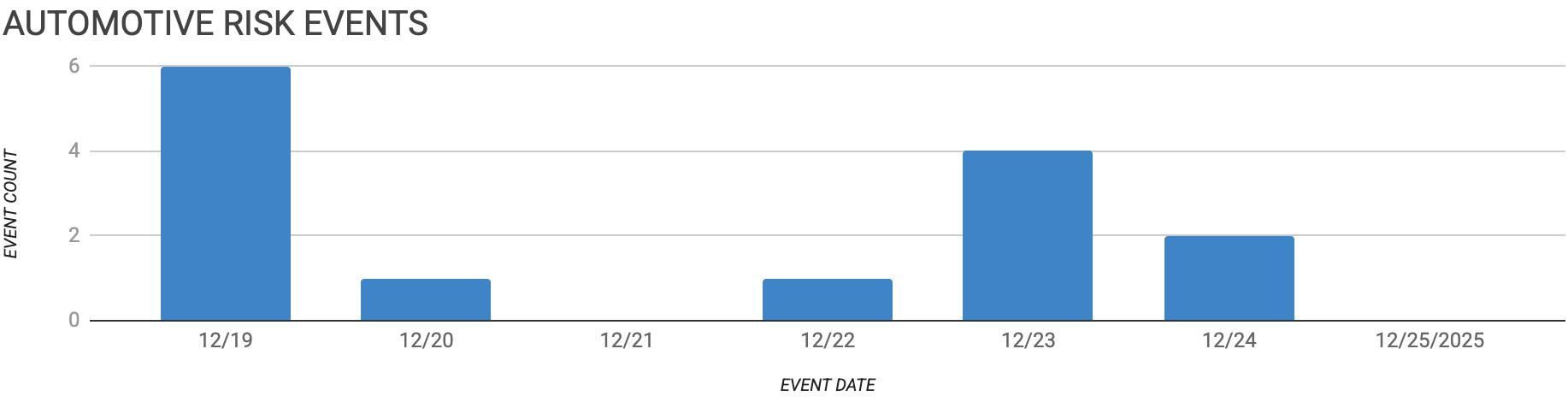

Automotive Supply Chain Risk Digest #462

December 19 - 25, 2025, by Elm Analytics

Dear Reader,

This has been a year of moving targets: policy shifts, volatile tariffs, uneven EV demand, and a steady drumbeat of operational surprises.

Through it all, you’ve continued to open, read, share, and challenge what we publish.

That engagement is what lets us keep refining this digest into something genuinely useful for purchasing, supply chain, risk, and finance teams who don’t have time to chase every headline, but can’t afford to miss the ones that matter.

We’re truly grateful for your trust, your time, and your feedback.

Whether you’ve been with us from the start or only recently subscribed, you’re helping shape how we track and interpret risk across the global automotive value chain.

As you read this week’s edition, we hope it gives you a clearer view of what’s ahead and a bit more confidence in the decisions you’ll have to make next year. Thanks again for reading and for being part of this community.

Warmly,

Nick Gaydos

Editor, Automotive Supply Chain Risk Digest

Elm Analytics, Inc.

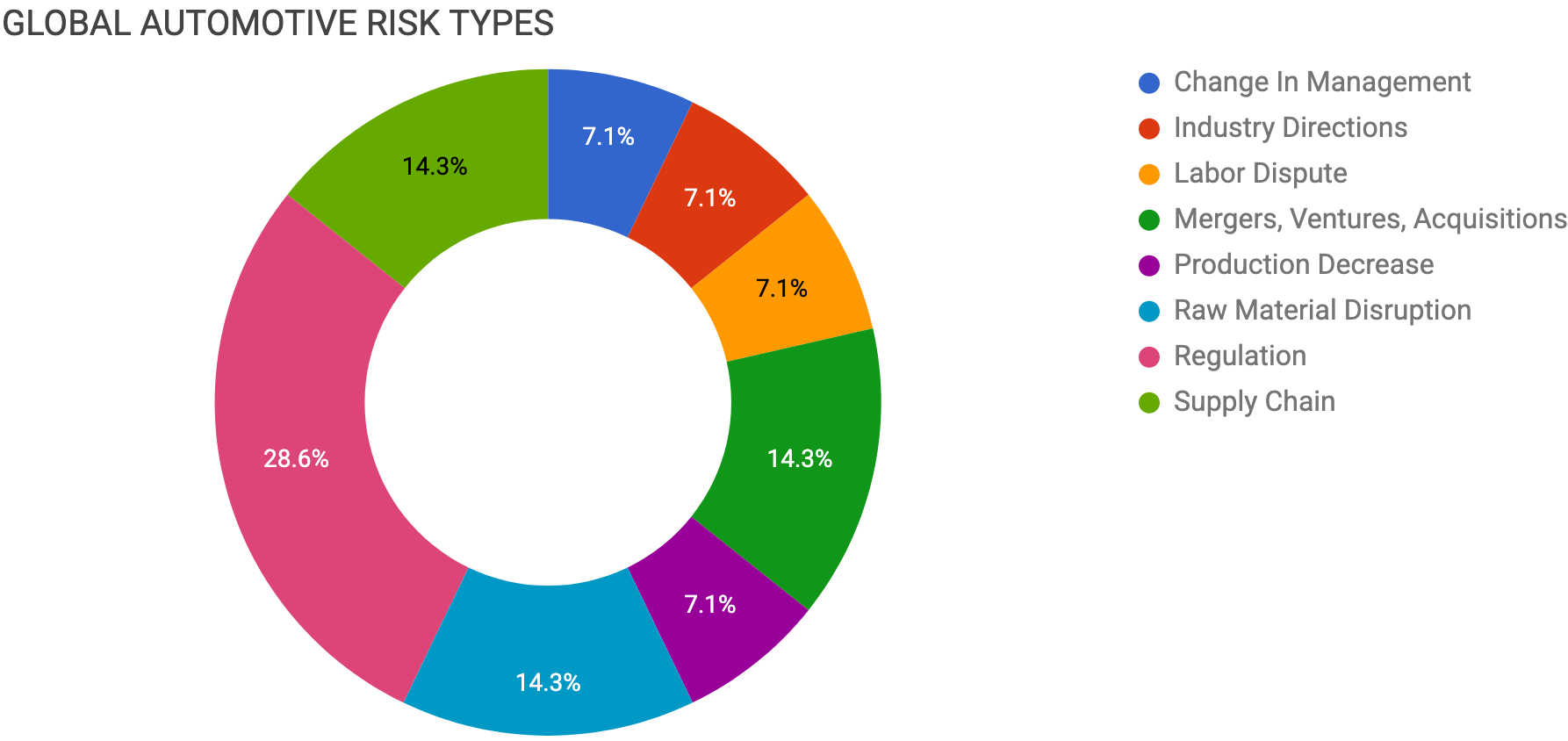

Contents

CHANGE IN MANAGEMENT

Kia Europe names new CEO

INDUSTRY DIRECTIONS

Western EV plans retreat as China advances

LABOR DISPUTE

Tariffs and labor threaten North American plants

MERGERS, VENTURES, ACQUISITIONS

LGES sells Ohio battery assets to Honda

Samsung Harman buys ZF ADAS business

PRODUCTION DECREASE

Ford delays Europe EV platform decision

RAW MATERIAL DISRUPTION

Congo halts artisanal cobalt processing

Battery metals weaken despite EV growth

REGULATION

Tariff uncertainty clouds 2026 auto planning

China tightens approvals for self-driving cars

Stellantis warns EU auto rules deter investment

German auto exports hit by US tariffs

SUPPLY CHAIN

Nexperia China localizes wafer supply

Maersk tests Red Sea route return

Change In Management

Kia has appointed Soohang Chang as CEO of Kia Europe, effective January 1. European sales fell to 479k vehicles in the first 11 months from 495k a year earlier, putting pressure on the new leadership team.

Chang is expected to stabilize volumes, speed up electrification, and manage tougher competition and regulation. He replaces Marc Hedrich, who becomes president of Kia France, maintaining leadership continuity while shifting focus to priority markets.

For suppliers, leadership changes during a sales downturn often signal shifts in model mix, EV launch timing, and resource allocation, with knock-on effects for logistics and inventory planning across Europe.

Industry Directions

Over the past year, Western automakers pulled back from ambitious EV plans as demand softened, costs stayed high, and policy support weakened in the US, Canada, and Europe.

Programs were canceled, plants were retooled, and significant losses followed, including Ford’s $19.5B write-down.

As governments eased or rolled back EV mandates and incentives, future sales became less predictable, forcing both automakers and suppliers to rethink investments in batteries, motors, and electronics.

China moved in the opposite direction, combining strong subsidies with an efficient domestic supply chain and a shift to plug-in hybrids to sidestep European tariffs.

As Western EV growth slowed, Chinese players rapidly gained market share. By year-end, the gap between China’s large-scale EV industry and the West’s uneven progress had widened.

In 2025, Western suppliers adjusted their expectations for EV demand, faced excess capacity and delayed launches, and saw rising risks to the recovery of prior investments, while China extended its cost and volume lead.

Labor

Unifor reports that US tariffs have already led to plant shutdowns, reduced shifts, and production moving out of Canada.

The union expects further disruption as major auto contracts enter negotiations in 2026.

For supply chains, this mix of trade volatility and labor pressure raises the risk of sudden shutdowns, uneven output, and forced realignment of North American manufacturing footprints.

Mergers, Ventures, Acquisitions

LGES plans to sell the Ohio battery plant building and selected assets to Honda for $2.86B, while keeping its joint venture structure and ownership stake. The goal is to streamline operations before production begins next year.

The move highlights a broader shift toward more flexible battery plants and supply arrangements for electric and hybrid vehicles. For nearby suppliers, however, changing ownership and operating models can translate into more volatile short-term materials demand and less clarity on long-term volumes.

Samsung Electronics said its Harman division will acquire ZF Friedrichshafen’s autonomous driving technology business for about $1.8B. The deal adds products such as front-facing cameras and ADAS controllers, extending Samsung’s in-car platform strategy well beyond audio.

For automotive supply chains, this is another sign of consolidation in ADAS and telematics, with potential shifts in bargaining power, integration requirements, and continuity risk for downstream suppliers.

Production Decrease

Ford is delaying a decision on bringing its new Universal Electric Vehicle platform to Europe, saying it wants to prove the architecture in the US first, given the high engineering and capital spend required.

The in-house EV platform will debut on a midsize electric pickup built in Kentucky in 2027, while Ford Europe continues to rely on partnerships with Volkswagen and Renault to limit financial exposure after earlier EV bets missed profitability targets.

The cautious stance reflects lessons from prior EV programs and a broader shift toward smaller, lower-cost vehicles with redesigned manufacturing processes and supply chains. The wait-and-see approach in Europe leaves suppliers uncertain about future sourcing, tooling, and production capacity tied to Ford’s next wave of EVs.

Raw Material Disruption

Congo has suspended artisanal processing of copper and cobalt until operators can prove the origin of mined material. The step is intended to improve transparency and curb illegal or corrupt exports.

Because Congo supplies about 70% of the world’s cobalt, tighter controls could reduce traceable supply and increase short-term price volatility and compliance risk for battery and EV supply chains. Buyers may need to step up due diligence and source tracking to maintain a certified supply.

Regulation

Automakers and suppliers face heightened supply chain uncertainty heading into 2026 as the US Supreme Court prepares to rule on the legality of Trump-era tariffs and the US, Canada, and Mexico launch a required review of the USMCA trade agreement.

The auto industry has already paid about $8.6B in tariffs now under review. Even if the court overturns some duties, the administration may still seek new tariffs under other authorities.

“There’s enough uncertainty with the current administration that each day has the potential to change course for businesses... Every day is Groundhog Day right now.”

- Jeff Lamb, partner at Honigman

At the same time, the US is weighing tariffs on industrial robotics and critical minerals, both of which are heavily used in automotive manufacturing, and plans to expand the list of parts subject to auto tariffs.

With court rulings, trade agreement reviews, and potential new duties all in play, automakers and suppliers are struggling to set sourcing strategies, automation investments, and North American production plans.

After a fatal March crash involving a Xiaomi SU7, Chinese regulators tightened approvals for self-driving vehicles, slowing automakers’ plans for mass deployment this year.

So far, only Beijing Automotive Group and Changan have received approval, and only for limited Level 3 robotaxi tests on selected highways, not for broader commercial use.

At the same time, companies such as Geely, XPeng, and Li Auto have already built vehicles with Level 3 hardware but are selling them with Level 2 software while authorities reassess safety, liability, and insurance rules.

“What looked like an imminent L3 rollout was, in hindsight, a marketing-led acceleration running ahead of governance, insurance frameworks and public trust.”

- Bill Russo, an EV consultant in Shanghai.

This regulatory reset creates significant risk for suppliers, as customers with advanced hardware platforms may face prolonged inventory and operational uncertainty while they wait for approvals.

Stellantis warns that the EU’s proposed auto package increases policy uncertainty and could chill investment, slowing localization and making it harder to build a resilient regional supplier base.

For suppliers, that raises the odds of delayed launches, shifting sourcing footprints, and more cautious commitments to tooling, labor, and logistics contracts.

German automotive exports to the US fell nearly 14% in the first three quarters of 2025, the steepest drop among major German industries. The decline reflects the impact of higher baseline tariffs, which have reset the economics of shipping vehicles into the US.

If these tariffs persist as the new normal, automakers should expect continued volume volatility, margin pressure, and potential shifts in production and sourcing to reduce tariff exposure.

Supply Chain

Nexperia’s China unit has secured silicon wafer supply from local firms to cover its full 2026 production of IGBT power chips after its Dutch parent cut off wafer shipments amid a corporate and geopolitical dispute.

The China business, which declared itself independent of European management two months ago, said it has locked in capacity with suppliers including Wingsky Semi, GAT Semiconductor, and United Nova, deepening the supply chain split with Nexperia’s headquarters.

Earlier, the suspension of wafer supplies and China’s temporary halt of finished-product exports triggered chip shortages for automakers, with Honda already warning of factory stoppages tied to constrained chip availability.

Nexperia says it is not in talks with its China subsidiary and warned that disruptions could resume without a long-term resolution. The dispute accelerates semiconductor supply chain decoupling, raising continuity risk for global automakers relying on power semiconductors and reinforcing China’s push to localize critical chip inputs.

Maersk said one of its vessels has successfully transited the Red Sea and Bab el-Mandeb Strait for the first time in nearly two years, testing a potential return to the Asia-Europe route via the Suez Canal after a Gaza ceasefire reduced security risks.

The company stressed it has no plans for a full reopening and will take a “stepwise approach,” as carriers remain cautious after Houthi attacks forced long reroutes around Africa since late 2023.

“Most carriers appear to be adopting a wait-and-see approach, monitoring developments, and any meaningful reopening would likely unfold gradually.”

- Nikos Tagoulis, analyst at Intermodal Group

Maersk emphasized that the test transit does not signal an imminent shift back to the Suez route despite pressure from longer transit times and higher freight rates.

Even a gradual return to Suez could shorten lead times and ease freight costs, but uncertainty still leaves logistics planners exposed to routing volatility and capacity swings.