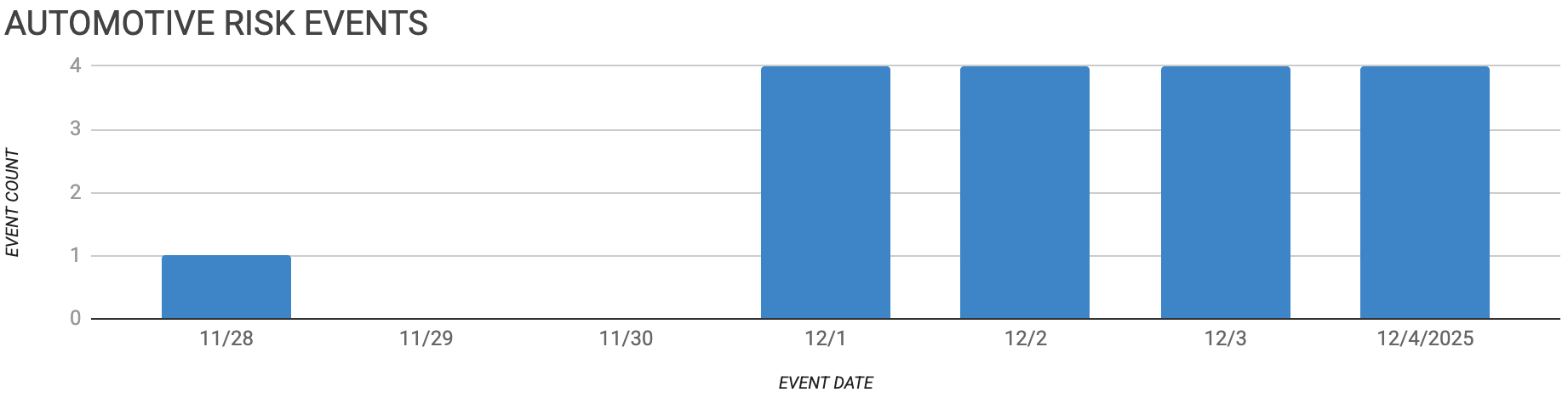

Automotive Supply Chain Risk Digest #459

November 28 - December 4, 2025, by Elm Analytics

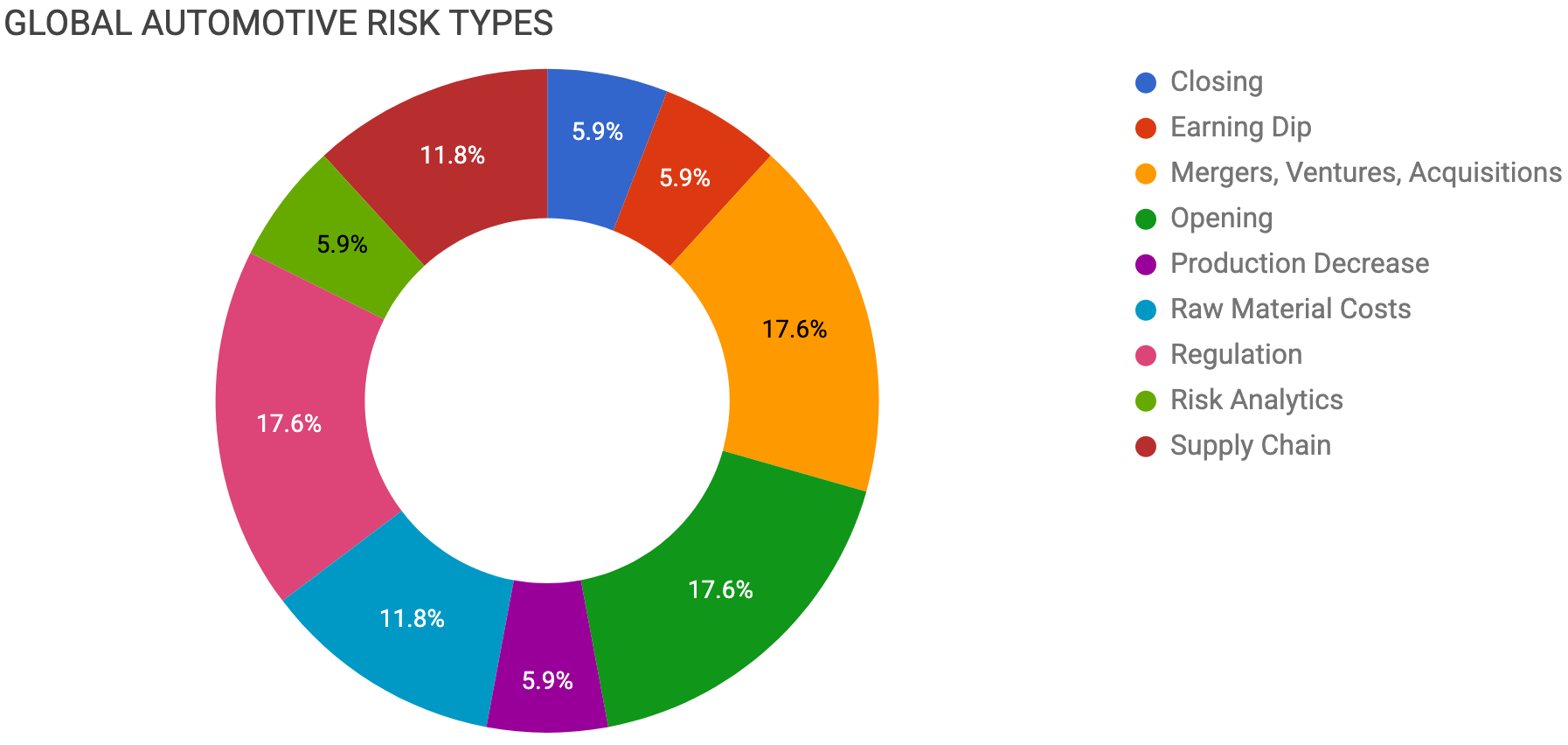

Contents

CLOSING

Rent deferral keeps Bulten operating

EARNING DIP

Chinese EV makers face profit squeeze

MERGERS, VENTURES, ACQUISITIONS

Mahindra trims CIE stake for cash

Factorial, POSCO advance solid-state materials

Symbio restructures after Stellantis exit

OPENING

Sodecia, AAPICO build SC ladder-frame plant

Tongling adds Mexico interior components plant

GO Enerji, LG open Turkish battery facility

PRODUCTION DECREASE

Stellantis forecasts declining French output

RAW MATERIAL DISRUPTION

Congo export halt triggers cobalt squeeze

Indonesian nickel oversupply risk grows

REGULATION

Trump administration eases fuel-economy targets

Canada warns Stellantis over Brampton default

EU delays decision on auto CO2 package

RISK ANALYTICS

Chinese connected-vehicle rise amid restrictions

SUPPLY CHAIN

Nexperia governance clash threatens chip flow

Border blockade forces costly part airlifts

Closing

North Lincolnshire Council has deferred rent payments on Bulten’s Scunthorpe plant to keep the automotive fastener supplier operating at Normanby Enterprise Park in the UK. The move helps the council avoid the cost and risk of a large industrial vacancy after Bulten warned that mounting pressure on the site could threaten its local presence.

Earning Dip

China’s major EV makers, including BYD, Xpeng, Li Auto, and Nio, are posting lower-than-expected earnings.

This has raised new concerns about their profits as government support fades and local demand weakens heading into 2026.

To make up for smaller tax breaks, automakers are offering more rebates, even as battery costs rise, which puts more pressure on already thin margins.

Analysts think competition will get tougher, with mass-market brands like BYD and Geely in a stronger position as buyers look for cheaper cars and automakers increase exports to boost profits.

These challenges could slow the growth of EV programs and change how batteries and parts are sourced, especially for higher-end models that face the most price cuts.

Mergers, Ventures, Acquisitions

Mahindra is selling part of its CIE Automotive stake for $138 million to raise cash, but will still keep CIE as an associate company and maintain its strategic relationship.

Factorial Energy and POSCO FUTURE M are working together to develop key materials for all-solid-state batteries.

They aim to overcome electrolyte and cost challenges that have slowed commercial use. Their partnership is meant to help bring solid-state technology to a larger market.

Michelin, Forvia, and Stellantis will restructure and refinance their Symbio joint venture after Stellantis dropped its hydrogen fuel cell program, cutting the JV’s workforce from about 650 to 175 and refocusing on a 10k systems-per-year target at the SymphonHy site in France between 2028 and 2030.

The deal preserves a smaller automotive hydrogen capability but signals weaker demand from core OEM customers, making hydrogen-focused suppliers’ order books a key watch point.

Opening

Sodecia and AAPICO plan to invest $120M in a new 400k ft² plant in Orangeburg County, South Carolina, to make ladder frames for Scout Motors. The factory, scheduled to open in 2027, will create up to 392 jobs, adding more North American capacity for chassis parts.

Tongling Mexico is investing $91M in a new plant in Irapuato to expand its North American capacity for interior components, including door panels and dashboards, for automakers such as VW and GM. Local leaders describe the project as a clear sign of accelerating Chinese nearshoring to Mexico amid ongoing shifts in global supply chains.

GO Enerji and LG Energy Solution will build a $52M battery pack plant in Ankara, Turkey, that can scale to 7.5 GWh and will target regional export markets.

Production Decrease

Stellantis expects car production in France to drop by about 11% by 2028, to roughly 588k units across its five assembly plants, according to estimates shared with unions.

Three factories are expected to see lower output, with Poissy facing the biggest cut. However, this forecast could change after the EU makes decisions on CO2 rules and support for the auto industry.

These planned cuts come after temporary shutdowns at Poissy and Mulhouse earlier this year, due to weak demand in Europe and a small decline in Stellantis’s French market share as new CEO Antonio Filosa updates the product plan.

Raw Material Costs

Congo’s 10-month stop on cobalt exports, now replaced by a quota system that is not yet approved, has cut off supply from a country that produces about 70% of the world’s mined cobalt.

This has pushed cobalt hydroxide prices from $6 to $23 per pound. The delay is putting pressure on China’s processing chain, with imports dropping sharply since May and inventories running low.

Analysts warn that even if exports restart soon, there could be a cobalt shortage in early 2026.

Longer delays could make the problem worse, especially as the EV market moves toward cobalt-free LFP batteries.

For carmakers and battery producers who rely on cobalt sulphate, this means more price swings, higher costs, and harder sourcing choices.

China played a big role in Indonesia’s rise as the world’s top nickel producer over the past decade, but now Chinese EV makers are moving to nickel-free LFP batteries.

Because of this, more Indonesian nickel is being stored in London Metal Exchange and Shanghai warehouses, inventories are growing, and prices are stuck near production costs.

Still, Indonesian nickel projects are expanding, which could lead to years of oversupply and a large stockpile of unused metal.

Future demand is likely to come from Western EV markets, where nickel-based batteries are still common, but these buyers will want cleaner, lower-carbon nickel, which is a challenge for Indonesia’s coal-powered industry.

Regulation

The Trump administration plans to reduce Biden-era fuel economy rules, lowering the 2031 target from 50 to 34.5 mpg and removing penalties for missing it.

This aims to support gasoline vehicles and cut short-term costs, but it conflicts with the large investments automakers have already made in EV plants, equipment, and supply chains.

Along with tariffs, higher car prices, and different US and global efficiency rules, carmakers and suppliers now face more planning risks and uncertainty about capacity, powertrain choices, and sourcing for North American programs.

Canada has formally notified Stellantis of a default after the company stopped retooling its Brampton, Ontario, plant and moved Jeep Compass production to Illinois.

This puts about $379 million in forgivable loans at risk and leaves about 3k jobs without a replacement plan.

Some funding for Stellantis’s new Windsor battery plant also depends on keeping production at Brampton, making talks with the federal government more important.

Ottawa has already tightened tariff exemptions on Stellantis imports, showing stricter enforcement of incentive deals and adding uncertainty to Stellantis’s Canadian operations, future model plans, and local parts sourcing.

The EU has postponed its December 10 meeting on the Auto Package, which covers possible changes to the 2035 ban on new combustion cars and a Small Affordable Cars initiative.

The meeting is now set for early January. Germany, Italy, and the auto industry want more flexibility and technology neutrality, including allowing hybrids and e-fuels after 2035.

France and environmental groups want the 2035 ban enforced strictly and are also discussing local-content rules for EVs.

UBS expects the outcome to be more flexible, focusing on powertrain mix and CO2 targets, which could lower some industry risks but still require major EV investment to compete with Chinese manufacturers.

Risk Analytics

Supply Chain

Nexperia is once again in conflict with its Chinese owner, Wingtech, after the Dutch government paused its planned takeover of the chipmaker but kept a court ruling that removes Wingtech’s voting rights and its China-backed CEO.

Wingtech and Nexperia’s China branch say Dutch management is trying to “de-Chinafy” the company by moving up to 90% of production out of China by mid-2026, including a planned $300M expansion in Malaysia.

The Dutch side claims Chinese entities are blocking payments, misusing company seals, diverting customer funds, and sending unauthorized messages, while global customers warn of possible production stoppages.

Although China has resumed export exemptions and 7.4B chips have shipped since October, both sides say output is still at risk as the dispute continues.

Ongoing governance issues at Nexperia threaten stable supply from this key automotive chipmaker, raising the risk of allocation cuts and delivery delays for global carmakers and suppliers who depend on its China-based packaging and testing.

A four-day farmer blockade at the El Paso-Juarez ports stranded about 7k trucks, forcing some maquiladoras to book $70k to $90k air charters to keep US plants operating.

The protest ended only after Mexico promised to protect farmers’ water rights. This shows how quickly local disputes can close key routes and lead to expensive measures to keep automotive supply chains running on time.